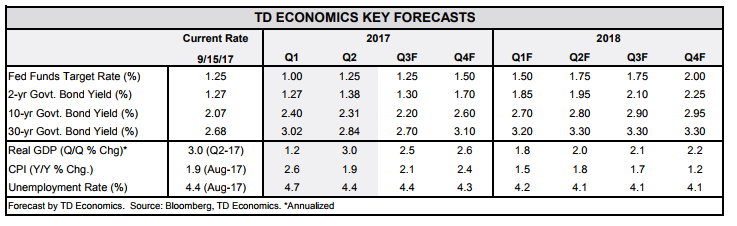

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors and analysts reading the economic tea leaves were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened.

- Consumer prices rose 0.4% (m/m) in August, pushing inflation to 1.9% (y/y) from 1.7%. A sharp rise in gasoline prices on the back of refinery shutdowns contributed to the gain. Core prices accelerated to 0.2% (m/m).

- Retail sales, on the other hand, fell 0.2% in August. With downward revisions to June and July, momentum in consumer spending has slowed heading into the third quarter relative to its blistering pace in Q2.

The Data Giveth and the Data Taketh Away

Investors and analysts reading the economic tea leaves for signals on future Federal Reserve policy were given mixed messages this week. On the one hand, inflation ticked up, but on the other, consumer spending softened. Further muddying the water, both the CPI and retail sales reports were affected by Hurricane Harvey, a phenomenon that will continue in the months ahead.

One of the chief concerns of the Federal Reserve recently has been the persistent weakness in inflation. Despite ongoing improvement in the job market and an unemployment rate comfortably below target, price growth been slowing for much of this year. Inflation according to both the overall CPI and the core measure peaked in February. Energy prices contributed to inflation early in the year, but the impact was fleeting. Moreover, the weakness in inflation cannot be attributed entirely to idiosyncratic factors. Measures that strip them out, such as median and trimmed-mean inflation, have also decelerated noticeably.

One month does not a trend make, but August may be an early sign of a reversal in this downward trend. Headline consumer prices rose 0.4% on the month, pushing year-on-year inflation to 1.9% from 1.7%. A sharp rise in gasoline prices (6.3% month-over-month) on the back of refinery shutdowns due to Hurricane Harvey contributed to the gain in the headline.

More convincing was the gain in core prices and in the aforementioned median and trimmed mean measures. Core prices rose 0.2% on the month (0.249% to be precise), the strongest gain since January. While Harvey may have had some impact on core prices, the acceleration was broad-based with both median and trimmed-mean prices accelerating noticeably (both up 0.2%).

For the Federal Reserve, evidence that inflation may finally be heading higher should provide confidence that the economy is ready for higher interest rates. However, it will also want to see signs that the economic recovery remains on track. In that regard the pullback in retail sales (down 0.2% in August) provided a cautionary note As with the CPI data, Hurricane Harvey was likely an influence, especially for auto sales, which fell 1.6% in dollar terms (units fell 4%). Nonetheless, downward revisions to both June and July suggest less momentum in consumer spending even prior to Harvey. While spending is likely to rebound as the recovery efforts from Harvey and Irma take shape, a broader-based slowdown will not go unnoticed at the Fed.

All of this comes as the FOMC is due to meet to deliberate policy early next week. The Fed appears unlikely to hike its key lending rate at this meeting, but it is likely to announce plans to gradually begin unwinding its balance sheet. These have been well telegraphed to markets with most of the impact on bond yields already priced in. More important will be how much the statement recognizes the recent moves in inflation and how this comes through in the expectations of FOMC members for future policy rates, which will be released in the Survey of Economic Projections along with the policy statement. -4 Stay tuned until Wednesday afternoon for more details.

James Marple, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.