Financial News Highlights

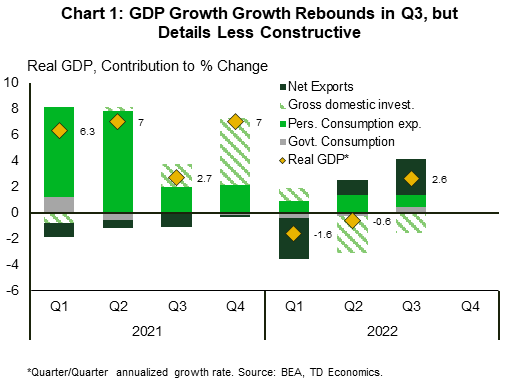

- The U.S. economy left behind the declines recorded in the first half of 2022, with GDP growth accelerating to 2.6% (ann.) in the third quarter. The headline was flattered by an outsized contribution from net exports, whereas private domestic drivers remained soft.

- The weakest area of the third quarter GDP report was residential investment, which fell 26% (ann.). Outside of the pandemic, this was the sharpest pullback since 2010.

- With mortgage rates currently topping 7%, there’s more weakness in the cards for housing. Pending home sales, a leading indicator of existing home sales, fell for the fourth consecutive month by a massive 10.2% m/m in September.

Fed’s Preferred Inflation Gauge Remains Hot

U.S. Treasury yields trended lower this week as investors digested mixed signals from the economy and earnings reports in financial news. The 10-year yield has fallen to around 4% as of writing after topping 4.3% late last week. Equities were trekked higher, with the S&P 500 looking to end the week up about 2.9% as at the time of writing.

U.S. Treasury yields trended lower this week as investors digested mixed signals from the economy and earnings reports in financial news. The 10-year yield has fallen to around 4% as of writing after topping 4.3% late last week. Equities were trekked higher, with the S&P 500 looking to end the week up about 2.9% as at the time of writing.

The U.S. economy left behind the negative prints recorded in the first half of the year, with growth accelerating to 2.6% annualized (ann.) in the third quarter – a touch higher than market expectations (2.3%). However, the headline number was flattered by an outsized gain in net exports (Chart 1). Meanwhile, private domestic drivers were largely unchanged, adding only 0.1 percentage points (pp) to headline growth – down from 0.5 pp in the second quarter. Consumer spending remained supportive, but its contribution to growth diminished in light of elevated inflation and a higher interest rate environment. Consumers continued to tap into the pent-up demand for services (up 2.8% ann.), while pulling back on goods – declined by 1.2%.

The weakest area weighing on domestic demand was residential investment, which fell 26% (ann.), marking the sixth consecutive quarterly decline. Outside of the pandemic, this was the largest quarterly decline since the start of 2010. The outsized pullback was the result of sharp declines in homes sales and residential construction through the third quarter, as higher interest rates have tighten the grip on the housing sector.

Housing is one of the most interest-sensitive areas of the economy and with rates elevated – with the 30-year fixed mortgage rate currently sitting at 7.1% – it is likely that there will be more weakness over the coming months. Several recent indicators support this view. Pending home sales, a leading indicator of existing home sales, fell by a massive 10.2% m/m in September. Meanwhile, mortgage applications to purchase a home dropped 2% last week from the week prior and were 42% lower than a year ago.

Housing is one of the most interest-sensitive areas of the economy and with rates elevated – with the 30-year fixed mortgage rate currently sitting at 7.1% – it is likely that there will be more weakness over the coming months. Several recent indicators support this view. Pending home sales, a leading indicator of existing home sales, fell by a massive 10.2% m/m in September. Meanwhile, mortgage applications to purchase a home dropped 2% last week from the week prior and were 42% lower than a year ago.

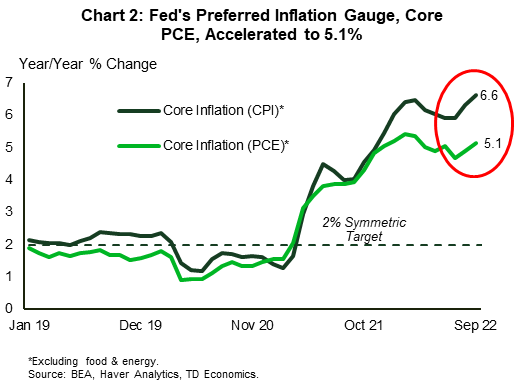

The housing market is also central to the Fed’s rate setting calculus. Market data tells us that rent growth is decelerating and that home prices are falling. However, as we explain in a recent note, market price changes take time to filter down to their corresponding inflation metrics, which means that shelter inflation is likely to continue to push up on core inflation over the next several months in financial news. This may be less of an issue for the Fed’s preferred inflation gauge, Core PCE – which accelerated to 5.1% Y/Y in September (Chart 2) – where shelter carries a lower weight than CPI (see here for differences). However, CPI gets released ahead of PCE, grabbing the market’s focus and adding to the Fed’s communication challenge.

The bottom line is that if the Fed does not pivot toward a more forward-looking stance, the result will be a more restrictive monetary policy than otherwise required, increasing the chances of a policy ‘error’. While the Fed will likely deliver on another 75-basis point hike next week, we expect the FOMC to soon start to pivot on its communication as the Fed will need to dial back on the pace of rate hikes.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.