Financial News Highlights

- The payrolls report for December came in weaker than expected, capping off the “low hire, low fire” 2025 jobs market.

- Global oil markets adjusted to the possible return of Venezuelan crude to global markets following U.S. actions in the country.

- Investors will have to stay tuned for the Supreme Court’s ruling on the IEEPA tariffs.

Data with A Grain of Salt

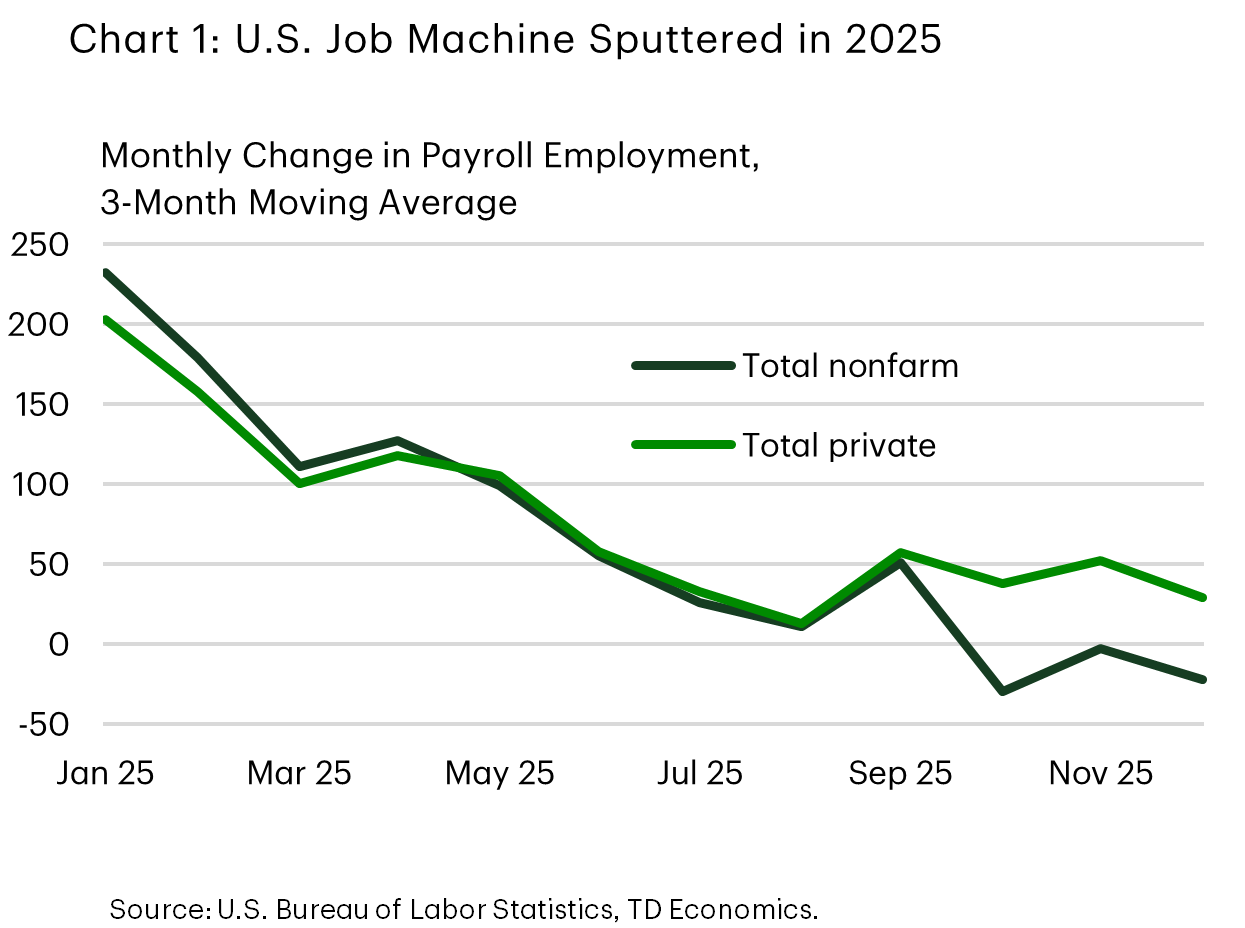

The world was on tenterhooks this morning as all waited to see if the Supreme Court would rule on the administration’s use of the International Emergency Economic Powers Act (IEEPA) to implement some of its tariffs in 2025. The much-anticipated IEEPA ruling did not come, so the big news of the day is the weaker than expected December jobs report. Private sector hiring slowed, prior months were revised lower, and the number of jobseekers declined, allowing the unemployment rate to fall even as jobs growth slowed. The data reinforce the view that 2025 was a “low hire, low fire” year, characterized by a pronounced deceleration in job growth and a modest rise in the unemployment rate (Chart 1).

Survey data this week were mixed. The ISM Manufacturing Index contracted for a tenth consecutive month, with respondents citing “tariff related pricing pressures” and notable reductions in 2026 capital expenditure plans. By contrast, the ISM Services surprised to the upside, highlighting continued resilience in consumer demand for travel, healthcare, and professional services. The divergence between manufacturing and services has persisted throughout the year, as manufacturing remains more exposed to tariff related uncertainty. Both surveys indicated easing price pressures and softening labour demand, consistent with today’s payrolls release.

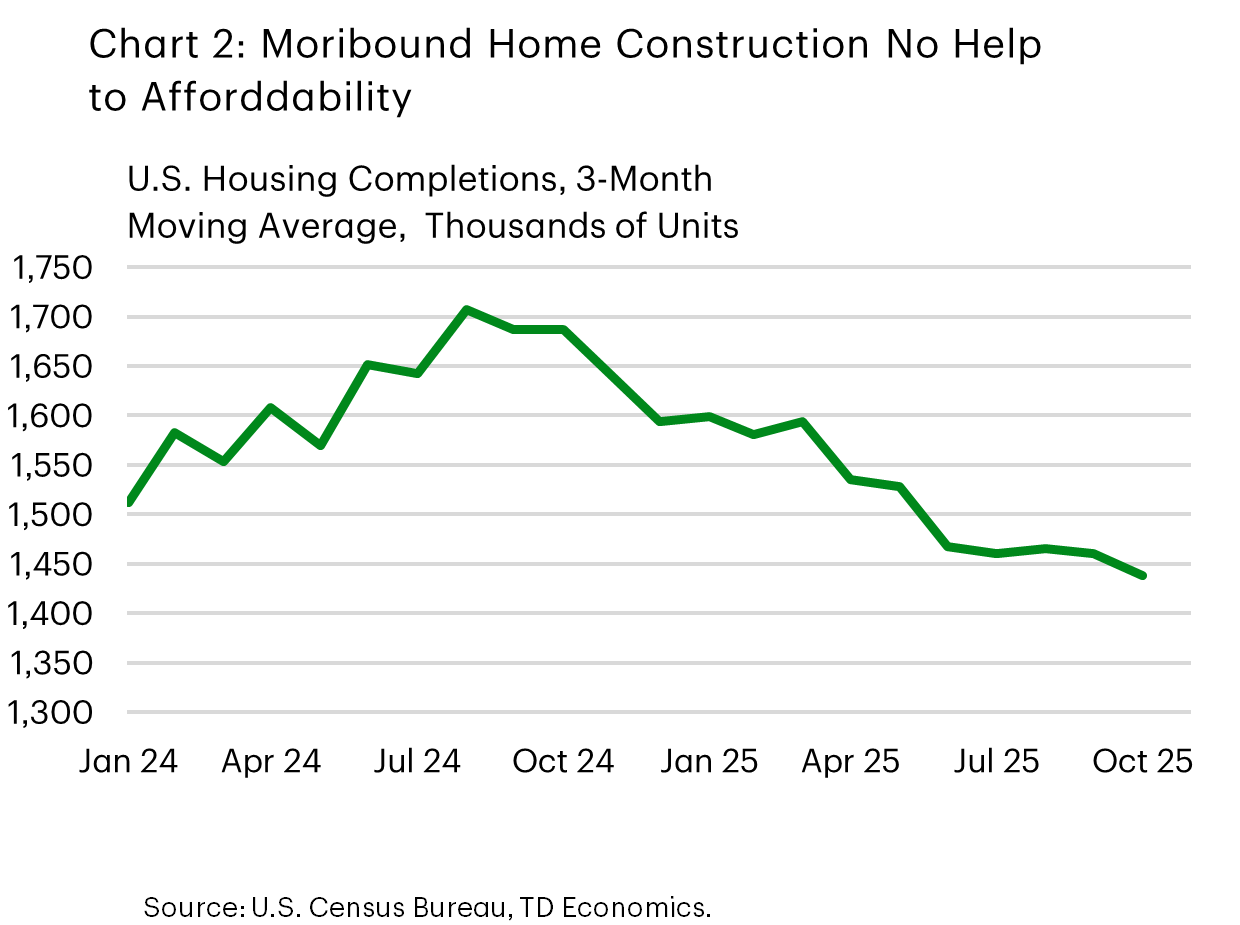

Developments in Venezuela added complexity to the oil market backdrop. Markets are assessing the administration’s commitment to the “Donroe Doctrine” and its implications for global oil supply. Despite Washington’s efforts to restore Venezuelan output, significant logistical and political hurdles remain. WTI moved down toward US$57 following the announcement that up to 50 million barrels of seized Venezuelan crude will be released to help address household affordability concerns. Adding to the affordability theme, housing data showed that homebuilding remains subdued, which doesn’t help the cost of housing (Chart 2). The administration has a clear desire to act on this front, promising a ban on institutional investor purchases and demanding government purchase mortgage-backed securities to help lower mortgage rates, though we await details on actual policy actions.

Prior to Friday’s jobs numbers, Federal Reserve officials suggested risks around employment and inflation were broadly balanced. Minneapolis President Kashkari indicated the labour market may be approaching equilibrium, while Richmond President Barkin characterized the economy as “finely tuned,” implying the FOMC would need to give equal weight to prices and employment. This reinforces our view and the view of the market that the FOMC is not in a hurry to cut rates further now, though we do expect to see interest rates come down later this year. We look ahead next week to the release of CPI inflation data, and after being let down by the Supreme Court this week, we are not going to be alone in being eager for news about when they may release decisions next.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.