Financial News Highlights

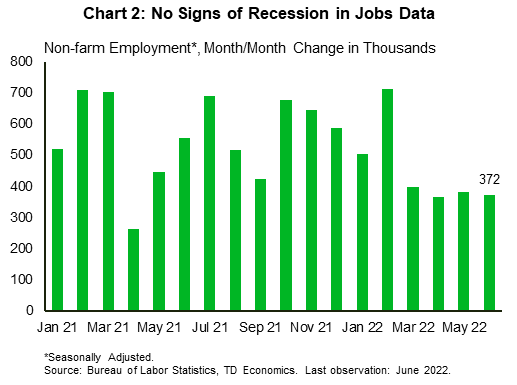

- Recession calls increased this week, but the job market begged to differ. The U.S. added 372k jobs in June, keeping the unemployment rate at its historic low of 3.6% and amplifying fears about inflation.

- In contrast, leading business indicators slipped modestly in June, while remaining above the 50 threshold, which suggests that both manufacturing and services sectors continue to expand.

- The FOMC minutes from the June meeting showed significant worries about the possibility that high inflation is becoming entrenched in consumer expectations. The Fed is positioned for another supersized rate hike at the end of the month.

U.S.-Job Gains Defy Recession Calls

Recession became a much more popular word on the street this week in financial news. Revisions to first quarter GDP data and a weak spending report for May which came out at the end of last week revealed much softer consumer momentum in the first half of the year. This led many forecasters to downgrade their outlooks, with some calling for recession. TD Economics is not calling for a recession, but we acknowledge the downside risks have risen. As such, we have formulated an alternate economic profile on how a U.S. recession might unfold.

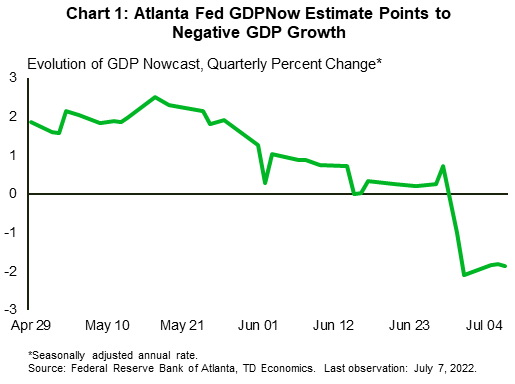

The Atlanta Fed’s GDP Nowcast is pointing to a second quarter of contraction in GDP in Q2 (Chart 1). However, two quarters of contraction in GDP is not enough to qualify as a recession according to NBER criteria – the economic body that defines recessions. In addition to economic output, it places a heavy importance on payrolls employment and real personal incomes less transfers. The income measure has certainly softened with high inflation in recent months but remains in expansionary territory. And the impressive June payrolls report confirmed that employment remained strong (Chart 2). The unemployment rate remained low at 3.6%, and average hourly wages were up a healthy 5.1% year-on-year, both pointing to tight labor market conditions.

Putting aside healthy hiring through June, sentiment indicators are showing some softness. The Institute for Supply Managements’ (ISM) readings for the manufacturing and services sectors both slipped modestly. However, both sectors remained above the 50 threshold, which suggests that both remained in expansionary territory. The underlying details paint a slightly more nuanced picture. Both sectors showed an increase in current business activity, but in the manufacturing sector, the new orders index slipped into contractionary territory, while in the services sector it eased but remained solidly expansionary.

Another important message of the ISM reports is that prices paid by businesses continue to ease – a trend that corresponds with a recent reduction in supply chain bottlenecks. Indeed, the supplier delivery times have improved since the beginning of the year, especially in the manufacturing sector. According to the San Francisco Fed’s research, the distribution of price gains as measured by core PCE inflation is equally split between supply and demand factors, suggesting that cooling on the supply side should help ease inflation going forward.

In the meantime, minutes from the FOMC meeting in June showed that members are worried about the level of stickiness in price gains, and the rising possibility that high inflation is becoming entrenched in consumers expectations. This fear clearly overshadowed any concern the members might have had about prospects for economic growth, resulting in a rare consensus when deciding to supersize the rate hike to 75 basis points. The Fed is positioned for another supersized rate hike at the end of the month, as it focuses on tempering demand.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.