Financial News Highlights

- Chair Powell’s testimony threw the market in to risk-off mode with both the Treasury and equity market falling on the week.

- The economy added 311k jobs in February, well ahead of the consensus forecast of 225k, reinforcing the resilience of the job market.

- There’s still plenty of data to come in before the Fed’s rate decision, with next week’s inflation report the most important.

Jobs Market Stays Strong

Chair Powell’s bi-annual testimony to Congress pushed the market into risk-off mode as his explicit remarks put the half-point rate hike back on the table in major financial news. In his statement, Powell highlighted the strength of the latest economic data, “which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated”.

Chair Powell’s bi-annual testimony to Congress pushed the market into risk-off mode as his explicit remarks put the half-point rate hike back on the table in major financial news. In his statement, Powell highlighted the strength of the latest economic data, “which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated”.

Treasuries plunged to fresh lows, with the two-year yield moving briefly above 5% for the first time since July 2007, while keeping the ten-year yield hovering just below 4%. As a result, the spread between the two (one of the strongest market-based recession indicators) widened to the 100-basis point mark before narrowing back to 90 bps by the end of the week (Chart 1) in financial news. This is the deepest inversion since 1981. The equity market was as volatile, with the trouble at SVB Financial Group adding to shock. The S&P 500 Index moved below the 4,000-level finishing the week with a 3.4% loss (at the time of writing).

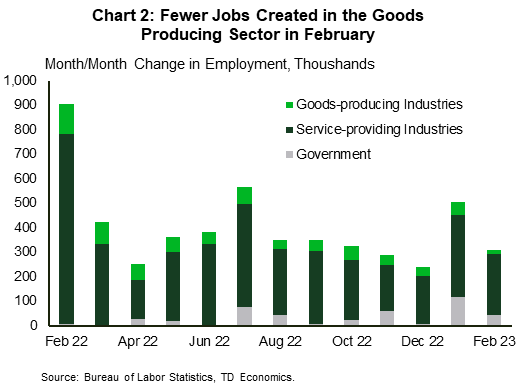

Today’s payrolls report didn’t help settle the markets. The employment number came in stronger than anticipated (at 311k v. 225k expected), suggesting that there is considerable strength in the jobs market. The unemployment rate returned to 3.6% as the labor force expanded, lifting the participation rate to 62.5%. Notably, the monthly increase in the goods producing sector was the smallest since May 2021, with job gains tilted towards the services sector (Chart 2). The trend pace of average hourly earnings growth over the past three months slipped to the slowest pace of growth in nearly two-years. However, hourly earnings don’t adjust for compositional effects across sectors, and have been running well below other metrics in recent months. February’s softness is likely in part due to job gains concentrated in lower-wage sectors and jobs losses in some higher-wage ones.

The tight labor market was also evidenced in January’s Job Openings and Labor Turnover Survey (JOLTS). While job vacancies declined to 10.8 from an upwardly revised 11.2 million in December, they remain high, suggesting that demand for workers exceeds supply – a condition that will continue to support wage growth.

The tight labor market was also evidenced in January’s Job Openings and Labor Turnover Survey (JOLTS). While job vacancies declined to 10.8 from an upwardly revised 11.2 million in December, they remain high, suggesting that demand for workers exceeds supply – a condition that will continue to support wage growth.

There’s still plenty of data to come before the Fed’s March 21-22 meeting, when the Fed decides on the rate hike and releases updated economic projections. Next week, we’ll have more details on CPI and retail sales for February. The former has more bearing on the rate decision, as it makes up the second half of the Fed’s dual mandate (besides maximum employment), while the latter may contribute to the Fed’s understanding of consumer spending momentum. To convince FOMC members to keep the same pace of rate hikes as in December, price changes would need to provide evidence of a decelerating trend. Today, the probability of a 50-basis points hike settled around 40% – higher than 28% last week but lower than more than 70% earlier this week.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.