Financial News Highlights

- Oil prices fell below $70/barrel, flirting with pre-conflict levels as the U.S. and Iran continue to negotiate towards a permanent resolution.

- The Federal Reserve’s preferred inflation metric, core PCE, rose 3.4% year-over-year in May.

- Personal income and spending both rebounded in price-adjusted terms in May, though households have increasingly relied on savings to support spending.

Oil Prices Retreat as AI Volatility Picks Up

The first week of summer was relatively quiet on the economic data front, with financial markets consumed by developments in the Middle East and evolving trends in AI. The latter proved to be a source of volatility in equity markets this week, as news of personnel changes at Alphabet led to a sell-off that spread to the broader AI ecosystem. This was partially reversed later in the week, but still highlights the inherent sensitivity of markets under the combined influence of elevated valuations and market concentration. The S&P 500 was down 1.8% while U.S. Treasury yields moved modestly lower on the week as of the time of writing.

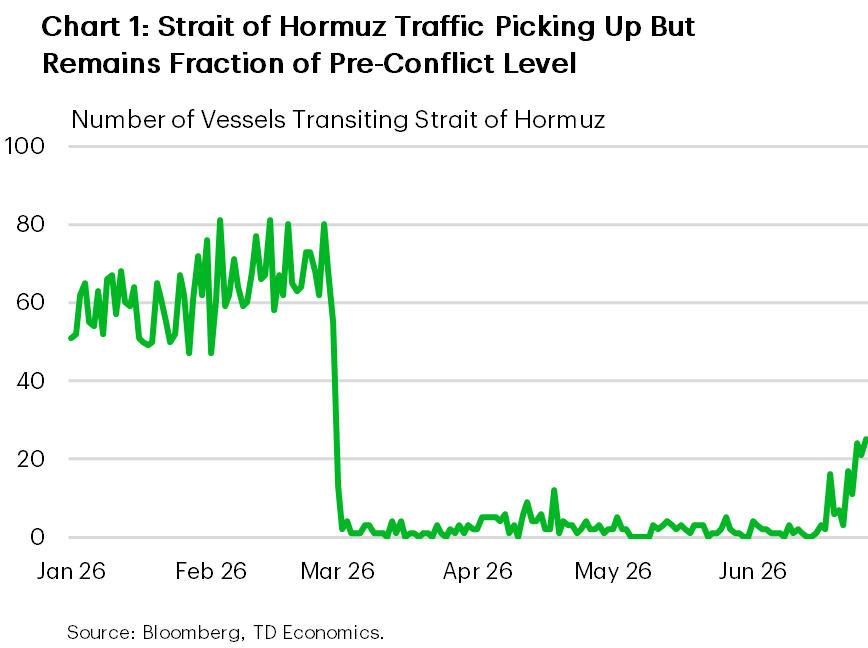

On the geopolitical front, negotiations between the U.S. and Iran continued after the two sides signed a 60-day memorandum of understanding (MOU) last week. The cessation of hostilities and reopening of the Strait of Hormuz have been enthusiastically welcomed by financial markers, with oil prices now back at their pre-conflict level. However, it bears repeating that the resumption of oil trade through the vital passageway is likely to be a gradual process as evidenced by the current level of maritime traffic through the strait (Chart 1). Combined with the possibility for roadblocks to be encountered during negotiations, risks related to oil prices remain skewed to the upside.

The feedthrough of higher energy prices to the economy was evident in the PCE inflation reading for May. Prices were 4.1% higher year-on-year (y/y) during the month, primarily driven by a 24% increase in energy prices. However, broader inflation pressures were also present, with core PCE inflation, which excludes food and energy products, rising 3.4% y/y. With energy prices having sharply reversed, some downward pressure on overall inflation is already in-tow. However, uncertainty around the magnitude and duration of energy-related second-order effects has given policymakers reason to adopt a more hawkish stance.

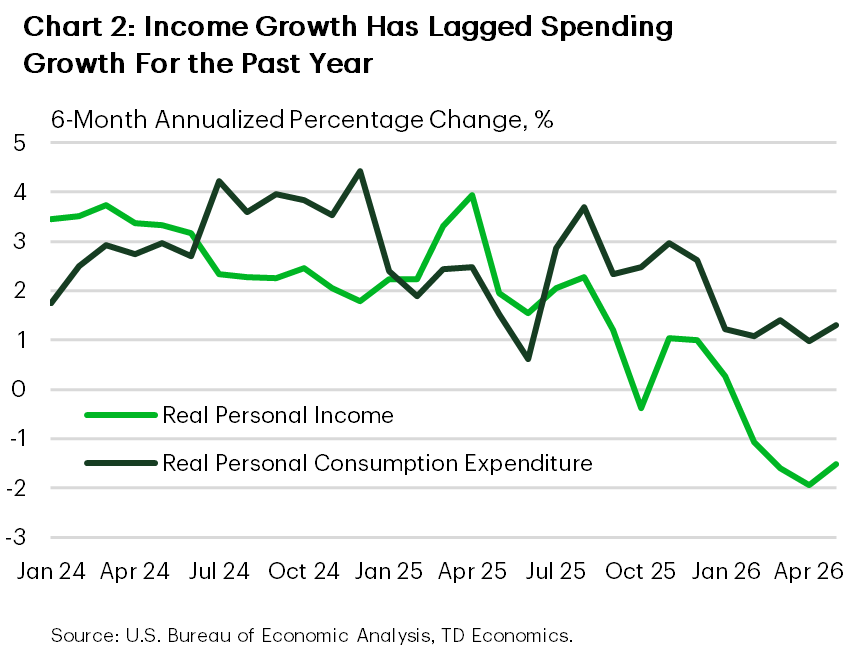

Personal income and spending both rebounded in real (price-adjusted) terms in May after softer readings in April, reflecting the sustained resilience of the American consumer. Still, much of the spending in recent months has been driven by a drawdown in savings, with the savings rate remaining at 3% in May – far below its historical average of 5-6%. While robust financial returns over the past few years may be offsetting the extent to which consumers need to save to meet their financial goals, the downward trend in the savings rate also began in mid-2025, coinciding with the introduction of broad tariffs and likely reflective of the multitude of cost pressures that have weighed on consumers over the past year (Chart 2).

Looking ahead to next week, the June employment data release on Thursday will be the highlight. Markets currently expect 118k new jobs to have been created during the month, marking a moderate deceleration relative to the strong reading in May. Fed Chair Warsh will also participate in a panel discussion next Wednesday, which will be watched closely for any signals on monetary policy decisions over the second half of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.