FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Covid-19 infections are surging in much of the world, prompting new restrictions in Europe and dampening market sentiment early in the week.

- U.S. data painted a clear picture of pandemic life. Inflation pressures for services hard hit by social distancing have cooled notably.

- Meanwhile, American consumers continue to snap up goods that will help them to enjoy life at home. That strength in September retailing put markets in a better mood late in the week.

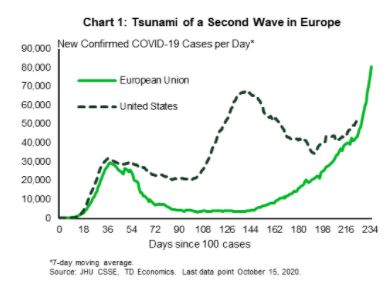

U.S. – Global Infections Surge

Earlier in the week, the IMF released their updated global forecast. It emphasized that the recovery will be long, uneven and uncertain. Their forecast contraction for 2020 (-4.4%) is slightly smaller than expected back in June, but the rebound is also shallower. So long as the pandemic is controlled next year, it expects the global economy to rebound 5.2%. Unfortunately, at the moment in many areas of the globe, the pandemic is far from controlled.

Infections have been on the upswing in Europe, where daily infections are well above their spring peaks, and have recently surpassed the U.S. (Chart 1). As a result, countries have imposed new restrictions to turn the tide, from curfews in France’s largest cities, to curbs on socializing indoors in London. New restrictions are more targeted relative to the spring, and therefore, the economic impact is likely to be much less severe. However, it still casts a pall over the outlook for Europe.

In the U.S., the latest inflation report should quiet the stagflation chatter that had emerged after a couple of hot months for core inflation. Both headline and core CPI rose a middling 0.2% in the month of September. However, removing an outsized 6.7% month/month increase in used vehicle prices leaves core inflation flat on the month.

The good news came from consumers, who ramped up their spending at retailers in September. Retail sales rose 1.9% on the month, driven by a big jump up in clothing purchases (+11% m/m), department stores (+9.7% m/m), sporting goods, hobby, book and music stores (+5.7% m/m) and vehicle sales (+3.6% m/m). There is some speculation that the strength in clothing may be due to the delayed back-to-school in many parts of the country. Even removing that influence, it was a strong month, and puts some upside risk to our forecast for consumer spending in the third and fourth quarter.

Like price patterns, the trend in retail sales also tells the tale of pandemic life (Chart 2). The hardest hit area is restaurants and bars, which have faced closures and restrictions. Since most consumers are staying home a lot more, there is also less of a need to get dressed up to go out, and even with September’s jump, clothing sales are below their pre-crisis level, as are department stores which would include a fair amount of clothing purchases. The strongest areas, apart from online shopping in general, are for things that make staying home a bit more appealing, such as new gym equipment or other hobbies and materials for home and garden improvement projects.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.