FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Fed left the policy rate unchanged at this week’s FOMC meeting but signaled that a rate hike was imminent come March. Uncertainty on the pace of hikes post March remains elevated, contributing to stock market volatility this week.

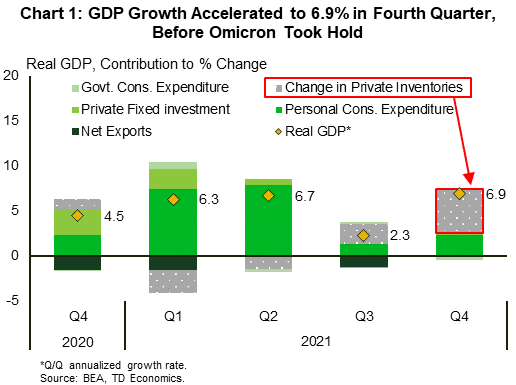

- The U.S. economy grew at 6.9% (annualized) in the final quarter of 2021 – a notable acceleration from the 2.3% pace in the in the quarter prior. Powering growth was a buildup of inventories.

- Consumer spending ended the year on a soft note, with real spending down 1.0% (m/m) in December. Pending home sales also ended the year on weak footing, falling 3.8% last month.

U.S. -Fed Sets the Stage for Rates to Liftoff Soon

The last week of January was rich on data reports, but the FOMC meeting absorbed much of the limelight in financial news. While the Fed left its policy rate unchanged, it delivered its clearest warning yet of imminent rate hikes. A March rate hike is now almost guaranteed, with market odds currently pegged at over 95%. That is likely just the start in what is sure to be a sequence of hikes. Concerns about future monetary tightening contributed to stock market volatility this week. Ultimately, the pace of rate hikes will depend on the pandemic, global supply chains and how aggregate demand reacts to higher rates.

The economy ended last year on a solid note, with a 6.9% annualized jump in fourth quarter real GDP. The acceleration in growth was powered by substantial inventory restocking. Inventories contributed 4.9 percentage points to the headline tally – accounting for over 70% of growth in the quarter (Chart 1). The inventory buildup was led by the retail and wholesale trade industries, with retail auto inventories leading the charge. Business investment (+2% annualized) and consumer spending (+3.3%) also contributed to growth, while a decline in government spending (-2.9%) was a small detractor.

Last quarter’s strong showing largely reflects activity before the Omicron infection wave took hold. Other data this week also pointed to slowing economic momentum at the turn of the year. December’s personal income and spending report showed that real spending fell 1.0% on the month, due primarily to a pullback in goods spending. Services spending remained in positive territory, but spending at restaurants and bars declined, likely reflecting consumer caution due to the rapid increase in COVID-19 infections. Close-contact services are likely to see further weakness in January as high-frequency indicators point to softening in things like air travel.

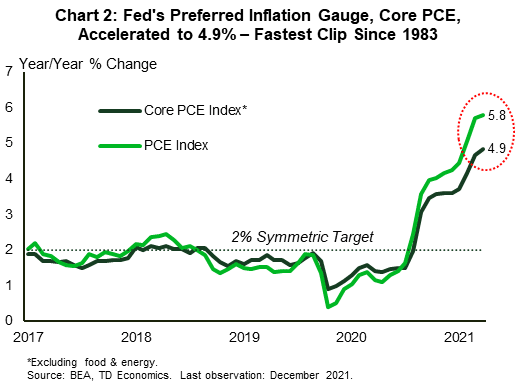

Inflation is adding to consumer woes in financial news. Echoing the acceleration in the Consumer Price Index, inflation as measured by the personal consumption expenditures (PCE) price index rose to 5.8% year-on-year (y/y) in December. Meanwhile, core PCE – the Fed’s preferred inflation gauge – accelerated to 4.9% y/y, moving further away from Fed’s target (Chart 2).

Second-tier data reports also point to slower near-term growth. Pending home sales fell 3.8% in December, marking the second consecutive monthly decline for the series. Pending sales lead actual (closed) sales by 1-2 months, with the recent weakness pointing to a soft start to the new year. A dearth of housing inventory is a key factor behind the weaker year-end trend. Looking at the start of this year, higher mortgage rates and uneasiness among prospective buyers during a surge in COVID-19 infections, are also likely to weigh on activity.

The good news is that the Omicron wave is likely to prove a temporary hurdle to economic activity. New infections in the U.S. appear to have crested. As the economy clears this hurdle, growth should rebound from a modest sub-2% pace this quarter to a much faster clip come spring. Inflation, however, is likely to remain elevated through 2022, even as it decelerates from the current highs (see here).

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.