Financial News Highlights

- The labor market cooled modestly in December, with 223k new jobs added and the unemployment rate ticking back

down to 3.5%. - The House of Representatives failed to elect a Speaker of the House on the first ballot for the first time in 100 years,

delaying the start of the new legislative session in the lower chamber of Congress. - FOMC minutes from the December meeting underlined the hawkish stance of the committee and warned of the

dangers of a pre-mature easing of financial conditions.

Plenty of Jobs, Except in Congress

The start of the new year kicked off with several important December data releases, including an update on the labor market and FOMC meeting minutes in financial news. In addition, the new Congressional session got off to a rocky start, with the House of Representatives unable to elect a Speaker of the House. Equity markets fluctuated on the week with the S&P 500 down 0.4% while yields declined sharply, with the 10 Year Treasury at 3.58% as of the time of writing.

The start of the new year kicked off with several important December data releases, including an update on the labor market and FOMC meeting minutes in financial news. In addition, the new Congressional session got off to a rocky start, with the House of Representatives unable to elect a Speaker of the House. Equity markets fluctuated on the week with the S&P 500 down 0.4% while yields declined sharply, with the 10 Year Treasury at 3.58% as of the time of writing.

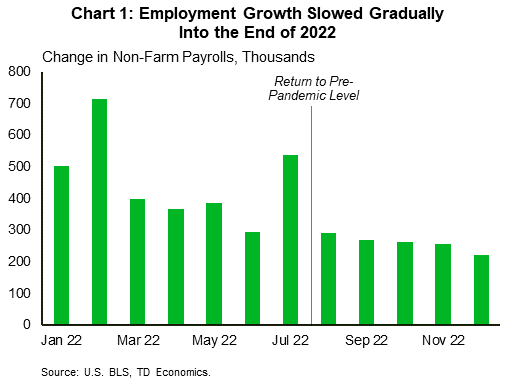

The exceptional strength seen in the jobs market over the past two years slowed into the end of 2022, with December adding 223k new jobs and bringing the annual total to 4.5 million (Chart 1). The labor market remained tight with the unemployment rate declining back to 3.5% as the labor force rose by 0.3% and the participation rate ticked up by 0.1 percentage-points. Average hourly earnings growth decelerated to 0.3% month-on-month, inciting an initial rally in equity markets as participants looked for evidence which might lead to a reprieve from the current aggressive round of rate hikes. The report also showed a notable uptick in the number of multiple job holders reflecting the weight of inflation and rate hikes on households as they seek additional support through secondary incomes.

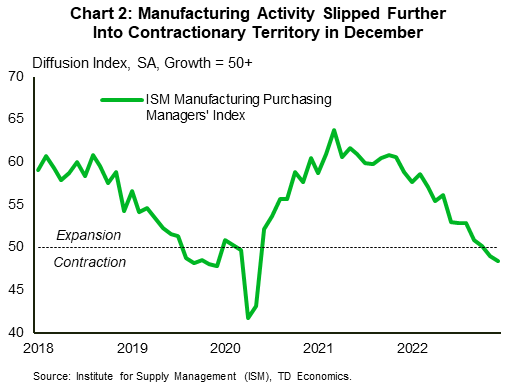

Earlier in the week, manufacturing data showed signs of further slowing, with the ISM manufacturing purchasing managers’ index (PMI) slipping further into contractionary territory in December (Chart 2). After two years of growth the industry has begun to give back some of its gains, in large part due to the direct and indirect effects of higher rates. We also saw this play a part in the ISM Services PMI which declined sharply and showed the sector contracting in December for the first time in 30 months. Within the services index, declines were led by new orders which dropped sharply by over 10.8 percentage-points relative to November. On a more positive note, the manufacturing report showed a continued decline in supply price pressures and improving delivery times, which will be welcome news for the Federal Reserve.

FOMC meeting minutes released on Wednesday unsurprisingly echoed earlier sentiments expressed by Chair Powell at his December 14th press conference. Members pushed back against the loosening of financial conditions seen in recent months on the back of softer inflation reports, noting that “an unwarranted easing in financial conditions…would complicate the committee’s effort to restore price stability” in financial news. The minutes reiterated that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path”, and this was further emphasized by the fact that no committee members foresee cutting rates this year.

FOMC meeting minutes released on Wednesday unsurprisingly echoed earlier sentiments expressed by Chair Powell at his December 14th press conference. Members pushed back against the loosening of financial conditions seen in recent months on the back of softer inflation reports, noting that “an unwarranted easing in financial conditions…would complicate the committee’s effort to restore price stability” in financial news. The minutes reiterated that “it would take substantially more evidence of progress to be confident that inflation was on a sustained downward path”, and this was further emphasized by the fact that no committee members foresee cutting rates this year.

Minneapolis Fed President (and 2023 FOMC member) Neel Kashkari also released an essay on Wednesday in which he noted the need to raise rates by another 100bps this year, which helped to briefly push the odds of a 50bps hike in February close to 50%, though they have since declined back to roughly 25%. Next week we will get December CPI data which will help clarify whether the recent downturn in inflation persisted into the end of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.