FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The labor market added 678k jobs in February, and the unemployment rate fell to 3.8% – the lowest reading since the pandemic began.

- Early indicators suggest that manufacturing and services sectors were out of sync in February, with the former accelerating and the latter slowing down. The difference is largely attributed to continued weakness in demand for services.

- The Russia-Ukraine War continues to reverberate through financial markets, lifting commodity prices and threatening to tighten financial conditions further. The Fed is likely to raise interest rates in March, but the speed of future rate hikes is more uncertain.

U.S. -Economy Marches On, Volatility Spikes due to the Russia-Ukraine War

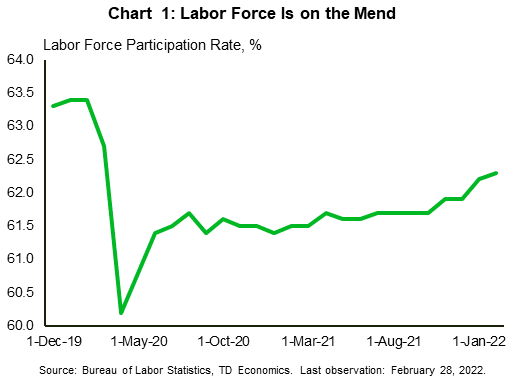

It’s the first week of March, which means we get the initial glance at how the economy did in February, when the Omicron wave started to ease in financial news. This morning, the U.S. Bureau of Labor Statistics surprised the market with 678k jobs created in February, well above 400k anticipated by forecasters. This was on top of an upward revision of 92k to December and January. The unemployment rate fell to 3.8 % – the lowest reading since the pandemic, just 0.3 percentage points above the level two years ago. The labor force – a measure of people working or actively looking for work – also made progress. The labor force participation rate ticked up to 62.3% after 304k people joined labor force in February (Chart 1). All in all, labor market is getting tighter and tighter.

In the meantime, leading business indicators diverged. As measured by the ISM Index, the manufacturing sector reversed three months of decline, accelerating to 58.6. Demand was solid, with new orders moving above 60 again. Production accelerated, but it could have been even stronger without materials supply constraints. The backlog of orders index jumped by almost 9 percentage points (ppts), while supplier deliveries inched 0.5 ppts higher. Despite all these challenges, inventory rebuilding continued, albeit at a very slow pace adding only 0.4 percentage points in February.

Surprisingly, the services sector slowed in February, with the two demand indicators – business activity and new orders – declining to mid-50 levels, last seen exactly one year ago. The consensus anticipated a modest increase, expecting that the fading threat of Omicron would help the services sector bounce back. Respondents blamed the post-holiday fatigue and difficult business conditions, affected by capacity constraints, inflation, logistical challenges, and labor shortages. Indeed, supply-side indicators deteriorated as delivery times slowed again while the employment index moved back into the contractionary territory.

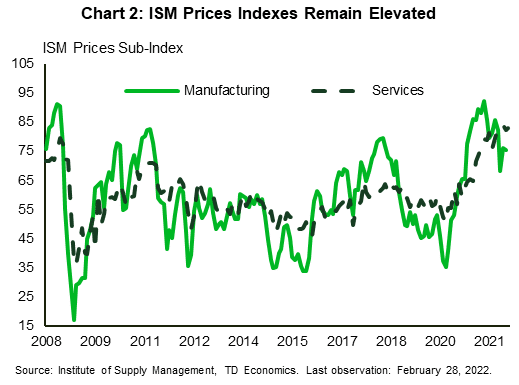

The price sub-indexes remained elevated, although price pressures seem to track lower in the manufacturing sector, while services continue to struggle with a reading above 83 (Chart 2). Despite these differences, there is little doubt that next week’s CPI reading will come in much higher than the 2% target. With the threat of higher prices becoming more entrenched, the Fed is unlikely to hesitate to raise the fed funds rate by 25 basis points on March 16th.

Meanwhile, Russia’s invasion of Ukraine has reverberated through financial markets, lifting a key measure of volatility to the highest level in more than a year. Although the U.S. trade dependency on Russian and Ukrainian products is limited to less than 1% (according to the World Bank), the U.S. economy may suffer through other channels. The conflict has already resulted in the biggest weekly surge in commodity prices since 1974, and threatens to exacerbate pandemic-induced logistical challenges in financial news. Both of these forces will lead to higher prices, and a drag on economic growth. Meanwhile, further deterioration in financial conditions would be equivalent to monetary tightening, which could force the Fed to slow down the speed of rate hikes in the future.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.