Financial News Highlights

- U.S. bond yields retreated from highs reached last week, as heightened geopolitical risks in the Middle East boosted investors demand for safe haven assets in financial news.

- However, the recent overall surge in yields has prompted some Fed members to pay closer attention to tightening financial conditions as they determine the most appropriate policy path for interest rate.

- Both producer prices and consumer prices suggest that the Fed still has some work to do to ensure inflation gets back to target, even as core prices continue to moderate.

Goodbye “How High”, Hello “How Long”

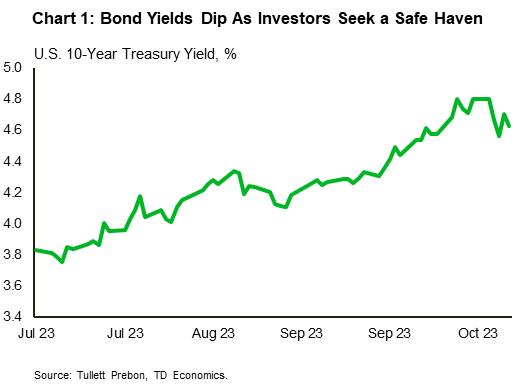

Last week’s tight financial conditions abated a bit this week, as conflict in the Middle East boosted demand for safe haven assets. As such, the 10-year Treasury yield took a reprieve from its upward trek and at the time of writing was down 17 basis points (bps) relative to the end of last week (Chart 1). Nonetheless, yields are still up 76 bps since July 26 when the Fed last raised the policy rate. Several factors have contributed to rising bond yields over the past few months including expectations of higher for longer interest rates and concerns about energy supply and prices.

Last week’s tight financial conditions abated a bit this week, as conflict in the Middle East boosted demand for safe haven assets. As such, the 10-year Treasury yield took a reprieve from its upward trek and at the time of writing was down 17 basis points (bps) relative to the end of last week (Chart 1). Nonetheless, yields are still up 76 bps since July 26 when the Fed last raised the policy rate. Several factors have contributed to rising bond yields over the past few months including expectations of higher for longer interest rates and concerns about energy supply and prices.

The relatively higher yields have prompted some Fed officials to acknowledge that higher longer-term yields may be helping to achieve their policy objective. Dallas Fed President Lorie Logan remarked that “if long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed-funds rate.” Similar sentiments were echoed by Fed governor Christopher Waller who said that “financial markets are tightening up and they are going to do some of the work for us”. Fed Vice Chair Philip Jefferson said that he would “remain cognizant of the tightening in financial conditions through higher bond yields” when assessing the path for interest rates. That sentiment was also echoed by Minneapolis Fed president Neel Kashkari.

The minutes released from the Fed’s September meeting revealed that, prior to the most recent run-up in bond yields, a “majority” of FOMC participants believed that another rate increase might be appropriate, while only “some” viewed no further increases as necessary. The tone of the minutes, economic projections and policy guidance was hawkish with Fed members expecting rates to be kept higher for even longer. This was reflected in a shallower path of expected rate cuts (FOMC commentary).

Additionally, “several” participants commented that the Fed’s focus should be transitioning to how long to maintain restrictive policy, rather than how high to raise rates. Ultimately, all participants were in favor of maintaining restrictive policy for some time to ensure that inflation remains on a sustainable path downwards.

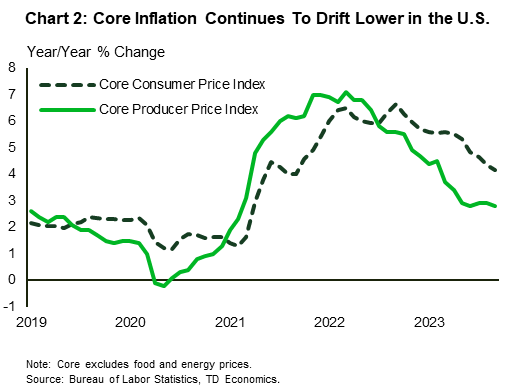

Both headline measures of producer prices (PPI) and consumer prices (CPI) show that the inflation battle is not quite over. On a yearly basis, PPI accelerated in September, while CPI held steady. The movements largely reflected gains in food and energy prices. Stripping out these volatile segments, core prices for both measures edged lower (Chart 2). While the downward tilt to core prices is sure to be welcomed by the Fed, rates are still too high for comfort given that near-term inflation expectations have inched higher in recent months and the labor market remains resilient.

American small businesses are also feeling less optimistic as expectations regarding the economic outlook and credit conditions deteriorated in September. Several firms noted that the Fed’s aggressive hiking campaign is weighing on credit with a net 26% of borrowers reporting paying higher interest rates versus three months ago. Nonetheless, the Fed will need to see a meaningful cooling in the jobs market and a sustained reduction in inflation, before shifting policy stance. As such, higher for longer may be around for some time.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.