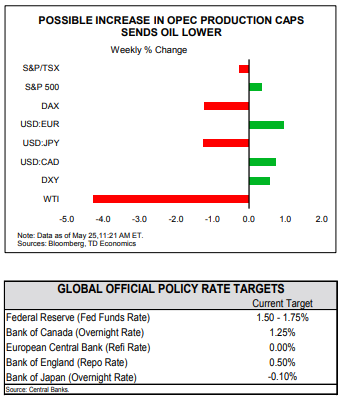

HIGHLIGHTS OF THE WEEK

- U.S. trade tensions with China have temporarily subsided, however they have flared up elsewhere, as President Trump ordered a review of U.S. automotive imports.

- Trade tensions were also flagged as a key risk in the latest FOMC minutes. However, the Committee remained in agreement that it would soon need to “take another step” in removing monetary accommodation.

- Falling affordability and lack of inventory, continued to weigh on the U.S. housing market activity. After a weak first quarter, existing home sales have started the second quarter on a weak footing, falling 2.5% in April. Sales of new homes also declined during the same month.

Markets Respond to Geopolitics and the Fed

Financial markets rallied on Monday on the news of positive weekend developments in the U.S.-China trade dispute. Details of the agreement were vague and largely unquantifiable as far as trade deficit reduction targets are concerned. In the follow-up statement China agreed to “meaningfully” increase imports of U.S. agricultural and energy products, and lowered tariffs on imports of autos and parts. These relatively limited concessions were sufficient to put the proposed tariffs on $50 billion worth of Chinese goods set to take effect on May 21 on hold.

Although U.S. trade tensions with China have eased for now, they have flared up elsewhere, weighing on market sentiment later in the week. On Wednesday President Trump ordered a review of automotive imports, citing national security concerns. The decision drew sharp international criticism and warnings of retaliatory tariffs, but was also opposed domestically. Automakers as well as Republican lawmakers expressed concerns that, if imposed, auto tariffs will raise auto prices for consumers, disrupt supply chains, start trade wars and alienate U.S. allies.

Higher interest rates will certainly have an impact on the housing market. After declining by 6% in the first quarter, existing home sales have started the second quarter on a weak footing as activity fell 2.5% in April. Sales of new homes also took a break in April, declining by 1.5%. Since the start of the year, the average rate on a 30-year mortgage rose by 70 basis points. Rising rates alongside brisk growth in home prices have dented affordability; however, this is only part of the story behind relatively tepid home sales. Low inventory of houses on the market has been the most important factor restraining resale activity (Chart 1), but the pace of construction remains modest and will likely be contained by labor shortages and rising input costs. The price of American steel rose 40% this year, while lumber prices are up 34%. Some relief to the housing shortage may come as more existing homeowners, with fully rebuilt home equity (Chart 2), become encouraged to list their homes. However, the overall pace of activity in the housing market will likely once again remain modest this year.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.