Financial News Highlights

- Minutes from the November FOMC meeting showed a sizeable majority of members were receptive to the idea of slowing the pace of rate hikes in the near-term.

- New home sales jumped 7.5% month-on-month (m/m), far outpacing expectations for a moderate decline, but remain down 5.8% year-on-year (y/y).

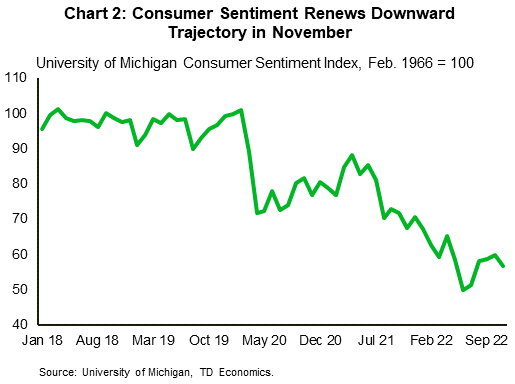

- Consumer sentiment declined in November for the first time since June, marking a return to the downward trend which started in the third quarter of 2021.

U.S. – FOMC Eyes Half-Point Hike

The holiday-shortened week was quiet overall, but did provide a healthy dose of Fed speak, new home sales data, and updated consumer sentiment readings in financial news. Due to lower trading volumes and shorter trading hours in the lead-up to the holiday, market movements this week were muted. The S&P 500 rose 1.5% on the week, while Treasury yields continued their gradual decline, with the 10-Year yield dropping 9 bps to 3.73% as of the time of writing.

The holiday-shortened week was quiet overall, but did provide a healthy dose of Fed speak, new home sales data, and updated consumer sentiment readings in financial news. Due to lower trading volumes and shorter trading hours in the lead-up to the holiday, market movements this week were muted. The S&P 500 rose 1.5% on the week, while Treasury yields continued their gradual decline, with the 10-Year yield dropping 9 bps to 3.73% as of the time of writing.

October’s CPI report has been the centerpiece of market thinking since its release two weeks ago. Fed speakers this week attempted to strike a balanced tone. San Francisco Fed President Daly started the week stating, “although one month of data does not a victory make, the latest inflation report had some encouraging numbers”. Cleveland Fed President Mester in a separate media appearance added that more work still needed to be done, but that “it makes sense that we can slow down a bit”.

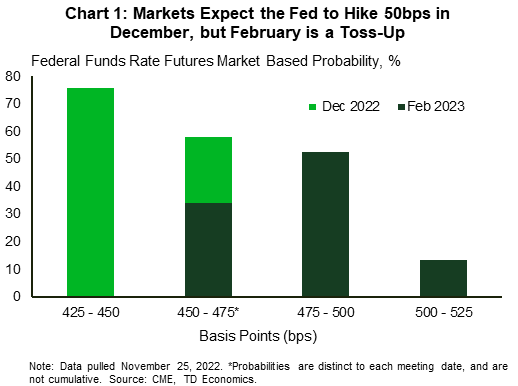

The November FOMC minutes released on Wednesday echoed this sentiment, noting that “a substantial majority of [FOMC] participants judged that a slowing in the pace of increase would likely soon be appropriate”. As of the time of writing, markets are expecting the Fed to raise rates by 50bps in December (Chart 1) in financial news. Next week’s October PCE inflation and November jobs reports should provide further clarification on the Fed’s progress thus far and how much further it may have to go.

November new home sales surprised to the upside, rising 7.5% month-on-month (m/m) versus an expected decline. However, sales are still down on the year (-5.8% year-on-year, y/y). We don’t expect November’s uptick to be sustained. Mortgage rates remain elevated, homebuilder sentiment is at its lowest level since June 2012 (excluding the early pandemic low), and existing home sales have declined for nine consecutive months as of November.

November new home sales surprised to the upside, rising 7.5% month-on-month (m/m) versus an expected decline. However, sales are still down on the year (-5.8% year-on-year, y/y). We don’t expect November’s uptick to be sustained. Mortgage rates remain elevated, homebuilder sentiment is at its lowest level since June 2012 (excluding the early pandemic low), and existing home sales have declined for nine consecutive months as of November.

On the consumer front, we saw the University of Michigan consumer sentiment index reading for November drop 3.1 points to 56.8 (Chart 2). The index had previously notched four consecutive months of gains after a precipitous drop in the second quarter of this year, as the robustness of the labor market, combined with a build-up of savings had provided a cushion to consumers. However, with the unemployment rate ticking higher, job growth slowing, and excess savings winding down, the dual shock of higher rates and higher prices present a stronger headwind.

On a cheerier note, holiday air travel is expected to roughly return to its pre-pandemic level this week. Coupled with the expected spike in retail sales driven by Black Friday deals, the Thanksgiving holiday should provide partial short-term insulation from some aspects of the impending economic slowdown. Next week we’ll see whether job growth decelerated in November, or whether the Fed may have more to think about at its last meeting of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.