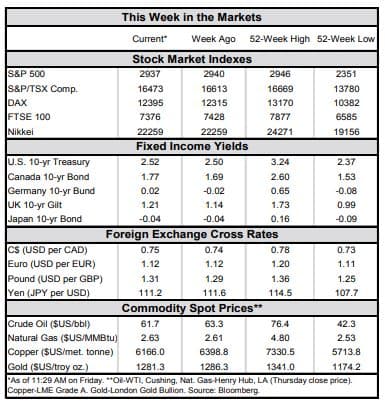

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Apart from vehicle sales, recent data paint a positive narrative for consumer-related industries at the start of spring. Real consumer spending and pending home sales surged in March, while consumer confidence improved in April.

- Payrolls were up 263k in April, much better than expected; wage growth held steady at 3.2% y/y and the unemployment rate fell to a near-50 year low of 3.6%. A drop in the labor force participation rate assisted the latter.

- The Fed held rates steady this week, with an emphasis put on inflation running below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is no strong case “for moving in either direction”. Indeed, for now, all of the tea leaves suggest that the Fed will remain on hold for some time.

U.S. – Q1 Growth Surge Shakier Underneath The Hood

While the consumer had a soft showing overall in the first quarter, a two-month data dump this week provided added detail on recent momentum. Real consumer spending was flat in February, before surging 0.7% in March. This spending upswing points to consumers shaking off the adverse effects of the prolonged government shutdown, and provides a solid handoff to consumption in the second-quarter.

The (mostly) positive narrative on consumer-related industries at the start of spring was further bolstered by a 3.8% m/m surge in pending home sales in March and a pickup in consumer confidence in April. The former leads existing home sales by 1-2 months, and points to further stabilization in the housing market. However, vehicle sales were disappointing, falling 6% m/m in April to 16.4M units. Despite this, overall consumer spending is still tracking a 3% annualized pace in the second quarter, a sharp acceleration from the 1.2% clip in the first quarter. This will provide support to overall economic activity as other temporary factors that boosted growth in the first quarter fall off.

Rounding out the April data reports were the ISM indices. Both moderated on the month but continue to hover around the 55-point mark, which is in tune with the broader narrative of slower, but still decent, growth this year.

With the labor market and economic growth not looking too shabby, inflation remains the Fed’s key concern and main reason for holding rates steady, as it did this week. The FOMC statement emphasized that inflation has run below target. But in the press conference, Fed Chair Powell noted that inflation was driven down by “transient” factors, adding that there is currently no strong case “for moving in either direction”. We agree with the Fed’s assessment. Given that inflation has persistently undershot the Fed’s target, it would take a notable acceleration in price pressures to push the Fed to hike. We do not expect inflation to accelerate that quickly, and all of the latest data support our view that the Fed is likely to remain on hold for quite some time.

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.