FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Equity markets rebounded this week as the U.S. administration delayed its decision on auto tariffs for six months.

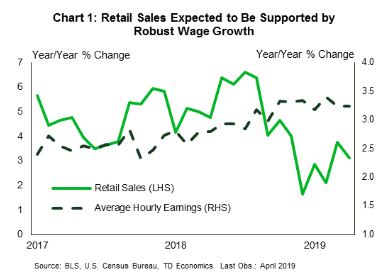

- Housing starts and retail sales data for April support the narrative of healthy domestic spending this quarter.

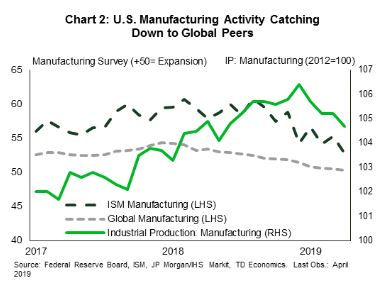

- That said, externally oriented industries appear to be getting caught in the downdraft of weak foreign demand.Formerly resilient, U.S. manufacturing activity has softened this year, in line with global developments.

Domestic Resilience, But Weakness Abroad Taking a Toll

Unease about U.S. economic performance is building for good reason. Economic growth is set to moderate this year after a blowout, stimulus-fueled 2018. Foreign demand remains weaker than last year, while geopolitical risks and trade policy uncertainty appear to be on the rise. Moreover, high frequency indicators are beginning to diverge. Domestic demand remains resilient, but externally oriented industries are combatting stronger headwinds.

Data for retail sales and housing starts for April support the view that the domestic economy remains healthy. Although retail sales pulled back in

Housing starts, on the other hand, surprised to the upside. After December’s dip, housing starts appear to have regained stronger footing, but activity has been choppy through April. Home builder sentiment is improving as well, reaching a 7-month high in May. Moderating home price growth, combined with lower mortgage rates, rising wage growth, and decades-low vacancy rates should support more homebuilding in the months to come.

All told, the data this week remains consistent with our forecast for the U.S. economy to expand at a 2% annualized pace this quarter, largely on the back of a more confident consumer. That said, signs continue to build that this may be as good as things get for the rest of this year. Cracks are beginning to appear in what was previously a very resilient manufacturing sector. Industrial production contracted 0.5% in April, the third contraction monthly contraction this year. This mirrors the declining pace of output reported in the ISM manufacturing survey (Chart 2). Softer auto sales are partly to blame, as motor vehicle assemblies have fallen 12.8% since December’s peak.

Although manufacturing is a relatively small share of the U.S. economy (about 11%), its performance is still considered a harbinger of the direction of the U.S. economy largely due to its sensitivity to changes in foreign demand. On that front, there are some signs that the global economy is gradually improving. However, escalating trade and geopolitical risks threaten to derail this nascent recovery.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.