FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A tug of war between encouraging vaccine news and hopes of new economic stimulus, and early indications that the recovery might be stalling, is fueling financial market volatility.

- Jobless claims rose to 1.42 million last week after declining for 15 consecutive weeks, suggesting that the labor market recovery might be weakening. By contrast, the housing sector continues to impress as existing home sales soar by 20.7%.

- Congress returned to work and is crafting the next installment of aid to household and businesses. Divergences remain, but an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week

Recovery Risks Stalling Out as Pandemic Worsens

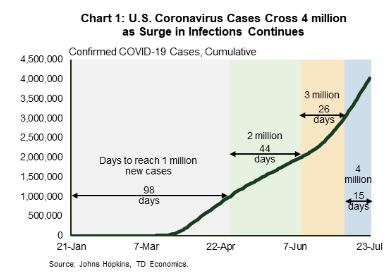

The pandemic marked another gloomy milestone in the U.S. as confirmed coronavirus cases breached the four million mark. This represents a sharp acceleration from just two weeks ago when cases topped three million (Chart 1). From a regional standpoint, California has now surpassed New York for the highest number of cases at over 430,000. With cases continuing to soar in several states, reopening plans are increasingly being rolled back and restrictive measures reintroduced to curb the spread. In one of the latest developments, bars that do not serve food are no longer permitted to offer indoor seating in Chicago, while parties are now limited to six people at restaurants.

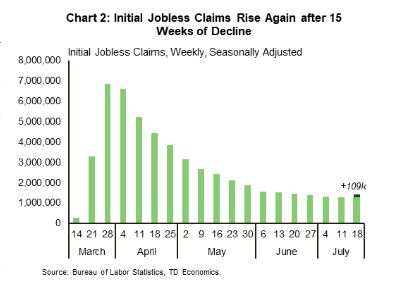

The surge in infections is weighing on economic activity, and this is starting to come through in high-frequency indicators. Initial jobless claims, which had declined for fifteen straight weeks, rose for the week ended on July 18, 2020 (Chart 2). Indeed, filings for unemployment insurance increased by 109,000 to 1.42 million last week, up from 1.31 million in the week prior. While the latest reading is still far below the late-March peak when weekly filings topped 6.9 million, it suggests that the recovery may be losing steam. The historical relationship between claims and employment suggests that employment growth will slow in July relative to the strong gains seen in June and May. This view was also echoed in the Census Bureau’s Household Pulse Survey, which points to increased job losses in July.

With risks increasingly tilted to the downside, policymakers are working on the next set of measures to help support the economy. Across the Atlantic, hard-fought negotiations between EU leaders finally came through earlier in the week in the form of a €1.8 trillion stimulus package. Closer to home, Congress returned to work this week and is crafting the next installment of aid to households and businesses. While divergences over the scope and the size of the next package remain, an agreement is expected over the next few weeks. Likewise, the Fed is set to deliberate on the next steps of its policy response at its scheduled meeting next week. Here’s hoping that the next array of policy responses is enough to keep the recovery on track.

Johary Razafindratsita, Economist | 416-430-7126

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.