Financial News Highlights

- Inflation eased modestly in April, with headline and core CPI both ticking down by 0.1 percentage points to 4.9% and

5.5% year-on-year respectively. - The Federal Reserve’s Senior Loan Officer Opinion Survey showed that a higher share of commercial banks tightened

credit conditions in April than January. - A meeting between President Biden and Congressional leaders failed to yield any progress on negotiations to raise/suspend

the debt limit.

Inflation Continues to Cool in Earnest

On the heels of last week’s FOMC meeting, we were provided with a host of economic data this week to assess the Fed’s new wait-and-see approach, including April’s CPI report in financial news. In addition, we also received the second quarter Senior Loan Officer Opinion Survey (SLOOS) and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.

On the heels of last week’s FOMC meeting, we were provided with a host of economic data this week to assess the Fed’s new wait-and-see approach, including April’s CPI report in financial news. In addition, we also received the second quarter Senior Loan Officer Opinion Survey (SLOOS) and had a meeting between President Biden and Congressional leadership as they attempt to find an agreement to raise the debt limit. Markets ended the week relatively unchanged, with the S&P 500 down 0.1% and the ten-year Treasury Yield down 4bps at 3.41% as of the time of writing.

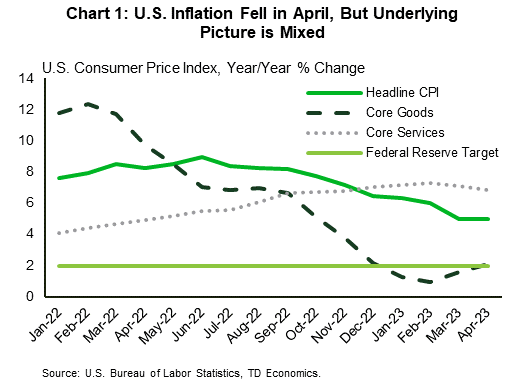

Inflation eased modestly in April, as headline inflation rose by 4.9% year-on-year, down modestly from 5% in March (Chart 1). Energy prices rose for the first time in three months as gasoline jumped by 3% month-on-month (m/m), and food prices were flat for a second consecutive month. Stripping out energy and food, core inflation ticked down to 5.5% y/y, having fluctuated between 5.5-5.6% y/y since January in financial news. While we did see shelter inflation decelerate for a second consecutive month, it still rose by 0.4% m/m. This in addition to the reacceleration in core goods inflation, worked to keep core inflation elevated. Although on aggregate this report had positive developments, it reiterated the fact that the path back to the Fed’s 2% target is unlikely to be a straight line.

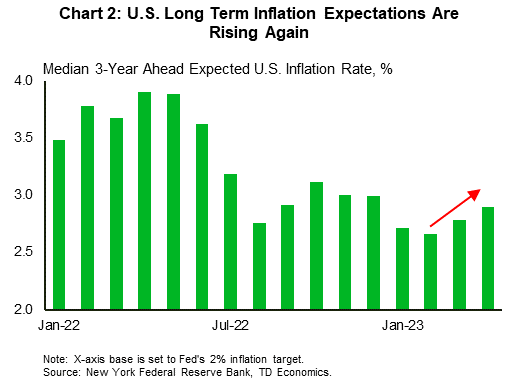

Of particular concern for the Fed is the potential for inflation expectations to become de-anchored. In the New York Fed’s Survey of Consumer Expectations this week, we saw three-year ahead inflation expectations rise for a second consecutive month to 2.9% in April (Chart 2). While this series has historically run slightly above the Fed’s 2% target, a sustained movement above 3% would be a concern for the FOMC.

Earlier in the week, we saw that U.S. commercial banks continued to tighten credit conditions in April in the Fed’s SLOOS. Commercial & industrial loans as well as commercial real estate (CRE) loans saw a higher net percentage of banks tightening credit standards than in January. Demand for these loans from businesses fell as a result, however household demand for consumer-facing loans (mortgages, auto, credit card, etc.) rose as credit remained relatively accessible. Further analysis of the SLOOS can be found here.

Earlier in the week, we saw that U.S. commercial banks continued to tighten credit conditions in April in the Fed’s SLOOS. Commercial & industrial loans as well as commercial real estate (CRE) loans saw a higher net percentage of banks tightening credit standards than in January. Demand for these loans from businesses fell as a result, however household demand for consumer-facing loans (mortgages, auto, credit card, etc.) rose as credit remained relatively accessible. Further analysis of the SLOOS can be found here.

Lastly, in the Oval Office this week, President Biden met with Congressional leaders on Tuesday to attempt to find an agreement to raise/suspend the debt limit. Treasury Secretary Yellen warned last week that the Treasury could run out of funds by early June, thus the impetus to reach an agreement is elevated. However, no progress has been made in the negotiations so far.

Looking ahead to next week, we will get a fresh update on the U.S. consumer with April retail sales as well as existing home sales. With the unemployment rate back down to 3.4% consumers may still have some wind in their sails, but we expect that this will be short-lived as past rate hikes continue to filter through the economy.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.