FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were on tenterhooks all week in anticipation of the British referendum, with anxiety turning to panic overnight as Britain, in a historic vote, decided to leave the European Union (EU).

- Central banks announced readiness to deal with any fallout related to potential liquidity shortages, helping stem near-term pressures in global markets but longer-term implications of the vote are far from certain. Still, there is little doubt that the economic implications are a net-negative and could be far reaching.

- In her semiannual testimony to Congress mid-week, Chair Yellen noted the potential for “significant economic repercussions” of such an outcome that could “usher in a period of uncertainty,” and negatively affect U.S. economic activity, with the Fed likely to monitor global developments closely.

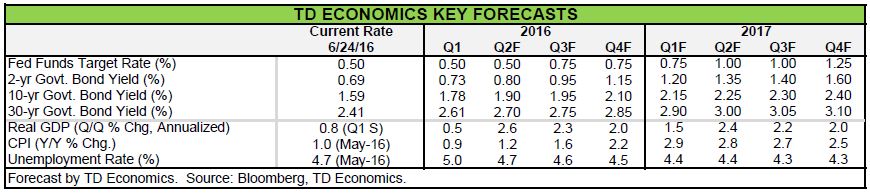

- Given the implications for slower U.S. growth and lower inflation, on account of the fallout, we expect the Fed will stay pat through the rest of the year.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

KEEP CALM AND TRADE ON… AS BRITAIN LEAVES THE EU

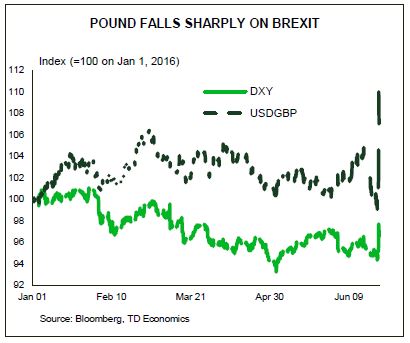

Markets were on tenterhooks all week in anticipation of the UK referendum. Anxiety turned to panic overnight as Britons, in a historic vote, decided to leave the EU. Despite the very close polls ahead of the vote investors increasingly positioned themselves for a status-quo result. In fact, sentiment was decidedly risk-on right through until voting booths closed at 10pm GMT. But, as results started to trickle in, doubts surfaced, with the BBC finally calling the vote for the “leave” camp at 4:45am London time. The final tally was 51.9% to 48.1% with 1,269,501 more votes cast in favor of divorcing the UK from the EU. Turnout was high, at 72.2%, but fell shy of that level in London, Scotland, and Northern Ireland – all bastions of the “remain” camp.

The pound fell as much as 12% versus the dollar as the outcome became clear. Gold and volatility surged while equities and the safest of bond yields slumped, before some retracement this morning. At this point, central banks have announced their readiness to deal with any near-term fallout related to potential liquidity shortages, with the Federal Reserve noting it is prepared to provide dollar liquidity through existing swap lines with major central banks. The concerted central bank move should help stem near-term pressures in global markets. But, longer-term implications of the vote are far from precise given the rapid and substantial repricing in global markets, the ensuing volatility, and uncertainty of the political response on both sides of the channel.

Despite the unknowns, there is little doubt that the economic implications are a net-negative and could be far reaching. The uncertainty and lack of access to the common market will almost surely decimate business investment in the UK and probably stifle trade with the EU (and potentially others) – something that’s not likely to be fully offset by the slumping sterling. The expected downturn will likely necessitate a monetary policy response from the Bank of England, which is most likely to cut rates at its meeting in August despite the expected uptick in inflation owing to the sharp currency depreciation. At the same time, while the EU may benefit from the exodus of capital from the UK into the region, it too will likely suffer from reduced trade ties and uncertainty, which could also drag on economic growth, delaying the region’s recovery even further.

While the economic impacts of Brexit will undoubtedly be most pronounced across the pond, the U.S. will not be immune to the fallout. In her semiannual testimony to Congress mid-week, Chair Yellen noted the potential for “significant economic repercussions” of such an outcome that could “usher in a period of uncertainty.” While the Chair didn’t believe such an outcome would trigger a recession in the U.S., she was forthright in saying that Fed officials “just don’t really know what will happen,” but will monitor developments closely, particularly as far as they relate to “domestic economic activity, labor markets, and inflation.”

On the domestic front, Chair Yellen’s testimony warned against focusing too much on a single data point and reinforced the view that despite the weak May employment report, the labor market continues to improve. This view was supported by this week’s initial jobless claims data, which fell down to 259 thousand. The Chair largely stuck to the script of accelerating U.S. growth, and indicated that wage growth is strengthening – corroborating a finding from our recent paper. Ultimately, rising wages and incomes should keep America’s economy supported through resilient consumption and the housing recovery – a view reinforced by this week’s data on existing home sales which rose to an eight-year high of 5.53 million.

The Chair declined to weigh in on when the Fed will next raise rates warning instead, perhaps ominously, that risks abound. In light of the negative implications from a surging greenback and financial volatility on U.S. trade and financial services industry, coupled with the downward pressure on inflation from the former, we expect the Fed will remain on the sidelines through the remainder of the year, and potentially well into 2017 given the downside risks that have surfaced.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.