Financial News Highlights

- FOMC voting members noted the interest rate path will depend on incoming data and highlighted the uncertainty surrounding the effects of regional bank stress on credit availability.

- Inflation remained relatively elevated, despite moderating last month, as total and core PCE inflation both rose 0.3% month-on-month (m/m) in February.

- Pending home sales in February surpassed expectations by a notable margin as modest price declines and lower mortgage rates supported activity at the start of the year.

Quiet End to a Volatile Quarter

The last week of the first quarter was relatively quiet as markets continued to digest last week’s Federal Reserve decision and the potential implications of regional bank stress on credit conditions in financial news. In terms of economic data, we received updates on housing, consumption, and inflation. Equity markets drifted higher on the week, with the S&P 500 up 2.5%, while the 2-year Treasury yield rose by roughly 30 basis-points (bps) to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.

The last week of the first quarter was relatively quiet as markets continued to digest last week’s Federal Reserve decision and the potential implications of regional bank stress on credit conditions in financial news. In terms of economic data, we received updates on housing, consumption, and inflation. Equity markets drifted higher on the week, with the S&P 500 up 2.5%, while the 2-year Treasury yield rose by roughly 30 basis-points (bps) to sit at 4.1% as of the time of writing – still about 90bps below its cyclical peak of 5% at the start of the month.

Starting off on Sunday, we heard from Minneapolis Fed President Neel Kashkari. Reiterating Chair Powell’s statements from last week, Kashkari noted that the banking system is resilient, but that uncertainty remained regarding the extent to which stress in the banking sector may lead to a credit crunch in financial news. For this reason, Kashkari assessed that “it’s too soon to make any forecasts about the next interest rate meeting [in May]”. This marks a notable deviation from his comments on March 1st that he was open to a 50bps hike in March. The uncertainty is also reflected in the market’s sentiment about the Fed’s May decision – now pricing the odds of a hike at basically a coin toss.

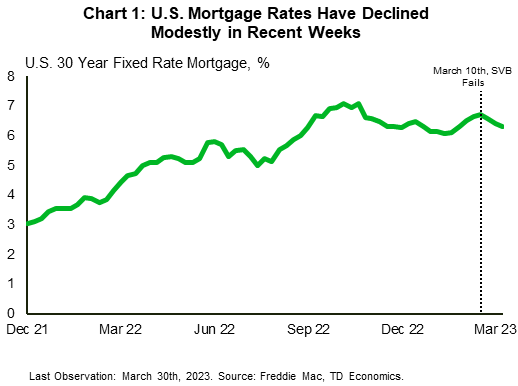

Housing data surprised to the upside this week, with pending home sales rising by 0.8% month-on-month (m/m) in February, down from the 1.8% rise seen in January, but well above the consensus expectation of a 3% m/m decline. This relative strength was likely front-loaded in the month, as mortgage rates rose by roughly 50bps in February. Pending home sales tend to lead final sales by 1-2 months, so this could be an indicator that the spring housing market may begin with some strength, particularly considering that mortgage rates have fallen by roughly 30bps since March 10th (Chart 1). However, stretched affordability and still relatively high financing costs are expected to remain notable headwinds moving forward.

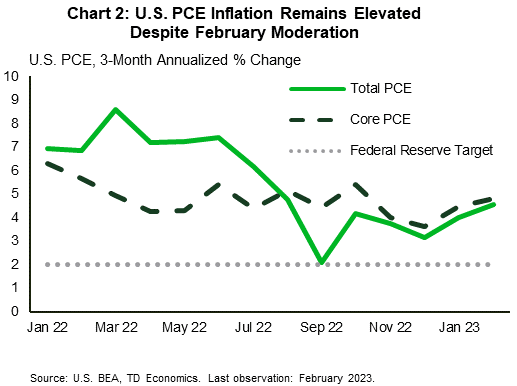

The pulse check on the American consumer this week showed that personal income grew by 0.3% m/m in February, decelerating from January’s gain of 0.6%. This helped to push personal spending up by 0.2% m/m, with housing and health care services seeing the largest increases. Total and core PCE inflation both rose by 0.3% m/m, decelerating relative to January but remaining elevated (Chart 2). More recent data showed that consumer confidence rose in March on a modestly improved outlook for six months ahead, whereas the consumer assessment of the current economic situation deteriorated. The survey cut-off was 10 days after SVB failed, so it is likely that this reading only partially captures the consumer response to recent banking sector stress.

The pulse check on the American consumer this week showed that personal income grew by 0.3% m/m in February, decelerating from January’s gain of 0.6%. This helped to push personal spending up by 0.2% m/m, with housing and health care services seeing the largest increases. Total and core PCE inflation both rose by 0.3% m/m, decelerating relative to January but remaining elevated (Chart 2). More recent data showed that consumer confidence rose in March on a modestly improved outlook for six months ahead, whereas the consumer assessment of the current economic situation deteriorated. The survey cut-off was 10 days after SVB failed, so it is likely that this reading only partially captures the consumer response to recent banking sector stress.

Looking ahead to next week, markets will be closely watching the March employment data release on Friday, with consensus expectations for job growth to cool and the unemployment rate to remain unchanged. This will be one of the more important updates between now and the May Fed meeting, as policymakers continue to look for signs of labor market cooling and its subsequent easing effect on price growth.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.