Highlights

- The second estimate of U.S. GDP growth confirmed that the economy contracted in the first quarter of the year, pulling back by 1.5% relative to the 1.4% reported previously.

- The housing market continued to show signs of buyer wariness as rising prices and mortgage rates erode affordability, resulting in slumping sales both for new and existing properties.

- U.S. consumers continued to post growth in both nominal income and spending in April. Continued price pressures, however, kept real income flat. On the upside, the annual pace of price increases abated in April, as headline personal consumption expenditure inflation decelerated from 6.6% in March to 6.3% in April.

U.S. – Walking the Inflation-Growth Tightrope

Economic developments for the week point to a U.S. economy that is in transition in financial news. As policymakers try to steer the economy from the current high inflation environment, they must walk a tightrope so as not to inflict too much damage on growth. The second estimate of first quarter GDP suggests that it is indeed a delicate balance that will have to be struck. The economy is now estimated to have contracted by 1.5% through the first three months of 2022, slightly lower than the 1.4% previously reported (see here). The revision mainly reflected lower investment in inventory. On the upside, consumer spending and business investment continued to show strong domestic demand.

On that front, orders for durable goods decelerated in April to 0.4% month-on-month (m/m), from a downwardly revised 0.6% in March. Core capital goods orders, a closely watched proxy for business investment, rose 0.3%. The report suggests that business investment growth is starting to taper as interest rates rise. Manufacturers however have a substantial backlog of orders to fulfill, which should continue to support investment in the near term.

The Fed’s mission to tame inflation is likely to see rates rise even further in financial news. Minutes of the Fed’s May meeting reinforced previous messaging as policymakers discussed getting to a neutral rate expeditiously, as well as the possibility of tightening policy to restrictive levels. Such a move would be dependent on the evolving economic outlook, which is currently shrouded in a great deal of uncertainty. We continue to expect two successive 50 basis point rate increases at the Fed’s June and July meetings.

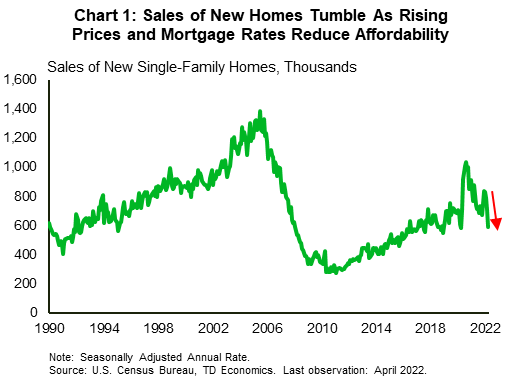

Rising interest rates are also taking some steam out of the white-hot U.S. housing market. Mortgage rates have risen sharply, and this has resulted in a pullback in buyer demand. Contracts for sales of existing homes (-3.9% m/m) as well as sales of new homes (-16.6% m/m) fell in April – both posting the largest declines since before the pandemic (Chart 1). Prices however continued to trek upwards with the median price for new homes rising 19.6% year-on-year to $450,600. The combination of high prices and rising rates is likely to see the market cool even further as affordability becomes an issue for more and more buyers.

The Congressional Budget Office also released an updated outlook this week and is expecting both inflation and economic growth to cool later this year and into 2023. On a fourth quarter-over-fourth quarter basis, the agency expects the economy to grow by 3.1% in 2022 and by 2.2% and 1.5% in 2023 and 2024 respectively. CPI inflation is projected at 4.7% for 2022, 2.7% for 2023 and 2.3% for 2024. These forecasts were completed prior to further fallout from the Russia-Ukraine war. As such, the inflation numbers are likely to come in higher than predicted.

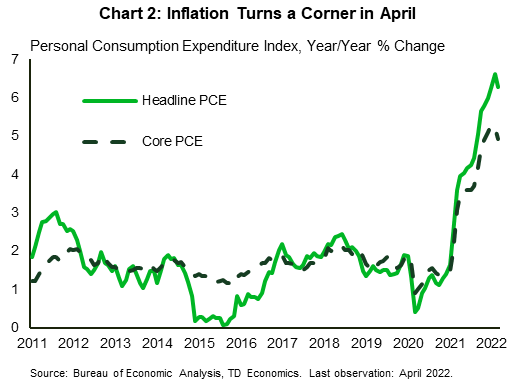

To cap off the week, nominal income and spending were up in April by 0.4% and 0.9% m/m respectively (see commentary) in financial news. However, due to inflation real disposable income was flat. On the upside, both headline and core personal consumption expenditure (PCE) inflation decelerated in April (Chart 2). Yearly core PCE inflation cooled from 5.2% in March to 4.9%, still well above the Fed’s comfort zone, but moving in the right direction.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.