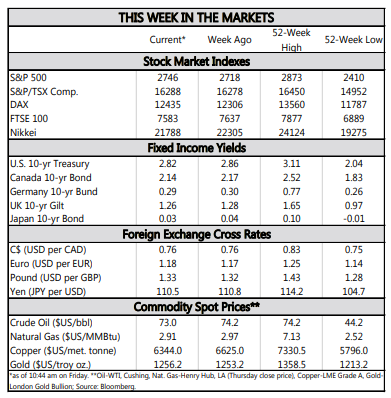

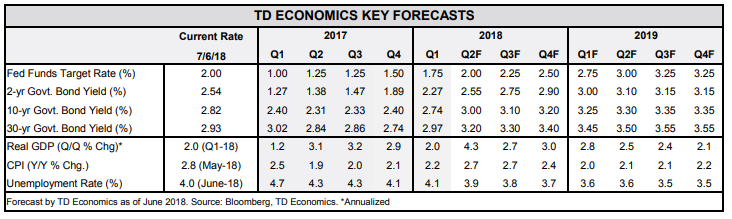

HIGHLIGHTS OF THE WEEK

- A holiday-shortened week was nevertheless chock-full of data releases that confirmed the U.S. economy continues to expand at a strong above-trend pace.

- Economic activity remains robust, but there are signs that trade uncertainty may be impeding further improvement.

- Tariffs on $34 billion in goods from China, and on U.S. goods to China, take effect today. Although these tariffs remain a downside risk to our economic outlook, further escalation could prove direr.

China Tariffs Likely to Impede Economic Momentum

Escalating tensions between Canada’s two most important trade partners weighted on sentiment, but economic data has so far remained intact. Hiring resumed in June with the Canadian economy adding 32k jobs last month. Gains were led by construction and manufacturing, while services disappointed, losing jobs on net for the first time in five months. Despite the job creation, unemployment ticked higher by 20bps to 6.0% as more than 75k people entered the labour force – a six year high. Average wages decelerated, down some 30bps, but at 3.6% y/y remains near a decade-high (Chart 1).

Canadian trade figures were less inspiring with the deficit in May widening to $2.8bn. Imports were up 1.7% and 1.2% in nominal and real terms, respectively. They were somewhat boosted by airliner and gasoline imports, but strength was broad-based across categories, indicative of healthy domestic demand. Exports, on the other hand were weak, remaining flat in nominal terms while volumes fell 1.0%. While much of the weakness was related to transitory factors including supply disruptions in automotive parts and work stoppages in iron mines, exports are unlikely to surge going forward. Alongside ongoing NAFTA uncertainty, the imposition of tariffs in June will have a severe impact on the Canadian metals industry, with potential for downstream effects a real risk.

Risks related to trade and housing will surely be top of mind for the Governing Council when it meets next week to discuss monetary policy. But, until they are seen as likely to materialize they will not drive monetary policy. This is set on incoming data and the outlook, which are relatively sanguine. From that standpoint, another 25 basis point hike next week is the most appropriate move.

Michael Dolega, Senior Economist | 416-983-0500

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.