Financial News Highlights

- The Fed resumed rate cuts at this week’s FOMC meeting, lowering the policy rate by 25 basis points to 4.00%-4.25%.

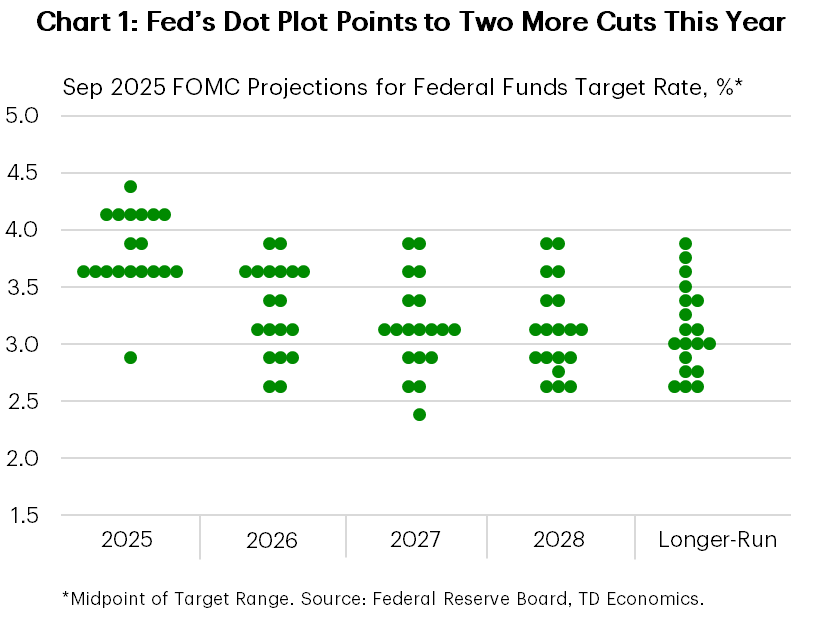

- The Fed’s “dot” plot pointed to two more cuts by the end of this year, but it also showed one member who expects a lot more easing.

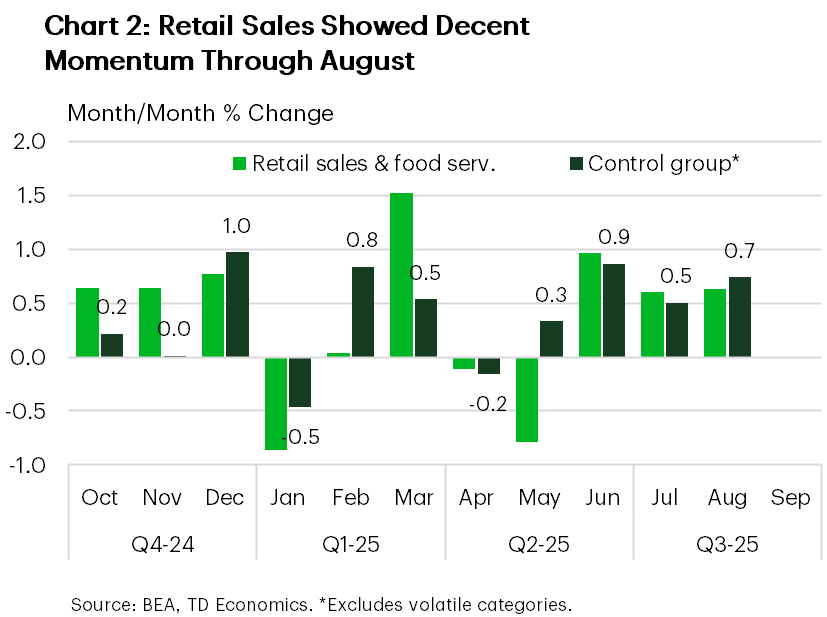

- Retail sales came in better than expected in August, rising 0.6% on the month. Sales in the control group, which strip out volatile categories, rose an even better 0.7%.

Powell’s ‘Risk Management’ Cut

The Federal Reserve resumed its easing cycle after a nine-month pause, cutting the policy rate by 25 basis points at this week’s FOMC meeting. The move was widely anticipated, and while bond yields initially dipped, they ultimately rose as markets digested the broader implications. Equities, however, rallied, with the S&P 500 climbing another 1% on the week at time of writing.

The FOMC statement signaled a shift in emphasis from the ‘price stability’ mandate toward ‘full employment’, noting that “downside risks to employment have risen”. This echoed Fed Chair Powell’s remarks at Jackson Hole last month and set the tone for what he later described as a “risk management cut”. In essence, while inflation remains elevated, the Fed deemed it prudent to begin easing the policy rate to help guard against further labor market deterioration.

The decision was accompanied by the latest Summary of Economic Projections (SEP), which offered a mixed picture. Unemployment rate forecasts were largely unchanged, while growth projections for 2025 and 2026 were nudged up 20 basis points (bps) to 1.6% and 1.8%, respectively. Core inflation expectations for next year were also bumped up by 20 bps to 2.6%, with this measure now projected to return to target only by 2028 – which would mark seven consecutive years above the Fed’s 2% goal. The median forecast now calls for three cuts by year-end (including this week’s) up from two, and is in tune with our expectations. But one member projected the equivalent of three jumbo 50 bps cuts total (Chart 1). Stephen Miran, President Trump’s newly appointed Fed governor, is likely the one projecting more aggressive cuts as he was the lone dissent at this week’s meeting, favoring a larger 50 bps cut.

Economic data released this week did little to bolster the case for continued easing. Initial jobless claims fell back last week, following a surge in the week prior. And while housing remained a soft spot, with homebuilding pulling back in August, consumption-related data came in better than anticipated. August retail sales and food services rose 0.6% on the month, matching July’s gain. Sales in the ‘control group’ – which strip out volatile components – rose a solid 0.7%, building on gains in the prior two months (Chart 2). While tariffs are still expected to chip away at spending power and weigh on consumption, this recent data suggests consumers may still have some gas in the tank.

The bottom line is that while the Fed has resumed rate cuts to guard against further labor market weakness, its “risk management” approach means future moves will remain highly data dependent. The Fed will continue to have a hard time balancing the risks with respect to its dual mandate. But ultimately, we believe that the tariff impact on inflation will be temporary, and we expect the central bank to continue to cuts rates to support the economy (see our latest Quarterly Economic Forecast here).

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.