FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A wide dispersion of forecasts for U.S. growth over the next year reflects high levels of uncertainty around the duration of the health crisis as well as future government supports.

- Assuming a modest fiscal package passes Congress this fall and a vaccine becomes available by the middle of next year, the American economy should recover most of what was lost through the pandemic by the end of 2021.

- Inflation data showed an acceleration in price growth in August. Total CPI was up 1.3% year-on-year in August, continuing its recovery from only 0.1% in May.

A Wide Dispersion of Expectations for Recovery

This wide dispersion reflects the unprecedented level of uncertainty around the course of the pandemic, as well as its secondary economic impacts. This can be seen in the wide array of underlying assumptions among forecasters around items key to the outlook. For example: when and if a vaccine becomes available, how effective and permanent it will be, how much future government support will be provided.

We do not claim to have any better insight on these questions than other forecasters, but we have tried to make plausible assumptions to ground our forecast. In the case of the health questions, we assume that a vaccine or effective treatment becomes widely available by the second half of 2020.

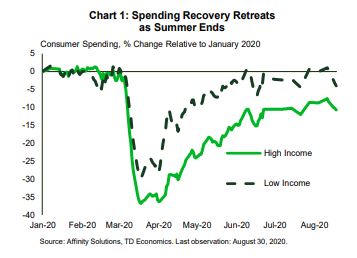

Beyond the basic uncertainty around when and if we recover fully from the pandemic, we have little in the way of traditional macro models to gauge how consumers and businesses respond to health crises. This was true on the way down, but also on the way up. We can observe, based on recent data, that after an initial plunge, households have been more than willing to increase spending on durable goods – suggesting little permanent damage to household confidence. Rather, what’s holding back a broader recovery is service-sector areas of the economy where activity is directly impacted by the potential risk of infection. This offers reason to expect a fairly solid bounce back once these fears are allayed.

With these assumptions in place, and assuming no major second wave of the virus leads to another round of shutdowns, it is reasonable to expect the American economy to recover much of what was lost to the pandemic over the past year. While growth appears likely to slow after its initial burst on reopening, it should pick up again once a vaccine is available. Importantly, much of the deficit in spending is due to high-income individuals, who should be able to dip into these accumulated saving to support growth once the virus threat has passed. As a result, we expect the level of GDP to regain its pre-recession level by the first quarter of 2022. We will be publishing our full views on the economic outlook next week and hope you will give them a read.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.