Financial News Highlights

- The Federal Reserve delivered a modest 25-basis point hike this week amid banking stress, lifting the policy rate to a range of 4.75-5.00% – a level that’s just a hair below its previous peak back in 2007.

- Fed projections show the policy rate peaking at 5.1% in 2023, implying one more hike for the year, while next year a series of cuts are forecast to bring the rate down to 4.3%. Market expectations, however, are titled toward a lower rate environment in both years.

- Existing home sales rose 14.5% in February, recording the first increase after twelve consecutive months of declines.

Fed Delivers Small Hike Amid Banking Stress

Stuck between a rock and a hard place, the Fed appears to have taken a middle-of-the-road approach in setting monetary policy this week in financial news. Inflation, which remains well above target and has shown moderate signs of acceleration recently coupled with strong job growth, meant that the Fed could have opted for a more hawkish stance at Wednesday’s FOMC meeting. Fed Chair Powell nodded to this possibility in his testimony to Congress two weeks ago. However, the ongoing banking turmoil has upended this narrative. Instead of leaving the rate unchanged, – an option that was closely considered – Fed officials ultimately went with a 25-basis point hike, lifting the policy rate to 4.75-to-5.00%.

Stuck between a rock and a hard place, the Fed appears to have taken a middle-of-the-road approach in setting monetary policy this week in financial news. Inflation, which remains well above target and has shown moderate signs of acceleration recently coupled with strong job growth, meant that the Fed could have opted for a more hawkish stance at Wednesday’s FOMC meeting. Fed Chair Powell nodded to this possibility in his testimony to Congress two weeks ago. However, the ongoing banking turmoil has upended this narrative. Instead of leaving the rate unchanged, – an option that was closely considered – Fed officials ultimately went with a 25-basis point hike, lifting the policy rate to 4.75-to-5.00%.

In taking this decision, the Fed acknowledged the risks from the banking turmoil, including the potential negative impact on the real economy from tighter credit conditions for households and businesses in financial news. Tighter credit conditions could do some of the Fed’s work for it in reducing inflationary pressures, substituting for further hikes. However, as Chair Powell noted in the press conference, it’s not clear how significant and how sustained the credit tightening will be. The Fed is keeping the door open to some further monetary tightening for now, but changes in the language of the FOMC statement suggest that it is very close to wrapping up its hiking cycle.

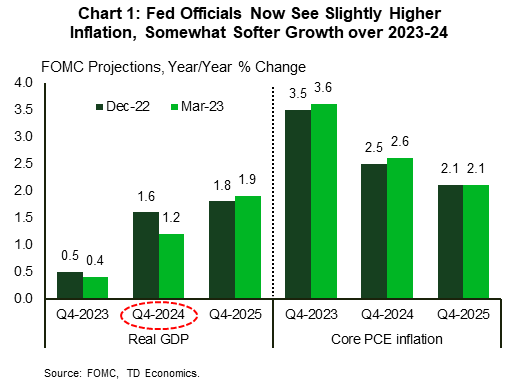

Along with the policy decision, the Fed also issued an update to its quarterly economic projections. Fed officials now expect inflation to remain slightly higher by the end of 2023 and 2024 compared to their view in December. Meanwhile, economic growth is expected to come in a bit softer over this same period, with a downgrade to the 2024 growth profile the most noticeable difference (Chart 1).

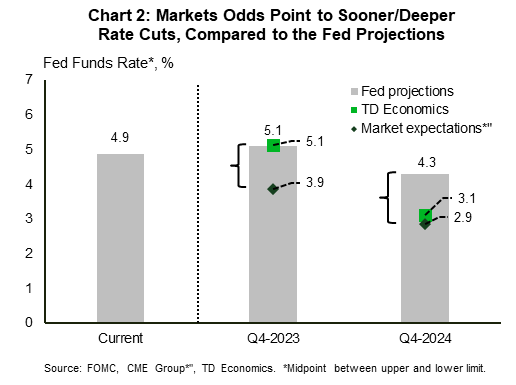

Policy rate expectations remained unchanged for 2023, with most Fed officials expecting the rate to peak to 5.1%, which implies one more hike this year. Market expectations, however, are not in tune with this view. The current pricing suggests that the Fed is done hiking rates, and that rate “cuts” will follow suit shortly this summer. Moving on to next year, while Fed officials have penciled in a series of rates cuts that will bring the policy rate down to 4.3%, market expectations remain more dovish, with the gap between the two forecasts widening (Chart 2). Our projection is aligned more closely with the Fed this year, but as growth slows into next year, we anticipate that in 2024 the Fed will loosen monetary policy more than it projects to steady the economic ship.

Policy rate expectations remained unchanged for 2023, with most Fed officials expecting the rate to peak to 5.1%, which implies one more hike this year. Market expectations, however, are not in tune with this view. The current pricing suggests that the Fed is done hiking rates, and that rate “cuts” will follow suit shortly this summer. Moving on to next year, while Fed officials have penciled in a series of rates cuts that will bring the policy rate down to 4.3%, market expectations remain more dovish, with the gap between the two forecasts widening (Chart 2). Our projection is aligned more closely with the Fed this year, but as growth slows into next year, we anticipate that in 2024 the Fed will loosen monetary policy more than it projects to steady the economic ship.

Reiterating Chair Powell’s view, the degree of credit tightening from the recent banking turmoil remains a major source of uncertainty for the outlook. On this front, it appears that authorities will need to stay alert in putting out more fires. Across the Atlantic, after finding a solution to the Credit Suisse troubles, the attention has now turned to another Global Systemically Important Bank (G-SIB), Deutsche Bank, after a surge this week in the cost of insuring the lender’s debt against default. With banking developments front and center, economic data played second fiddle, but a strong housing report (see here) did bring some cheer.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.