Financial News Highlights

- The government shutdown continues through its second week, with no clear end in sight, while trade tensions between the U.S. and China have suddenly heated up.

- Absent official data, the market is turning to imperfect private-sector alternatives, which suggest the labor market continued to cool in September.

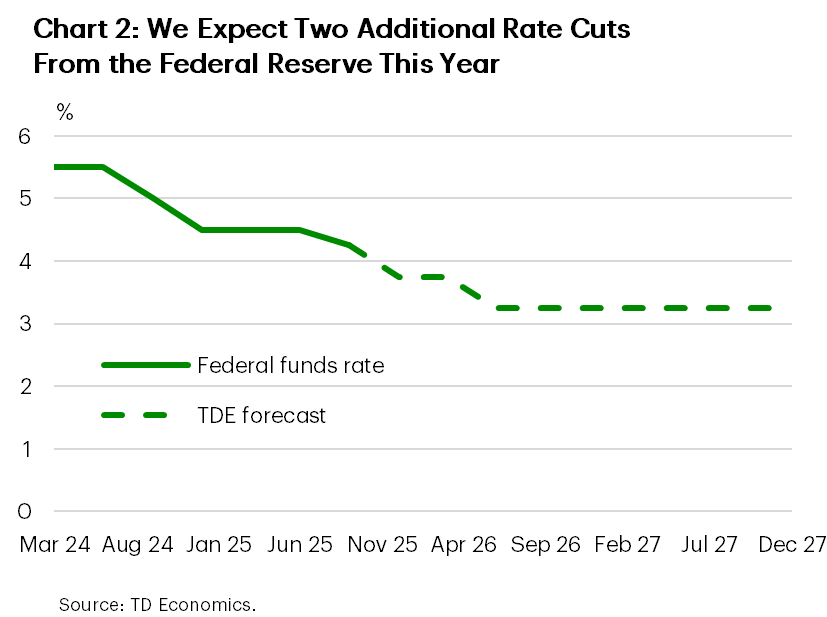

- We don’t see any developments this week that are likely to cause a big shift in the perception of the economy or the outlook, and so we are still penciling in two more quarter-point rate cuts from the Federal Reserve by year-end.

No Data, No Problem

Up until Friday, markets had been relatively calm amid the ongoing government shutdown, which has entered its 10th day. President Trump’s threat to increase tariffs on China this morning, in response to China’s export controls on rare-earth metals, has upended that. President Trump has gone so far as to declare he is not interested in meeting President Xi in person as previously scheduled for the end of the month, leading to a sharp sell-off in US equities and pushing Treasury yields lower. Markets stoically withstood the failure of seven separate proposals to re-open the government, but the possible breakdown of U.S.-China trade negotiations may be too much to bear. If that wasn’t enough, the end of the shutdown is not clearly in sight. The Senate is now adjourned until October 14, which all but guarantees that military members will miss a full pay cycle, an unprecedented development.

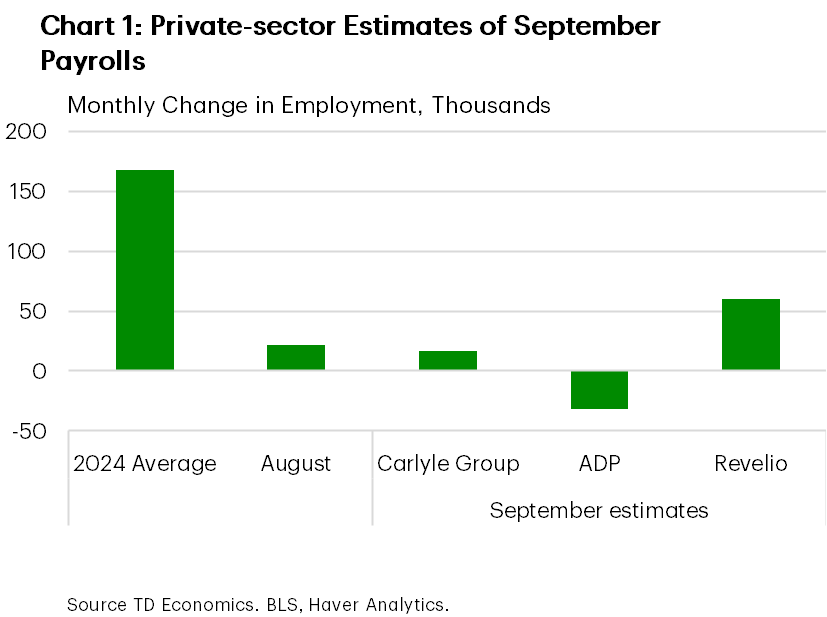

The outlook for the shutdown is not the only thing that is cloudy. The government shutdown means that official economic data are not being published, and policymakers, businesses, and households are unable to see new data on the state of the economy. Various private-sector groups have produced estimates of what happened to employment in September, shown in Chart 1. This was the key piece of data which was due to be published last Friday. While these alternative estimates generally suggest the labor market continued to cool through September, these measures are at best imperfect proxies for the official data. As for what data we do have this week, the preliminary reading of the University of Michigan’s consumer confidence ticked a touch higher in October. However, expectations on the future outlook continued to slide for a third consecutive month, likely driven by the softening labor market and still elevated uncertainty on trade policy.

Several members of the FOMC spoke this week, offering some insight into their thinking amidst the shutdown. New York Fed President Williams indicated that the lapse in government data would not deter him from further easing the policy rate at the Fed’s coming meetings. Meanwhile, other speakers continued to reiterate prior views. Kansas City Fed President Schmid voiced concern about inflation, while Miran, the only FOMC member to vote for a larger 50 basis point rate-cut at the last meeting, again indicated how he expected inflation to moderate. It is little surprise that market pricing at the next Fed meeting has remained relatively unchanged through the government shutdown. Expectations for further easing at a moderate pace are in line with the general view we observed in the FOMC minutes released this week, that interest rates are currently moderately restrictive and risks have shifted somewhat to the downside.

Normally, we would be looking ahead to next week’s release of CPI for more information on how prices are reacting to tariffs, but we are following the shutdown. We will also be closely watching trade negotiations between the U.S. and China to see what comes of today’s escalation.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.