Financial News Highlights

- The third quarter is shaping up to be the strongest of the year for the U.S. economy, with GDP tracking 3.7% q/q (annualized).

- The August reading of CPI showed inflationary pressures accelerated last month, though the trend remains favorable, with the three-month annualized change on core inflation slipping to 2.4%.

- A 1-2-3 punch of risks lies on the horizon for the U.S. economy. The end of the student debt moratorium, a potential government shutdown, and the UAW strike could all leave a mark on Q4 growth.

Flying High in Q3, But Headwinds on the Horizon

There were a lot of new data reads on the U.S. economy this week in financial news, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

There were a lot of new data reads on the U.S. economy this week in financial news, but on balance it is looking like the third quarter is shaping up to be the strongest of the year. Real GDP growth is on track for a nearly 4% q/q (annualized) pace! That performance is driven by defiant consumer spending, which is also close to 4% even though August retail sales weren’t much to write home about. The tradeoff, however, is that persistently higher demand undermines the Fed’s efforts to cool inflation. That was evident in the August CPI data, where both headline and core inflation accelerated relative to July.

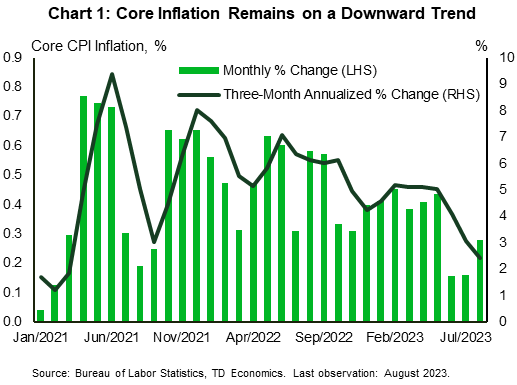

Over half of the gain in headline inflation was due to higher gasoline prices, which rose sharply alongside the recent uptick in oil prices. Meanwhile, the 0.3% m/m gain in core inflation came in a tick above expectations and bucked the trend from the ‘soft’ 0.2% gains seen in both June and July (Chart 1). However, putting these numbers in context, the monthly gain was still the third smallest in nearly two-years. Moreover, the trend on inflation remains favorable, with the three-month annualized pace cooling to 2.4% – the slowest pace of growth since March 2021.

Next week’s interest rate announcement hangs in the balance, where it is widely expected that the Federal Reserve will keep the policy rate unchanged. However, the devil will be in the details. The FOMC will also release revised economic projections, where at a minimum, they’re likely to lift the near-term growth forecast and lower the unemployment rate projection to account for the more persistent strength since the June update. The big question will be if policymakers see the near-term resilience as a source of more persistent inflationary pressures, and whether that alters the expected future path of the fed funds rate. While it is very unlikely that the FOMC would lift its terminal rate projection of 5.75% for 2023, a shallower rate cut trajectory could be signaled, reinforcing the need for rates to remain higher for longer.

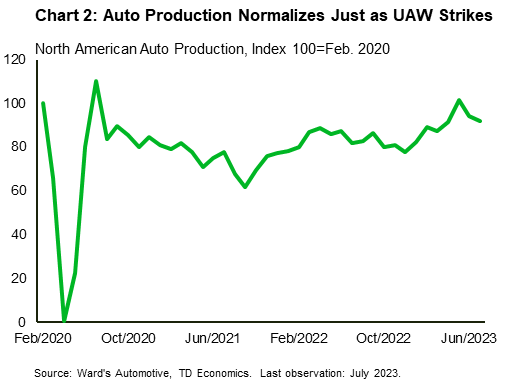

The Fed needs to thread a very small needle in its communication next week in major financial news. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

The Fed needs to thread a very small needle in its communication next week in major financial news. While policymakers will need to show a continued commitment to fight inflation, coming off too hawkish runs the risk of leading to an over tightening in financial conditions. This is particularly crucial now, as there is a trifecta of headwinds to fourth quarter growth on the horizon: the end of the student debt moratorium, a potential government shutdown, and the United Auto Workers (UAW) strike. The UAW strike, which began Thursday evening, comes just as auto production had normalized to pre-pandemic levels (Chart 2). As it currently stands, the UAW has announced work stoppages at three facilities, accounting for about 7.5% of overall U.S. production. Assuming no other stoppages, this alone would shave about 0.025 percentage points (pp) for each week the strike lasts. The hit from a government shutdown is a multiple of that, while the impact of the end of the student debt moratorium could have a cumulative Q4 hit of 0.3pp. So, while growth is flying high in the third quarter, there’s the potential it ends 2023 with a thud!

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.