Financial News Highlights

- The Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4%, opened the door to a slower pace of tightening, while also setting expectations for a higher terminal rate.

- The ISM purchasing mangers’ indexes weakened in October, suggesting that demand is softening.

- The economy added 261k new jobs, while unemployment rate rose marginally to 3.7%. It will take much more of a slowdown for the Fed to be convinced that pressures from the labor market are moderating.

A Hawkish Pivot

On Wednesday, the Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4% (Chart 1) in major financial news. The hike itself was expected, what captured headlines was the Fed’s pledge to “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In translation, the Fed plans to take a more measured approach to rate hikes going forward and opens the door to a slower pace of tightening. This sent bond and stock markets higher.

On Wednesday, the Fed increased the monetary policy rate by 75 basis points to a range of 3.75-4% (Chart 1) in major financial news. The hike itself was expected, what captured headlines was the Fed’s pledge to “take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” In translation, the Fed plans to take a more measured approach to rate hikes going forward and opens the door to a slower pace of tightening. This sent bond and stock markets higher.

Thirty minutes later, Chair Powell poured cold water on those animal spirits by clarifying that despite a potentially slower pace of hiking, the terminal policy rate is likely higher than what FOMC members expected in September. He pointed out that the labor market is very tight, and that consumers still have a mountain of excess savings to keep demand healthy. Therefore, further tightening is likely going to be required to rein in inflation. He further emphasized that it is “very premature” to consider pausing rate hikes, which soured market sentiment, pushing equity prices 3.5% lower relative to last week.

Despite Powell emphasizing strength in demand, leading business indicators – the ISM purchasing managers indexes – weakened in October. While the headline manufacturing index just managed to stay expansionary, the new orders and new export orders indexes continued contracting for the second and third straight month, respectively. Services activity also slowed, with demand factors expansion now clearly on the downward trend. This means that the cumulative impact of rate hikes might be catching up to consumers. However, more concerning to the Fed is that following five straight months of decline, the prices paid component of the services index suddenly accelerated. This suggests that the largest sector of the economy is still facing faster and more widespread price increases.

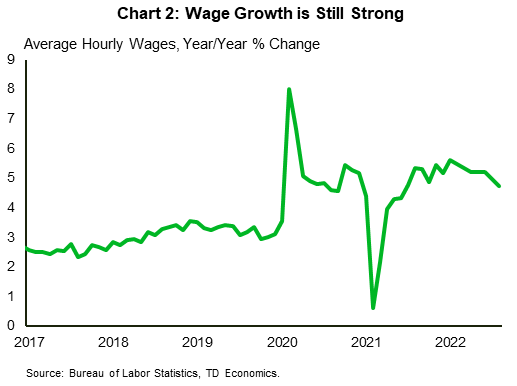

October’s jobs report provided little progress on the Fed’s mission to bring the labor market back into balance. The economy added 261k new jobs, above market expectations for a larger slow down. Meanwhile, the unemployment rate rose by two tenths of a percentage point to 3.7% in the household survey, which showed job losses of 328k in further financial news. While that is an increase, 3.7% is still a very low level historically. The tight labor market showed up in average hourly earnings growth, which eased only slightly to a still very healthy 4.7% year-on-year (Chart 2).

October’s jobs report provided little progress on the Fed’s mission to bring the labor market back into balance. The economy added 261k new jobs, above market expectations for a larger slow down. Meanwhile, the unemployment rate rose by two tenths of a percentage point to 3.7% in the household survey, which showed job losses of 328k in further financial news. While that is an increase, 3.7% is still a very low level historically. The tight labor market showed up in average hourly earnings growth, which eased only slightly to a still very healthy 4.7% year-on-year (Chart 2).

With the Fed laser focused on the bringing down inflation, it will take much more of a slowdown to be convinced that pressures from the labor market are moderating. For now, erring on the hawkish side remains the Fed’s best option. Looking ahead to next week, the CPI report on Thursday may provide some good news with consensus hoping for a slight moderation in price gains. Markets will also be watching the mid-term elections with recent polls pointing to a Republican majority in Congress, resulting in a divided government. While a divided government is historically positive for risk assets, it could result in more fiscal restraint, which would help the Fed at the margin in reigning in inflation.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.