FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. stock markets reached new highs this week, with the S&P 500, Dow, and Nasdaq all breaking records, but the economic data has been disappointing. Retail sales data for July suggests a slow start to third quarter consumer spending, which is now tracking 3% – much slower than the 4.2% pace last quarter.

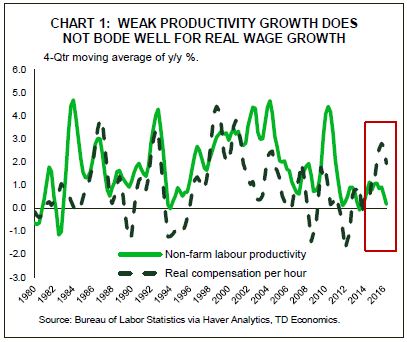

- Data on labor productivity growth released this week indicated a third consecutive quarterly decline. Falling productivity has highlighted the risks of the U.S. falling into a low-growth phase with persistent weakness in labor productivity boding poorly for real wage growth.

- In light of the elevated level of global economic uncertainty and the structural headwinds exerting downward pressure on the long-run growth rate of the U.S. economy, it would be prudent for the FOMC to delay tightening until there were clear signs that the U.S. economy is generating persistent inflationary pressures – something that’s unlikely to take place until next year.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

MORE EVIDENCE BUILDSFOR THE FOMC TO DELAY TIGHTENING

U.S. stock markets reached new highs this week, with the S&P 500, Dow, and Nasdaq all breaking records, but the economic data has been disappointing. Labor productivity declined for the third consecutive quarter in Q2, while this morning’s flat July retail sales report suggested consumer spending slowed at the start of the third quarter, with personal consumption expenditures on pace to grow by 3.0% during Q3. While this is not unhealthy growth, it is nonetheless a significant slowdown from the robust second quarter pace of 4.2%, and suggests less support for third

Economic growth is still poised to exceed the estimated sustainable trend rate of growth. Alongside a tightening labor market and a pick-up in inflation expectations, one could argue in favor for some removal of monetary accommodation in the near term. However, the case for remaining patient and delaying tightening appears to be strengthening. For one, the rise in global economic uncertainty since the UK referendum has accentuated the risk that a small crisis in an EU nation, possibly triggered by a bank failure, could spread more broadly through financial linkages. The risk that heightened financial market volatility, likely to result in a rapid appreciation in the U.S. dollar, is sure to keep the FOMC on the sidelines.

Secondly, there are also signs that not all is well domestically. The persistent weakness in labor productivity growth is a cause for concern (Chart 1). Lack of an increase in output per hour worked does not bode well for real wage growth despite a tightening labor market. Weak labor productivity growth is generally a reflection of a confluence of factors. One such factor is a lack of significant investment in capital necessary to produce a unit of output. The recent disappointment in non-energy business investment speaks to this (Chart 2). Furthermore, the rate of how quickly firms are

incorporating innovative ideas and processes that enhance their efficiency has slowed markedly in the aftermath of the financial crisis.

Lastly, there is a high level of uncertainty about the current amount of monetary stimulus supporting the U.S. economy. Recent estimates of the current real neutral rate for the U.S. economy

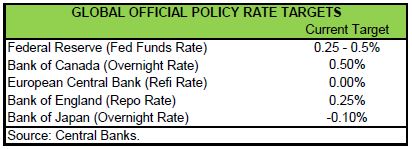

range from 0.2% to -1.0%. With the nominal fed funds rate near 0.35%, and core PCE inflation tracking around 1.6%, this implies a real fed funds rate of about -1.25%. This suggests a fair amount of monetary accommodation in the economy if the real neutral rate is close to zero, but the accommodative cushion nearly vanishes if the neutral rate is closer to the bottom of the estimated range. In fact, in such a scenario, a 25 bp move up in the FOMC’s target rate would remove all remaining monetary accommodation.

Overall, given the elevated level of global economic uncertainty, a U.S. economy facing structurally lower long-run growth prospects, and uncertainty about the current amount of monetary stimulus, it would be prudent for the FOMC to delay tightening until there were clear signs that the U.S. economy is generating persistent inflationary pressures – something that’s unlikely to take place until next year.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.