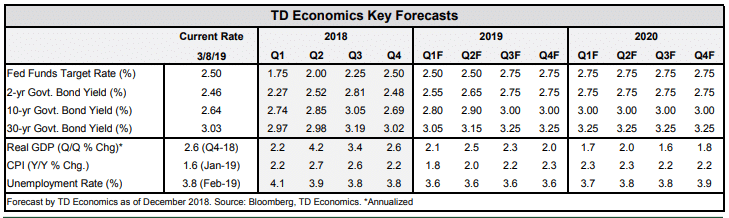

HIGHLIGHTS OF THE WEEK

- This week started off on an upbeat note. An uptick in the ISM non-manufacturing index got the ball rolling, with the headline rising by 3.0 points to 59.7 in February.

- In a nice twist to the recent doom and gloom, housing data was also encouraging. Sales of new homes rose 3.6% in December, and housing starts surged by 18.6% in January.

- The positive economic news faced a setback on Friday as the payroll report showed job growth slowing to just 20k in February. The soft payroll print is unlikely to stay, but works to reinforce the Federal Reserve’s current “patient” approach.

U.S. – Positive Economic Data Muted By Weak Payroll Print

Housing data was also encouraging this week. Sales of new homes rose 3.6% in December, edging higher for the second month in a row. Ditto for housing starts. After ending 2018 on a sour note, homebuilding started the year on better footing with starts surging by 18.6% in January. The gain in single-family construction was even more impressive, with starts up by 25% – the highest monthly gain since 1979. As we discuss in our recent report, the housing market has room to grow and demand should rebound alongside rising affordability. With low vacancy rates, housing construction should continue to make gains over the next year.

There is good reason to look past the dour headline, which was probably influenced by temporary factors and poor weather. We expect job growth to slow in the months ahead, but it will be on the back of a labor market that for all intents and purposes has achieved full employment rather than any pronounced deterioration in domestic demand.

Still, the soft payroll print will reinforce the Federal Reserve’s current “patient” approach. On that front, the Federal Reserve has been joined by other global central banks. This week, the ECB unveiled a package of cheap funding for the Eurozone’s banks and said it would keep rates on hold until 2020 on the back of softening economic momentum and rising uncertainty related to Brexit and trade. The Bank of Canada’s statement this week was similarly dovish – noting the increased difficulty in reading the economic tea leaves given the increase in global crosscurrents. The dovish turn in other global central banks means the U.S. dollar is likely to remain relatively strong, giving the Fed even more reason to remain on the sidelines until at least the second half of this year.

Ksenia Bushmeneva, Economist | 647-876-1707

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.