FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

- Covid-19 infections continued to rise this week, nearing record highs set in July. Concerns regarding this trend weighed on markets, but progress on a new stimulus package helped improve the mood later in the week.

- Positive housing reports reinforced the sector’s position as a bright spot in the U.S. economy. Existing home sales soared 9.4% in September, blowing expectations out of the water, while price growth accelerated further.

- Fast-rising prices are good news for builders who have recognized the need to build more homes. Housing starts also pushed higher in September (+1.9%), with gains concentrated in the single-family segment.

U.S. – Housing Market Remains A Bright Spot

The September existing home sales report reinforced the notion that the housing market remains a bright spot, even as most sectors of the economy continue to struggle under the weight of the pandemic. After gains moderated in the two months prior, resale activity surged by 9.4% in September, blowing expectations out of the water. Sales are now at a new post-Great Recession high and nearly 14% above their pre-pandemic level (Chart 1). Details from the report suggested that the purchasing of homes in vacation destinations – a trend that appears to have been supported by an improved flexibility of working from home – played a part in boosting overall sales. While the latter are up 21% year-over-year (y/y), sales in vacation destination counties accelerated over the summer and are up 34% y/y according to the National Association of Realtors.

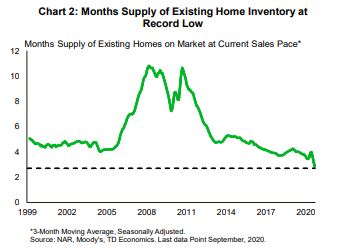

With low mortgage rates and a still-improving labor market, we expect resale activity to continue grinding higher, but at a more moderate pace. A sharp acceleration in home price growth is eroding affordability and a record-low supply of housing means that markets will remain tight. Housing inventory now sits at just 1.47 million or a record low of 2.7 months at the current sales pace (Chart 2). As a result, the median existing home price has accelerated to a sharp 15% y/y – the fastest pace since the “frothy” days of 2005.

The few remaining indicators pointed to a slowing economic recovery outside housing. Initial jobless claims fell by 55k to 787k last week – better than expected, but still slightly higher than at the start of the month. Meanwhile, continuing claims from all programs eased to a still-elevated 23.2 million at the start of the month (data is delayed). Anecdotal evidence from the Beige Book also pointed to a “slight to modest” pace of growth this fall. Coupled with the fact that the virus’ spread is nearing a record high, these elements support the case for added fiscal stimulus.

The outcome of the election, which is now a little over a week away, will have important implications for the economy (see here) and the amount of fiscal stimulus. So far, Joe Biden is leading in the polls. But, judging from what happened in 2016, it’s worth continuing to take these numbers with a grain of salt.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.