Financial News Highlights

- Minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working in financial news.

- Existing home sales sag as high prices and financing costs make homes their least affordable since the mid-80s.

- All eyes will be on next week’s personal income and spending report for October, watching for further signs of slowing demand growth.

Looking for Signs of Slowing

U.S. Treasury yields extended their decline this week, with the 10-year now hovering around 4.5% in financial news. As economic data have decelerated, expectations for policy easing next year have helped markets continue to rally – up about 1% this week. This week, minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working, while housing starts data showcased that higher interest rates are working to cool the economy. Coming off the Thanksgiving holiday, all eyes are now tuned to next week’s consumer spending report for October for signs of slowing economic momentum and cooling inflation.

U.S. Treasury yields extended their decline this week, with the 10-year now hovering around 4.5% in financial news. As economic data have decelerated, expectations for policy easing next year have helped markets continue to rally – up about 1% this week. This week, minutes from the Federal Open Market Committee (FOMC) meeting reinforced the Fed’s messaging that patience is warranted while the disinflation process is working, while housing starts data showcased that higher interest rates are working to cool the economy. Coming off the Thanksgiving holiday, all eyes are now tuned to next week’s consumer spending report for October for signs of slowing economic momentum and cooling inflation.

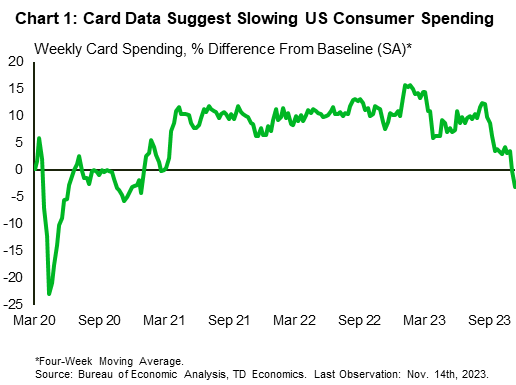

The minutes from the FOMC’s last meeting essentially backed up the hawkish signals the Fed has been putting out while they hold the policy rate fixed. Committee members noted how the economy stayed unexpectedly hot through the third quarter of the year, powered by relentless consumer spending. With the supply shocks from the pandemic and the war in Ukraine still gradually resolving themselves, persistently strong aggregate demand helped keep pressure on prices through much of the year. However, committee members judged that this may be starting to shift (Chart 1). This has left the Fed squarely focused on cooling demand to tame inflation pressures. On this front, the Fed maintains that restrictive policy rates are working, and are at an appropriate level. Moreover, with members agreeing that there needs to be clear evidence that inflation is on a solid trajectory back to 2% before easing, and upside risks ever-present, officials will be keenly looking out for any signs that more needs to be done to restore the supply-demand balance.

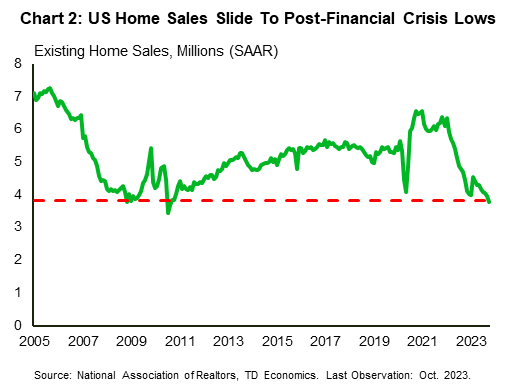

On the demand side, the housing market is clearly responding to the surge in borrowing costs since the summer, with existing home sales in October falling to their lowest level since 2010 (Chart 2). However, conditions today are drastically different than in 2010, when the housing bubble burst leading to an abundance of supply, and a tepid recovery after the Global Financial Crisis saw a drastic improvement in affordability. Today, affordability is weighing on activity as high prices and financing costs make homes their least affordable since the mid-80s. With the Fed poised to keep rates at multi-decade highs, a quick turnaround is unlikely.

On the demand side, the housing market is clearly responding to the surge in borrowing costs since the summer, with existing home sales in October falling to their lowest level since 2010 (Chart 2). However, conditions today are drastically different than in 2010, when the housing bubble burst leading to an abundance of supply, and a tepid recovery after the Global Financial Crisis saw a drastic improvement in affordability. Today, affordability is weighing on activity as high prices and financing costs make homes their least affordable since the mid-80s. With the Fed poised to keep rates at multi-decade highs, a quick turnaround is unlikely.

However, with healthy economic momentum through the third quarter all eyes will be on next week’s consumer income and spending report for signs of slowing demand growth. With payrolls growth slowing in October, consensus expectations are for real consumer spending growth to slow from 0.4% month-on-month (m/m) in September to 0.1% in October. The Fed’s preferred inflation measure, the core PCE deflator, is expected to follow suit, slowing to 0.2% m/m from 0.4% in September.

Of course, given the experience of the past year, the risks run to the upside, and that the American consumer will once again prove to be more resilient than expected. In that event, the Fed has told us it stands ready to tighten policy further if they assess that data show, “progress toward the Committee’s inflation objective was insufficient.”

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.