Financial News Highlights

- Real personal consumption expenditures contracted in May, as consumers continue to tap excess savings.

- Indeed, in another sign that demand may be softening, core PCE inflation (that excludes food and energy) declined again to +4.7% year-over-year (y/y). Headline inflation (+6.4% y/y) continues to be supported by rising food and energy costs.

- The coming year will certainly pose economic challenges for emerging markets. However, there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

- Three shocks are the main drivers of the lower outlook for EMs: the spring lockdowns in China, the war in Ukraine, and the sanctions on the Russian economy.

U.S. -Consumers Cut Back As Prices at the Pump Surge

Cracks are starting to show in the U.S. economy in financial news. First quarter growth disappointed as the economy contracted for the three months to March. Despite the negative print, there was still reason to be optimistic given resilient consumer demand. Unfortunately, this fillip to growth is quickly fading.

The final release of the first quarter data this week showed that consumer spending was much weaker than realized at first blush. Personal consumption expenditures rose 1.8% (at a seasonally adjusted annual rate) in the first quarter, notably less than the 3.1% expansion reported in the prior release. Consumer services spending was notably weaker, having been marked down by 1.8 percentage points to 3.0%. Durables spending also registered a more tepid expansion of 5.9% relative to the 6.8% previously reported.

Most have expected that goods demand was set to lag as the economy reopened and people were able to travel, go out, and engage with the services sector. So, what is particularly worrisome about the report is the tepid growth in services demand. Indeed, May’s personal income and spending report looks like it reflects an extension of this trend. On a nominal basis spending registered + 0.2% month-over-month (m/m) but, with inflation at multi-decade highs, after price effects were stripped out the real consumption expenditures contracted 0.4% for the month. Worryingly, April’s growth was revised downward to 0.3% m/m from 0.7% prior.

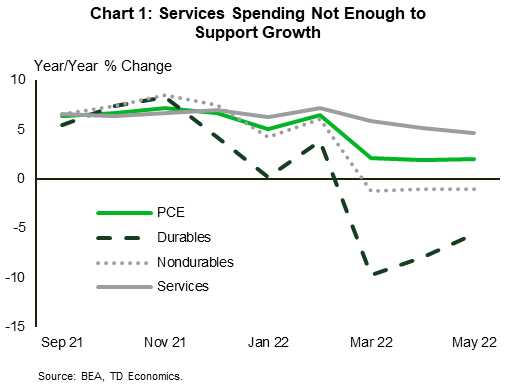

Ultimately this is coming about as the anticipated growth in services spending is not materializing to the extent required to offset the slowdown in goods spending (Chart 1). In May, real services expenditures grew by 0.3% (m/m) but were nowhere near enough to offset the 1.6% m/m contraction in goods purchases in financial news.

Indeed, in another sign that demand may be softening, core PCE inflation (that excludes food and energy) declined again to +4.7% year-over-year (y/y), after peaking at 5.3% in February. Unfortunately, headline inflation (6.4%) picked up and was underpinned by surging food prices and energy goods and services prices, which were up 11.0% and 35.8 % year-over-year respectively. The ongoing surge in the cost-of-living may already be forcing households to make tough choices on what to buy and what to forego, or at least rethink some discretionary purchases.

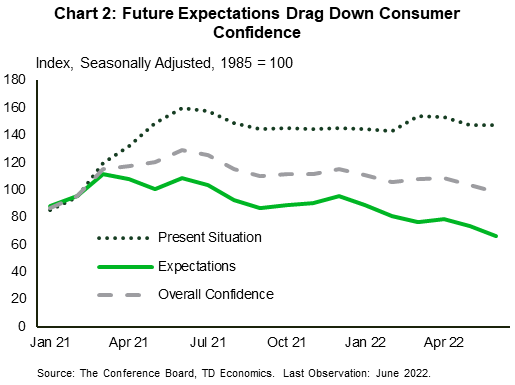

Going forward, the concern is that consumer sentiment continues to fall as inflation and rising interest rates dent disposable incomes and talk of recession raises anxieties. In June, the Conference Board’s measure of consumer confidence reached its lowest level since February 2021. The main culprit being the sustained decline in consumer expectations (Chart 2).

Households are facing a historic cost-of-living crunch. Moreover, given the broader context of high inflation, sagging consumer confidence, and a Fed that remains steadfast in tightening monetary conditions until inflation abates, consumer spending faces a slew of headwinds in the coming months.

Andrew Hencic, Senior Economist | 416-944-5307

Global- Emerging Market Outlook Dims

The skyrocketing food prices and interest rate hikes in advanced economies have raised bad memories of past stumbling blocks for emerging market (EM) economies. The coming year will certainly pose economic challenges, but there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

The skyrocketing food prices and interest rate hikes in advanced economies have raised bad memories of past stumbling blocks for emerging market (EM) economies. The coming year will certainly pose economic challenges, but there is still ample slack to be made up after the past two pandemic years that will provide a fillip to growth for many countries.

We have highlighted the risks to the outlook in our recent Quarterly Economic Forecast (link) and Question and Answer (link) publications. Broadly speaking, tighter financial conditions, slowing growth in advanced economies, the knock-on effects from the war in Ukraine, and China’s commitment to Zero-COVID will all weigh on demand. Our outlook for emerging markets has been marked down to 3.2% in 2022 (from over 4% in our March outlook).

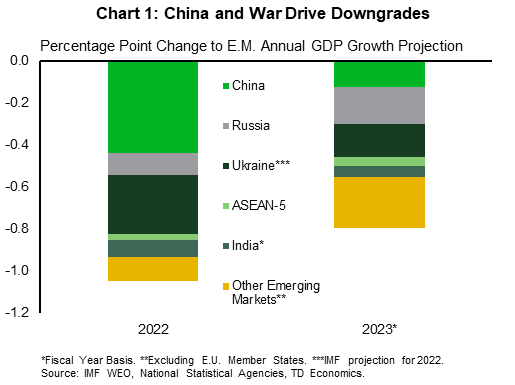

Three shocks are the main drivers of the lower outlook for EMs: the spring lockdowns in China, the war in Ukraine, and the sanctions on the Russian economy (Chart 1). Beyond that, the global economic landscape is shifting as growth in advanced economies slows – with anticipated knock-on effects for the rest of the world.

The war in Ukraine has kicked off another surge higher in energy prices. For most, higher energy prices act as a tax on households, eroding disposable incomes. Moreover, rising prices of key commodities (accompanied by the recent surge in the U.S. dollar) materially raise input costs for firms in import reliant markets.

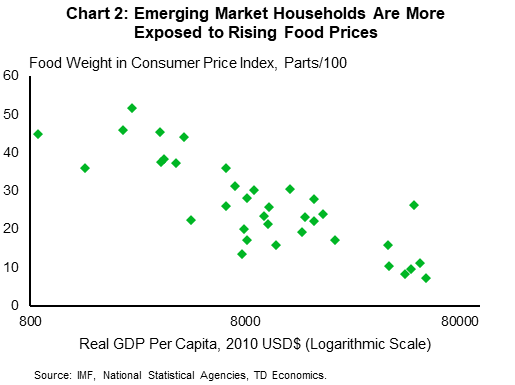

Food expenditures also make up a much larger share of the household expenditure basket in less developed nations than in advanced economies (Chart 2). Higher food prices will be reflected in more severe inflation, that indicates a rapid erosion in living standards and leaves less money available to purchase other goods and services.

Food expenditures also make up a much larger share of the household expenditure basket in less developed nations than in advanced economies (Chart 2). Higher food prices will be reflected in more severe inflation, that indicates a rapid erosion in living standards and leaves less money available to purchase other goods and services.

The increasingly downbeat outlook for China and the U.S. will bleed into total global demand. The two countries accounted for 13.9% and 8.5% of global merchandise imports, respectively, in 2019 and any slowdown in activity will trickle down through supply chains.

Financial conditions have also tightened as monetary authorities have been raising interest rates since 2021, in an effort to combat domestic inflation and stave off capital flight. As higher costs of capital feed through to the economy, the challenging conditions will leave vulnerable firms looking to secure liquidity.

Despite the landscape for emerging markets growing increasingly challenging in 2022 there is room for optimism as services spending resumes. Thailand, for example, saw tourist arrivals plummet from nearly four million in December 2019 to 520 thousand in May 2022. Moreover, if advanced economies execute a soft landing, the risks associated with a rapid tightening of financial conditions can be avoided.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.