Financial News Highlights

-

Highlights

- Real GDP declined for the second consecutive quarter in Q2, meeting one (narrow) criteria of a recession.

- The Federal Reserve delivered another supersized rate hike of 75bps this week, bringing the upper bound of the policy rate to 2.5%. Chair Powell emphasized the need to take rates higher but neglected to give any forward guidance.

- The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth.

- For the European Central Bank, this represents the worst-case scenario, as it could soon be faced with the prospect of raising rates to preserve longer-term stability despite an output contraction.

U.S. Technically Not There (Yet)

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

According to Bureau of Economic Analysis, real GDP declined 0.9% q/q (annualized) in Q2 – well below the consensus forecast of a modest 0.4% gain (Chart 1). More significant than the headline print was that activity has now declined in each of the last two consecutive quarters – meeting one (narrow) criteria of a “technical” recession. At this point, most economists would agree that the US economy isn’t (yet) in recession. The National Bureau of Economic Research (NBER), who is tasked with dating business cycles, would also agree. Outside of just economic growth, the NBER considers a host of other indicators including measures of production, employment, and income. At present, most of these measures continue to point to an economy that remains in expansionary territory.

That said, domestic demand has shown a clear sign of slowing. Consumer spending decelerated to just 1% in the second quarter, while fixed investment declined by 3.9%. At this point, it doesn’t appear that growth prospects will be improving anytime soon. Measures of both consumer and business sentiment have turned decisively lower in recent months, and this is showing in the monthly consumer spending data (Chart 2). After adjusting for inflation, real consumer spending was up just 0.1% m/m in June – a rebound from May’s 0.3% decline – but nonetheless a weak handoff into Q3.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.Perhaps the most noteworthy takeaway from Powell’s entire press conference came from what he neglected to say. In contrast to more recent briefings, the Chair failed to give explicit forward guidance on the expected changes to the policy rate at its next meeting in major financial news. Instead, he emphasized the need to “just go to a meeting-by-meeting basis”, suggesting the size of future hikes will be entirely data dependent. From that perspective, the July/August CPI and employment reports will be under the microscope. However, the Q2 release of the employment cost index will also catch the FOMC’s eye. The index adjusts for the composition of jobs, providing the cleanest snapshot of overall employee earnings. It showed that growth in employment compensation remained elevated in Q2 – growing 5.4% (annualized). From a scoring perspective, this favors another big move in September. Let’s see what employment brings next Friday!

Thomas Feltmate, Director | 416-944-5730

The European Dilemma

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a “meeting-to-meeting” basis for rate decisions that could force them to raise rates into a recession.

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a “meeting-to-meeting” basis for rate decisions that could force them to raise rates into a recession.

Near-term tracking measures have started to show a steep deceleration, or outright contractions, in economic activity in the euro area. July’s flash PMI readings for the euro area reflected a decline in output, with much of the pain being felt in its industrial engine – Germany. The EuroCOIN and Ita-COIN indicators are also showing growth having topped out and starting to fall.

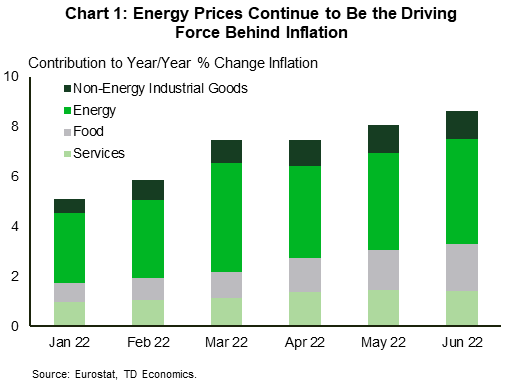

Looking forward, it is the ongoing lift to energy prices that is most concerning. Recession fears have helped crude oil prices off their highs, but supply concerns have supported a high floor under prices. Moreover, if Russia halts natural gas flows to Europe, it risks creating an outright shortage in the coming months, further raising inflation and reducing output. Thus far the energy shock is responsible for roughly half (Chart 1) of the inflationary impulse in the euro zone.

A full stoppage of gas flows would lead to substantial demand destruction and a host of literature on potential losses has emerged in the past months. IMF researchi suggests E.U. output losses could range between -2.7%, in the worst-case scenario and -0.4% if the E.U. were able to fully integrate into the global LNG market.

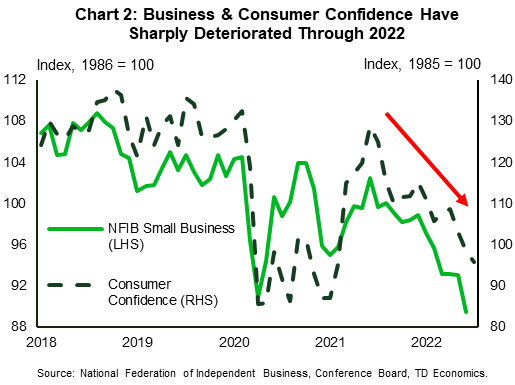

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.Beyond the direct effects, consumer confidence is tumbling (Chart 2). Falls this large typically drive up precautionary savings. Meanwhile, business confidence, having remained relatively resilient through June is starting to weaken notably.

The ECB supported its decision to raise interest rates by 50 basis points by emphasizing the need to temper inflation expectations and the introduction of a new bond-buying tool to help monetary policy transmission. However, higher energy prices are fueling an inflationary feedback loop, and it may soon be faced with the prospect of raising rates to preserve longer-term stability despite an output contraction.

Andrew Hencic, Senior Economist | 416-944-5307

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The dreaded “R” word (recession) isn’t one economist’s use lightly. This is why so much focus was placed on this week’s advance estimate of Q2 GDP and the FOMC meeting in financial news.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September.

The FOMC acknowledged the recent softening in economic data in the very first sentence of its July statement. But that didn’t stop them from raising rates by another 75bps. At 2.5%, the policy rate is now in the vicinity of the FOMC’s assessment of neutral – the interest rate that’s neither accommodative nor restrictive. However, Chair Powell was explicit in the press conference that the Committee intends to raise the policy rate well into “restrictive” territory in order to return price stability. Powell was careful in his word choice, admitting that doing so will lead to some slowing in growth and a rise in the unemployment rate, but skirted any explicit reference to recession. Just how far above neutral the FOMC will have to go remains dependent on how the economy responds to past hikes between now and September. The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a “meeting-to-meeting” basis for rate decisions that could force them to raise rates into a recession.

The European Central Bank (ECB) is facing a daunting outlook. The energy shock due to Russia’s war in Ukraine that is fueling much of the region’s inflation is also increasingly likely to profoundly restrict growth in financial news. As near-term indicators are signaling that a recession may soon begin, the ECB has committed to a “meeting-to-meeting” basis for rate decisions that could force them to raise rates into a recession.

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.

To counteract the risks, the European Commission has asked for a voluntary 15% reduction in natural gas usage across the EU (with some exceptions). These voluntary cutbacks could go a long way to limit the economic fallout from a gas shortage. IMF estimatesii for Germany suggest that by strategically rationing gas, the direct GDP loss in the first six months of the shock could be reduced from 0.9% to 0.2%.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.