Financial News Highlights

- U.S. CPI came in above expectations, with the headline reading reaching a new 40-year high. Core inflation also surprised with a broad-based acceleration.

- The U.S. trade deficit narrowed in April with both lower U.S. imports and rising exports contributing. We expect further narrowing will add to GDP growth in the second quarter.

- Meanwhile, consumer credit made bad headlines this week, but as long as household income stays on the rise, credit growth should remain sustainable.

U.S. – The Good, the Bad and the Ugly

Market anticipation built through the week for Friday’s CPI data release. Inflation came in above expectations and markets reacted by ratcheting up their expectations for rate hikes. Financial markets have now priced in three consecutive 50 basis-point hikes, starting with next Wednesday’s FOMC decision. The 10-Year Treasury yield jumped seven basis points on the news, finishing the week 18 basis points higher at 3.11% (at the time of writing). Equity markets’ timid attempts to regain their footing early in the week came crashing down Friday, as Thursday’s sell-off intensified.

Indeed, “ugly” seems like an appropriate epithet for May’s CPI print. Energy prices pushed the headline print to a new 40-year high. Since May, the nationwide average retail gasoline price has continued to rise and is likely to reach $5 per gallon in the coming days. This will keep the headline reading elevated in June. Food prices also continued to accelerate, adding to the headline print.

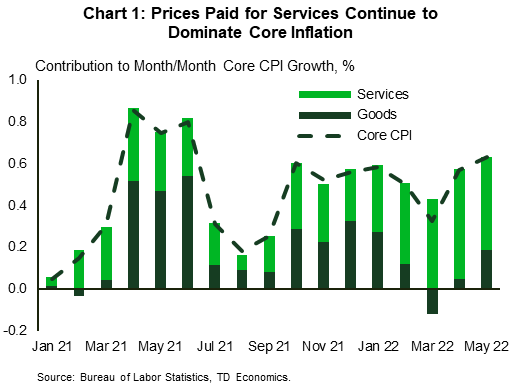

Excluding energy and food, May’s month-on-month core inflation matched the April’s reading. What came as a surprise was an acceleration in core goods inflation. In turn, core services inflation, which tends to be stickier and less volatile, decelerated only slightly remaining above last year’s average (Chart 1). This suggest that core inflation – the main yardstick for monetary policy– is not coming down to a level the Fed would like it to be at any time soon. What’s needed is a further easing in demand, particularly for goods, to lower price pressures. Since some retailers are starting to discount their merchandise in the wake of excessive inventories, we expect pressures there to ease in the coming months.

Some good news came from trade data. The U.S. trade deficit narrowed in April to $87.1 from a record of $107.7 billion in March. Over the past two years demand for imported goods outweighed the value of American exports, contributing to a significant wedge in the trade balance, but this week’s report delivered a snapback, providing some evidence of declining demand for imported items. Meanwhile, exports of goods and services expanded. Trade data is quite volatile and it’s possible to see it zag after the current zig, but we think the recent report portends a reversal of the two-year trend, and we will see the gap narrowing further, adding to GDP growth in the second quarter.

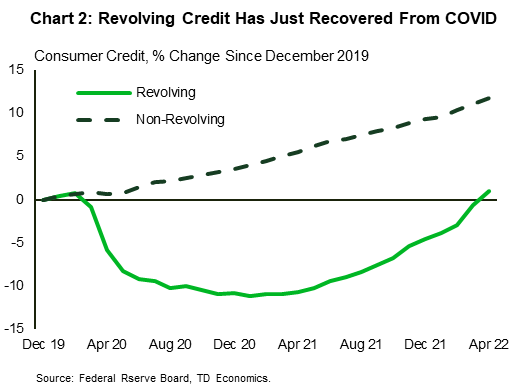

Meanwhile, consumer credit made bad headlines this week as it expanded by $38.1 billion in April after an already sizeable increase in March. This increase suggests that consumers are relying more on credit for their purchases, which could become a burden should they face trouble repaying this debt. Zooming in on details, however, much of this growth was due to an acceleration in revolving credit, which has only just recovered to its prepandemic level(Chart 2). This conincides with a normalization in spending on discretionary services, such as in-person entertainment and travel, which are usually financed by revolving credit, such as credit cards. As long as household income stays on the rise, credit growth should remain sustainable.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.