FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Investors paid close attention to developments from the White House this week, with President Trump’s tax overhaul proposal helping to send the S&P 500 to new highs.

- Inflation disappointed again in August, but some states are beginning to display meaningful wage acceleration, as we noted in our Quarterly State Forecast this week, which bodes well for the inflation outlook.

- Next week, investors should look for hurricane impacts to inject volatility into September’s U.S. data. As a result, auto sales should see a boost while net exports should experience a drag.

Equities Soar on Trump’s Tax Reform Proposal

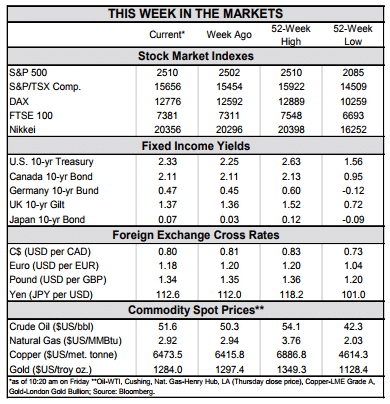

Investors paid close attention to developments from the White House this week, with President Trump’s tax overhaul proposal sending the S&P 500 to another record high at the end of the week. Exchange and fixed-income markets were also impacted, with the greenback appreciating and the ten-year yield rising to its highest level in two months. The proposal contains a sharp reduction in the corporate tax rate to 20% (from 39.1% currently), in addition to the consolidation of personal income tax brackets from seven to three. But the Devil is in the details, of which the plan was largely barren. If delays or opposition to the proposal prevail, equities could pare their gains on diminished expectations for future earnings.

Meanwhile, on the economic data front, Friday’s PCE report marked another month of decelerating inflation in August (Chart 1). Consumer spending was also weak, but that is partly attributable to Hurricane Harvey’s disruption. The report disappointed markets, but not by enough to reverse the equity gains accrued as a result of President Trump’s tax plan announcement earlier in the week.

Across the Atlantic, the Euro Area is also grappling with missing inflation coinciding with solid economic growth. Underlying inflation in September remains subdued, reinforcing the ECB’s stance of cautiously tightening monetary policy. The first steps in winding down asset purchases are expected to begin next year, with further details anticipated following the ECB’s October meeting. Consumer and business confidence indicators have recently returned to pre-recession levels and investors have taken notice, with both the DAX and the FTSE ascending this week while German and UK government bond yields rose.

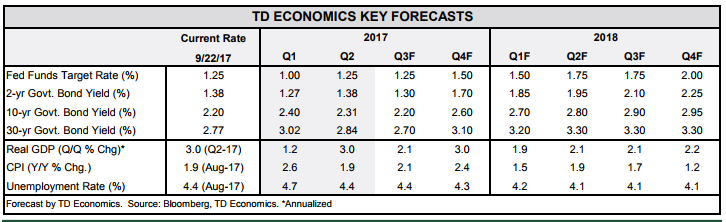

Next week, investors should look for hurricane impacts to inject volatility into September’s U.S. data. Specifically, auto sales should see a boost while net exports should experience a drag. This volatility should fade as rebuilding begins in the fourth quarter. While the Fed will look past hurricane disruptions in the data, inflation data will remain central in guiding monetary policy.

Katherine Judge, Economic Analyst

Financial News, Sept. 29, 2017

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.