Financial News Highlights

- The Federal Reserve started its easing cycle with a bang, reducing the policy rate by 50 basis points (bps) in financial news, bringing the target range to 4.75%-5.0%.

- Futures markets are pricing an additional 75 bps of cuts by year-end, slightly more than the updated median FOMC forecast, which shows another 50 bps of cuts.

- Economic data out this week including retail sales, housing starts, and industrial production all came in stronger than expected. Our Q3 GDP tracking sits a 2.1%.

FOMC Starts Easing Cycle With a Bang

There was no doubt heading into this week that the Federal Reserve would be cutting its policy rate on Wednesday. What remained in question, was the size of the cut. Right up until the announcement, market pricing remained relatively split on whether the FOMC would cut by 25 or 50 basis points (bps). Ultimately, policymakers opted for the bigger cut and signaled more easing to come. The more dovish tilt pushed U.S. equity markets higher, with the S&P 500 up just over 1% for the week at the time of writing.

There was no doubt heading into this week that the Federal Reserve would be cutting its policy rate on Wednesday. What remained in question, was the size of the cut. Right up until the announcement, market pricing remained relatively split on whether the FOMC would cut by 25 or 50 basis points (bps). Ultimately, policymakers opted for the bigger cut and signaled more easing to come. The more dovish tilt pushed U.S. equity markets higher, with the S&P 500 up just over 1% for the week at the time of writing.

Accompanying the policy statement, the FOMC also released revised economic forecasts, known as the Summary of Economic Projections (SEP) in financial news. The SEP is an aggregation of each Committee members’ individual forecasts but are not “official” Fed projections. Overall, the median forecast showed that the growth outlook remained little changed relative to the June forecast, with GDP still expected to expand by 2.0% per-year between 2024 and 2027. However, the unemployment rate was revised higher for both 2024 and 2025, and core PCE inflation was marked down in both years.

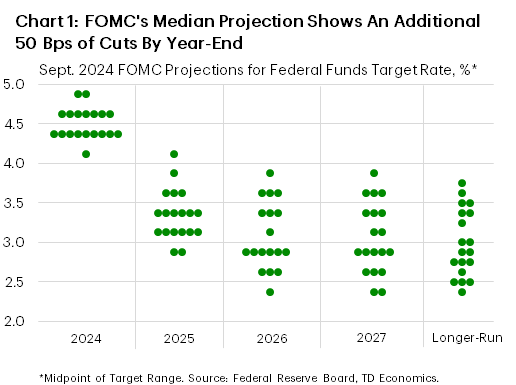

Consistent with the FOMC’s expectations for a slightly softer labor market, and cooler inflation, there were notable downward revisions to the median interest rate outlook (i.e., the “dot plot”) for 2024 through 2026. The revised forecast now shows a total of 100 bps of easing by the end of this year (previously 25 bps) with another 100 bps of cuts projected for 2025, corresponding to a target range of 3.25%-3.5% (Chart 1). This is 75 bps lower than the June SEP.

In the press conference, Chair Powell characterized the larger cut as a “strong start”, but also reiterated that future reductions in the policy rate were by no means on a preset course. Moreover, the Chair pushed back on the notion that this week’s outsized move was driven by a fear that the FOMC had fallen behind the curve. However, he did state that had the FOMC known back at the July 30-31 meeting that the labor market would have cooled as much as it did in the months that followed that rate decision, they probably would have started the easing cycle sooner.

In the press conference, Chair Powell characterized the larger cut as a “strong start”, but also reiterated that future reductions in the policy rate were by no means on a preset course. Moreover, the Chair pushed back on the notion that this week’s outsized move was driven by a fear that the FOMC had fallen behind the curve. However, he did state that had the FOMC known back at the July 30-31 meeting that the labor market would have cooled as much as it did in the months that followed that rate decision, they probably would have started the easing cycle sooner.

As noted in our recent Quarterly Forecast, we feel that odds favor another 50-bps cut in November. If policymakers are truly concerned that today’s policy stance is too restrictive, it’s more likely that they will want to act quickly to alleviate the pressure, before slowing the pace in December.

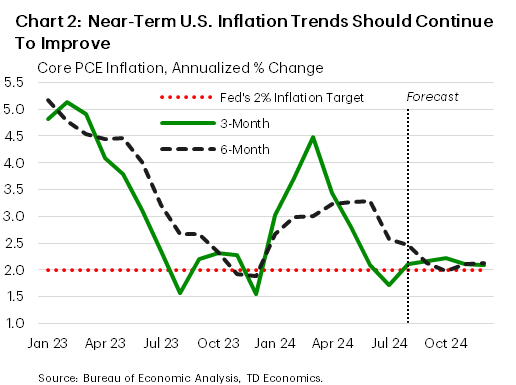

This is not a guarantee. The Fed remains data dependent, and nearly all economic data out this week including retail sales, industrial production, housing starts, and initial jobless claims came in better than expected, and remain consistent with an economy that’s still expanding in the 2-2.5% range. Next week’s personal income and spending data will provide more insight on August spending trends and is also likely to show a bit more progress on easing inflationary pressures (Chart 2). But it’s the September and October employment reports that could ultimately be the deciding factor of whether the Fed cuts by 25 or 50 bps in November.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.