FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

United States

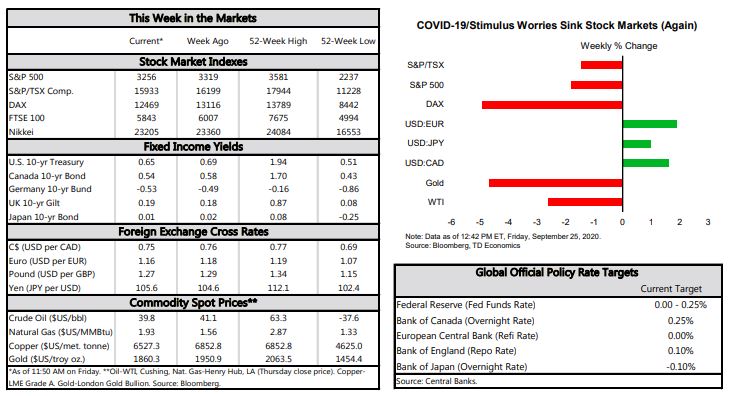

- Major U.S. equity markets edged lower this week, extending their losing streak to four weeks. This came alongside an uptick in new COVID-19 cases and growing evidence that the economic recovery has shifted into lower gear.

- Existing home sales rose by 2.4% to 6.0 million units (annualized) in August – another post-Great Recession record. New single-family home sales did even better, rising 4.8%.

- The labor market is generally still moving in the right direction, but it is doing so at a slower pace. Initial jobless claims rose modestly to 870k last week, extending a flat trend just below 900k. On a more positive note, continuing claims continued to edge lower earlier in the month.

U.S. – More Evidence of Recovery Shifting into Slower Gear

On the data front, the housing market – one of the brightest areas of the U.S. the economy – continued to be a source of good news. Existing home sales rose by 2.4% in August to 6.0 million units (annualized), which marked another post-Great Recession record. The improvement spanned both single and multi-family segments and all four Census regions, though gains in the latter were concentrated in Northeast (13.8%). Meanwhile, in part due to a low inventory backdrop, home price growth accelerated sharply into double digit territory, with the median existing home price up over 11% in August relative to a year ago. New single-family home sales were even more impressive, rising 4.8% even after hitting the highest level in nearly 14 years in July. The level of new home sales has only been higher in the frenzied housing market of the mid-2000s that preceded the Great Recession (Chart 1).

As we argued in a recent publication, housing can’t remain divorced from the broader economy forever (see here). While we expect record-low interest rates to continue to support demand as the economy recovers, the acceleration in prices goes in the other direction. Diminished affordability will become a barrier to further increases. At the same time, the end of mortgage forbearance programs could result in more distressed sales in the quarters ahead. Finally, historically low population growth will weigh on demand growth once the initial recovery phase has played out.

All in all, the labor market is generally still moving in the right direction, but it is doing so at a much slower pace. The capricious nature of the health crisis remains a downside risk, with a still-elevated infection spread to continue weighing on the recovery (Chart 2). In the meantime, without additional income supports, spending could take a tumble as the high numbers of unemployed are forced to reduce consumption. With the Fed clearing up its stance (and limitations) on monetary policy last week, the ball is clearly in Congress’ hands. On this front, yesterday it was announced that Treasury Secretary Steven Mnuchin and House Speaker Nancy Pelosi have agreed to restart stimulus talks, in what marks a small positive step in the right direction.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.