Financial News Highlights

- The U.S. economy added 187k jobs in August, but revisions to the two prior months subtracted a notable 110k jobs from the previous reported tally.

- Both total and core PCE inflation rose by 0.2% month-on-month in July, equal to the monthly change seen in June for both measures.

- Hurricane Idalia, the first of the season to make landfall in the U.S., caused widespread flooding and wind damage through Florida’s Big Bend region and up through Georgia and the Carolinas.

The Labor Market Takes a Holiday

The U.S. almost managed to escape August without a major hurricane, but unfortunately those hopes were dashed when Hurricane Idalia made landfall as a category 3 hurricane on Wednesday in Florida in non financial news. Strong winds, rain, and storm surges caused widespread flooding and property damage, leaving hundreds of thousands of Americans without power across the Southeast. Although the extent of the damage is still being assessed, insurance and clean-up costs are expected to be well over a billion dollars.

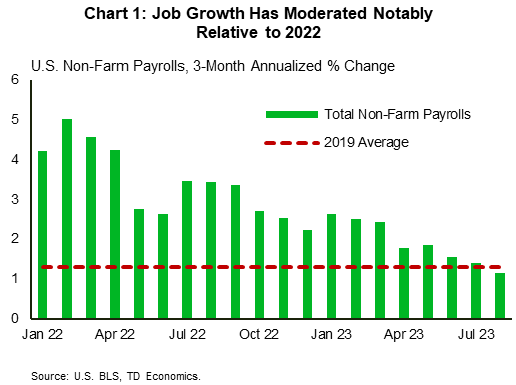

Fortunately for the national economy, sunnier skies could be found in this week’s economic data, including the 187k new jobs added in August. While this reading, in addition to the downward revisions to the previous two months, marks a continued moderation in the pace of hiring, it indicates that supply and demand in the labor market are coming into a more sustainable alignment (Chart 1). This was further evidenced by the decline in job openings in July, with the job opening to unemployed ratio falling to 1.5 in financial news. While the unemployment rate did rise to 3.8%, this mostly resulted from a boost in labor force growth which could be considered a net positive if it helps to offset labor shortages. On aggregate, this progress will come as positive news for the Federal Reserve, however the most recent data on inflation was slightly more mixed.

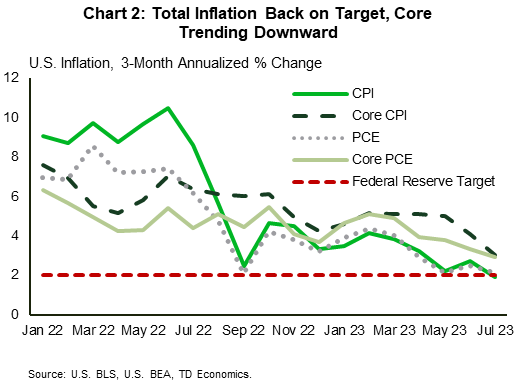

On Thursday, we saw that PCE inflation rose by 3.3% year-on-year (y/y) in July, up from 3.0% in June. This was driven by a moderation in the negative base effects resulting from the spike in energy prices last year in addition to a moderate uptick in services inflation – driven entirely by Powell’s ‘supercore’ component. Looking at the 3-month annualized trend (Chart 2),  we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

we can see that total inflation is pushing closer to the Fed’s 2% target, though this is likely to be short lived given the recent move up in energy prices. In addition, while core inflation is moving in the right direction, non-housing core services have barely budged from their cyclical highs and continue to run at an elevated annualized pace. Until we see a meaningful cooling here, core inflation will likely remain north of 3%.

Some offset to inflationary pressures continues to be provided by the goods sector, with the ISM Manufacturing Purchasing Managers’ Index (PMI) showing manufacturing activity contracted for a tenth consecutive month in August. Ten out of sixteen industries reported lower input prices, which is likely factoring in downstream to the consumer. Price growth in the services sector has been more stubborn, so next week’s update on the ISM Services PMI will offer insight into how resilient the sector remains.

With the Labor Day holiday on Monday, next week will be short both in length and in the volume of economic data that we receive. However, the release of the Fed’s Beige Book will be one item to watch, as it will feed into the viewpoints that FOMC members bring to the upcoming meeting. We expect that the progress on inflation and job market cooling up to this point will be sufficient to warrant a hold in 2 weeks’ time, but the tone will likely remain hawkish to guard against the potential for pre-mature easing in financial conditions.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.