Financial News Highlights

- A second read on fourth-quarter GDP showed that the U.S. economy grew by 2.7% (q/q annualized) instead of 2.9%

as reported previously. A measure of underlying domestic demand was revised down from 0.2% to an even softer 0.1%. - Real consumer spending rose a solid 1.1% month-on-month (m/m) in January. Core PCE inflation came in hotter than

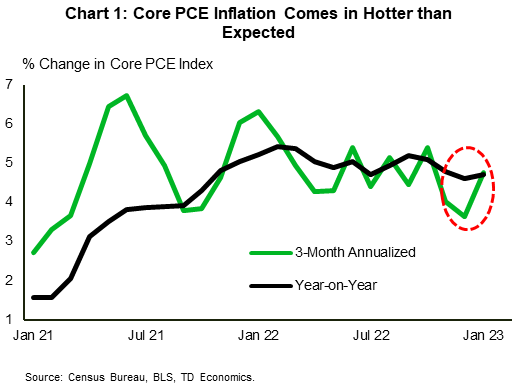

anticipated, rising to 4.7% year-on-year in January from an upwardly revised 4.6% in December. - Despite hopes for an improvement to the housing narrative at the start of 2023, existing home sales fell 0.7% (m/m) in

January, extending their losing streak to 12 consecutive months.

Sticky Inflation Means Higher Rates

Not all economic data was positive this week, but a strong rebound in consumption and evidence of sticky inflation continued to build the case that the Fed will take the policy rate higher in financial news. Rising Treasury yields took a toll on equity markets, with the S&P 500 down 3.3% from last week’s close (at time of writing).

Not all economic data was positive this week, but a strong rebound in consumption and evidence of sticky inflation continued to build the case that the Fed will take the policy rate higher in financial news. Rising Treasury yields took a toll on equity markets, with the S&P 500 down 3.3% from last week’s close (at time of writing).

A second reading on fourth-quarter GDP showed that the U.S. economy ended 2022 on softer footing than previously reported. The headline measure was revised down from 2.9% quarter-on-quarter (q/q) annualized to 2.7%. Net exports and inventory investment, two inherently volatile components, continued to make up the bulk of gain, while final sales to private domestic purchasers – a measure of underlying domestic demand – was downgraded from 0.2% to an even softer 0.1%. This as consumer spending was shaved down noticeably from 2.1% to 1.4%.

However, January’s personal income and outlays report showed that consumer spending rebounded strongly to start the year. Real consumer spending rose 1.1% month-on-month (m/m) in January, reflecting gains in both goods and services. Following in the footsteps of a strong retail sales report, real goods spending rose a sharp 2.2% (m/m), while services spending rose 0.6%. Overall, this is a very good start to first-quarter consumption, which we anticipate will expand in the 1.5-2.0% (q/q annualized) range in financial news. A tight labor market, which is helping support healthy growth in wages and salaries, will also help in this regard.

The above report also provided an update on inflation. Total PCE inflation accelerated to 5.4% year-on-year (y/y) from 5.0% in December. The Fed’s preferred inflation gauge, core PCE, accelerated modestly, rising to 4.7% y/y from an upwardly revised 4.6% in December. The key point to highlight here is that core PCE inflation looks to have picked up some steam recently (Chart 1).

The fact that inflation is showing signs of stickiness and that the labor market remains hot, raises the odds that the Fed will need to take the policy rate higher and perhaps keep it there for longer. Minutes from the latest FOMC meeting, which showed members’ resolve to keep fighting inflation through additional rate hikes based on incoming data, helps further cement this view. Marked odds still favor a rate hike of 25 basis points (bps) at the March meeting, but odds for a 50-bps hike crept higher following the PCE report and are hovering around 33% as of writing.

The fact that inflation is showing signs of stickiness and that the labor market remains hot, raises the odds that the Fed will need to take the policy rate higher and perhaps keep it there for longer. Minutes from the latest FOMC meeting, which showed members’ resolve to keep fighting inflation through additional rate hikes based on incoming data, helps further cement this view. Marked odds still favor a rate hike of 25 basis points (bps) at the March meeting, but odds for a 50-bps hike crept higher following the PCE report and are hovering around 33% as of writing.

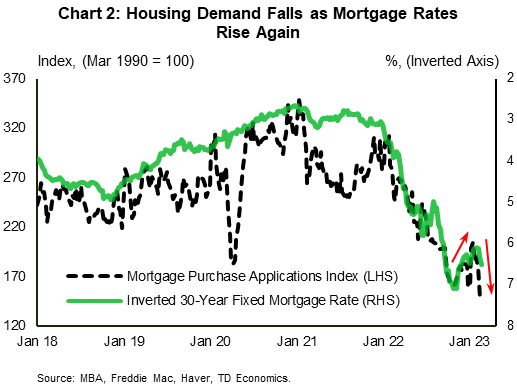

Among other things, a “higher for longer” policy rate, means that there could be additional fallout for interest-sensitive areas of the economy. On this front, existing home sales fell again in January (-0.7% m/m), extending the losing streak to 12 consecutive months. Since interest rate changes tend to influence sales activity with a lag, past declines in mortgage rates could drive some improvement in sales over the near-term. But given that mortgage rates turned higher again, housing activity will continue to be tested. High frequency data second this view, with mortgage purchase applications falling to a 28-year low last week (Chart 2). Indeed, it appears that the start of a new and improving trend in housing is still some time away.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.