Financial News Highlights

- Pending home sales rose 8.1% in January, however with mortgage rates now back up around 7% this is unlikely to be sustained moving forward.

- The ISM Manufacturing Index improved for the first time in six months but continued to indicate contraction in the sector.

- Fed speakers this week noted the upside risk to the policy rate path posed by recent economic data, pushing the 10-year Treasury yield above 4%.

Higher Rates Abound

Congratulations on successfully making it to the third month of 2023. We are now just two and a half weeks away from economists’ most anticipated day of 2023. No, not the first day of Spring, the next FOMC rate announcement on March 22nd. This week we got a peek into six different FOMC members thinking on the expected path of policy and got pulse checks on the housing, manufacturing, and service sectors. In financial markets, Treasury yields continued their upward march, with the ten-year Treasury yield rising above 4% while the S&P 500 has clawed back earlier losses and is up 1% on the week as of the time of writing.

Congratulations on successfully making it to the third month of 2023. We are now just two and a half weeks away from economists’ most anticipated day of 2023. No, not the first day of Spring, the next FOMC rate announcement on March 22nd. This week we got a peek into six different FOMC members thinking on the expected path of policy and got pulse checks on the housing, manufacturing, and service sectors. In financial markets, Treasury yields continued their upward march, with the ten-year Treasury yield rising above 4% while the S&P 500 has clawed back earlier losses and is up 1% on the week as of the time of writing.

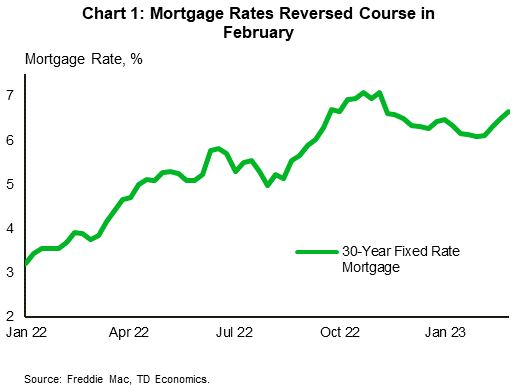

Pending home sales in January increased for the second consecutive month, rising by 8.1% month-on-month (m/m). Falling mortgage rates in late 2022 helped slow the year-long decline in sales activity, despite prices continuing to sink through the end of the year. Seasonally adjusted national home prices, as measured by the S&P CoreLogic Case-Shiller index, continued to decline in December (-0.3% m/m), matching the decline seen in November. With the 30-year mortgage rate rising to 7% in February this reprieve is likely to prove temporary (Chart 1).

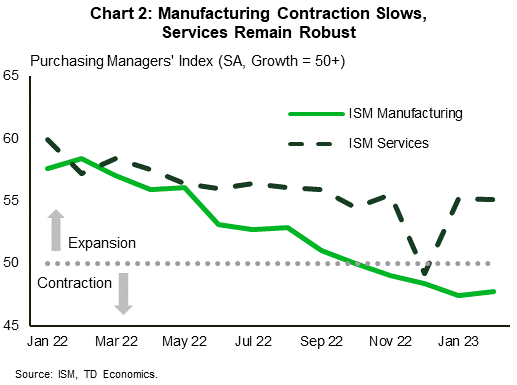

On Wednesday, the ISM Manufacturing Index improved for the first time since August, though the sector remained in contractionary territory for the fourth consecutive month (Chart 2). New orders and backlogged orders continued to contract, albeit at a slower pace. In contrast, the ISM Services Index reading on Friday showed that the industry is still expanding, with new orders growing at a faster pace.

Supplier delivery times continued to see improvement in both sectors with ocean freight costs declining for a sixth consecutive month. However, the manufacturing prices paid subindex increased for the first time since September, reflecting higher raw material prices. Although the subindex remained below the historical level associated with an uptick in the Producer’s Price Index, Treasury yields rose in response to the possible implications this could have on inflation and the Federal Reserve’s policy path.

Supplier delivery times continued to see improvement in both sectors with ocean freight costs declining for a sixth consecutive month. However, the manufacturing prices paid subindex increased for the first time since September, reflecting higher raw material prices. Although the subindex remained below the historical level associated with an uptick in the Producer’s Price Index, Treasury yields rose in response to the possible implications this could have on inflation and the Federal Reserve’s policy path.

Speaking of the Fed, we heard from seven different Federal Reserve officials this week, six of whom are current voting FOMC members. Their talking points covered a range of topics, from Governor Jefferson pushing back against calls for the Fed to raise its inflation target to Chicago Fed President Goolsbee saying it would be a mistake for the Fed to rely too heavily on financial market reactions. We also received policy specific comments, with Minneapolis Fed President Kashkari noting that he is open to a 50 basis point hike at the next meeting and Atlanta Fed President Bostic (a 2024 FOMC member) saying in an essay that he sees the policy rate going to 5.00 – 5.25% and staying there well into 2024.

Members made it clear that they are not yet convinced of the downward trajectory in inflation and upside risks to the policy rate path remain. All eyes will be on next week’s February employment data, which will show whether January’s blowout job growth was just a blip or something more concerning altogether for the Fed.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.