Financial News Highlights

- Republicans look to have won control of the House in this week’s midterm elections. The Senate race remains too close to call. With Washington more divided, major spending and tax changes are less likely, while some risks increase (i.e., the potential for a government shutdown).

- CPI inflation eased in October, with headline CPI decelerating to 7.7% y/y (from 8.2%) and core CPI cooling to 6.3% y/y (from 6.6%). Shelter costs remained a key contributor to inflation.

- Small business confidence pulled back a bit in October, but job openings remained unchanged near record highs.

Markets Cheer Inflation Easing a Touch

The midterm elections took center stage for much of the week, although markets were most encouraged by good news on the inflation front on Thursday in financial news. Republicans look to have won control of the House, capturing an estimated 208 seats thus far (vs. 185 for Democrats), while the Senate remains too close to call. We may need to wait until Georgia’s runoff election on December 6th, to know the final result, depending on races in Arizona and Nevada.

The midterm elections took center stage for much of the week, although markets were most encouraged by good news on the inflation front on Thursday in financial news. Republicans look to have won control of the House, capturing an estimated 208 seats thus far (vs. 185 for Democrats), while the Senate remains too close to call. We may need to wait until Georgia’s runoff election on December 6th, to know the final result, depending on races in Arizona and Nevada.

Either way, Washington is looking more divided than it was a week ago, and the chance that new major policy measures get the three required checkmarks – House, Senate and White House – have diminished. Indeed, large scale fiscal spending measures and major tax changes seem unlikely over the next two years. In this vein, the midterms should not have a major impact on economic growth in financial news. There are, however, risks that come with a divided Congress. One concerning aspect is the potential for a lack of agreement to fund government programs in the near-to-medium term, which could lead to a government shutdown, or debt-ceiling standoff, which raises the (unlikely) risk of a default on debt or leave other bills unpaid. These issues, which have the potential to significantly disrupt financial markets, as they’ve done in the past, are added risks for a slowing economy in the year ahead.

Inflation was likely top of mind for many voters as they headed to the polls, as it has been taking a sizable bite out of consumers’ wallets this year. The Consumer Price Index (CPI) showed that inflation eased in October, for both headline and core CPI, with the latter decelerating to 6.3% year-on-year (y/y) from 6.6% in the month prior (Chart 1). In month-over-month (m/m) terms, core CPI decelerated meaningfully to 0.3% in October from 0.6% previously. Core goods prices declined 0.4% (m/m) amidst a pullback in several categories such as appliances, apparel and used car prices. Price growth across core services (0.5%) also moderated from last month’s gain of 0.8%, driven by a notable pullback in health care services (-0.6%). However, shelter costs (0.8%) remained a meaningful contributor.

All in all, inflation has eased a bit, in part because of the pullback in core goods prices. However, it remains well above the Fed’s comfort zone, and (without wanting to sound like a broken record) we’re likely to see continued gains in the shelter component over the near term (see here). So, we’re not out of the woods just yet.

All in all, inflation has eased a bit, in part because of the pullback in core goods prices. However, it remains well above the Fed’s comfort zone, and (without wanting to sound like a broken record) we’re likely to see continued gains in the shelter component over the near term (see here). So, we’re not out of the woods just yet.

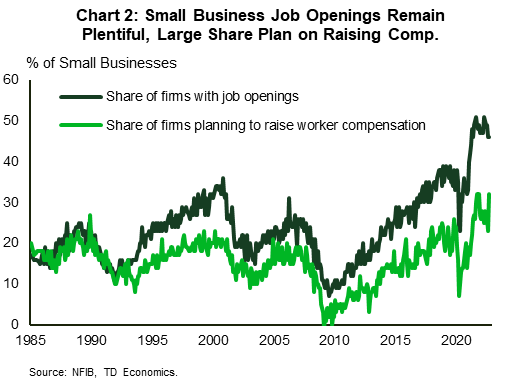

As Fed Chair Powell noted recently, the Fed has reached a point where it will dial back the pace of rate hikes, but there’s quite a bit more to be done in raising rates. Underpinning this hawkish tilt is the broad resilience in the labor market. Job openings for instance, have eased a bit, but remain plentiful – a message echoed by the NFIB small business survey (Chart 2). Still, cracks continue to form in some corners of the economy, case in point the tech sector. Layoffs at Meta and Redfin (online real estate broker) amounting to 13% of their workforces added to the string of cuts announced in the tech space this year. Meanwhile, the higher interest environment is expected to continue weighing on the housing market, with weak prints likely to follow in next week’s housing starts and existing home sales reports. Bringing inflation down comes at a cost.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.