Financial News Highlights

- Minutes from the December FOMC meeting confirmed that monetary policy was “likely at or near its peak” for this tightening cycle, but showed no meaningful discussion on rate cuts in financial news.

- The U.S. economy added a better-than-expected 216k jobs in December, but downward revisions to the prior two months kept a cooling trend intact. The unemployment rate held steady at 3.7%, while wage growth accelerated slightly.

- The ISM surveys overall signaled softness. Manufacturing remained in contractionary territory in December, albeit slightly less negative, while activity in the services sector slowed but remained in expansionary territory.

Rate Cut Expectations Ease Slightly at the Start of 2024

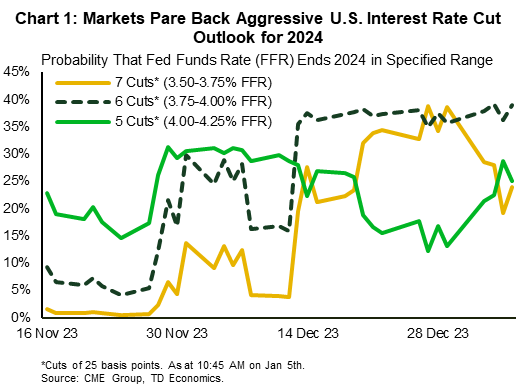

After a festive December where a sharp pullback in long-term yields sent risk assets higher, markets have gotten off to a much more sober start in 2024. Investors have seemingly adjusted their New Year’s resolutions, resulting in more moderate expectations for interest rate cuts this year. Cuts totaling 150 basis points by the end of 2024 remains the dominant scenario. The probability for more aggressive policy loosening (i.e., 7 cuts) has fallen sharply, while the probability of slightly less aggressive loosening (i.e., 5 cuts) has increased (Chart 1). In line with these developments, the 10-year Treasury yield has recouped some of the lost ground, rising from 3.8% at the end of December to near 4% recently, and equity markets have pared back year-end gains, with the S&P 500 down 1.6% from its recent peak.

After a festive December where a sharp pullback in long-term yields sent risk assets higher, markets have gotten off to a much more sober start in 2024. Investors have seemingly adjusted their New Year’s resolutions, resulting in more moderate expectations for interest rate cuts this year. Cuts totaling 150 basis points by the end of 2024 remains the dominant scenario. The probability for more aggressive policy loosening (i.e., 7 cuts) has fallen sharply, while the probability of slightly less aggressive loosening (i.e., 5 cuts) has increased (Chart 1). In line with these developments, the 10-year Treasury yield has recouped some of the lost ground, rising from 3.8% at the end of December to near 4% recently, and equity markets have pared back year-end gains, with the S&P 500 down 1.6% from its recent peak.

The minutes from the December FOMC meeting contributed to the softening in expectations for interest rate cuts this week. After the Fed signaled that the policy rate would head lower in 2024, there was an anticipation that rate cut talk may have featured heavily at the last meeting. Committee participants confirmed that the policy rate was “likely at or near its peak for this tightening cycle”, given the reduction in inflation in 2023 and “growing signs of demand and supply coming into better balance in product and labor markets”. But, meaningful debate on rate cuts was missing. Instead, the discussion was somewhat more balanced, touching on both the risks of maintaining rates in a restrictive position for too long and the risks of prematurely easing policy. Participants noted that their outlooks were associated with an “unusually elevated” degree of uncertainty and stressed the importance of maintaining a data-dependent approach to setting monetary policy.

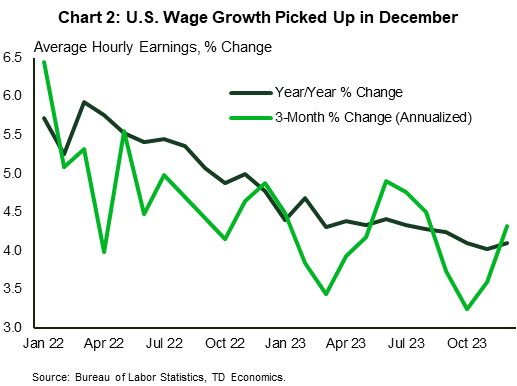

Speaking of data, this morning’s payrolls report showed that hiring unexpectedly accelerated in December, with the U.S. economy adding 216 thousand jobs (see commentary) in financial news. However, a downward revision of 71 thousand jobs to the prior two months limits some of the enthusiasm of this upward surprise. On a three-month moving average basis, hiring is still trending lower, which suggests that restrictive monetary policy continues to work as intended, cooling labor demand. Nonetheless, other aspects of the report still play in favor of showing some caution on easing monetary policy. The unemployment rate held steady at 3.7%. With the labor market still tight, wage growth gained some ground in December (Chart 2). A recent pullback in the job ‘quits’ rate – a leading indicator of labor costs – suggests that wage growth is nonetheless poised to cool ahead.

Speaking of data, this morning’s payrolls report showed that hiring unexpectedly accelerated in December, with the U.S. economy adding 216 thousand jobs (see commentary) in financial news. However, a downward revision of 71 thousand jobs to the prior two months limits some of the enthusiasm of this upward surprise. On a three-month moving average basis, hiring is still trending lower, which suggests that restrictive monetary policy continues to work as intended, cooling labor demand. Nonetheless, other aspects of the report still play in favor of showing some caution on easing monetary policy. The unemployment rate held steady at 3.7%. With the labor market still tight, wage growth gained some ground in December (Chart 2). A recent pullback in the job ‘quits’ rate – a leading indicator of labor costs – suggests that wage growth is nonetheless poised to cool ahead.

Other data reports were a mixed bag. Consumers increased vehicle purchases in December (up 3.2% to 15.8 million annualized), although this appears to be partially related to the return of year-end discounts (see here). Meanwhile, the ISM indexes signaled softness. There was a slowdown in the expansion of the services side of the economy, and the manufacturing sector remained in contraction for the 14th month in row in December, albeit slightly less so on the month.

All factors considered, a loosening in monetary policy is coming, but we anticipate the Fed will show a bit more caution, with the first rate cut not likely to come until the second half of the year.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.