Financial News Highlights

- Headline inflation rose 0.1% m/m in March, while core rose by a strong 0.4% m/m. The 12-month change on headline slipped to a near two-year low of 5%, while core ticked higher to a still uncomfortable 5.6%.

- Retail sales (-1.0% m/m) slipped again in March, falling for a second consecutive month after an unusually strong start to the year. Declines were seen across most categories, leaving a weak handoff heading into Q2.

- Though there are tentative signs the economy is cooling, the Federal Reserve likely has one more 25 basis-point rate hike to follow through on in May, before pausing to better assess the full impact of rate hikes.

Calm Prevails As Economy Shows Tentative Signs of Cooling

Rounding the corner into earnings season, a sense of calm seemed to descend across financial markets this week in financial news. But with earnings season not officially in full swing until Friday morning, investor focus fell squarely on the economic data. The two headliners this week were the March readings of CPI inflation and retail sales, though the release of the FOMC meeting minutes also garnered some attention.

Rounding the corner into earnings season, a sense of calm seemed to descend across financial markets this week in financial news. But with earnings season not officially in full swing until Friday morning, investor focus fell squarely on the economic data. The two headliners this week were the March readings of CPI inflation and retail sales, though the release of the FOMC meeting minutes also garnered some attention.

The latest move by the Federal Reserve occurred during the recent regional banking crisis, which ultimately forced the FOMC to rethink its trajectory for the federal funds rate. The uncertainty was on full display in the minutes, where several participants thought it was appropriate to hold the target range steady last month in light of recent events. This was an abrupt U-turn from what policymakers had communicated just a few weeks prior to the interest rate announcement, where the thought was rates needed to move both higher and faster relative to what had been assumed in the December’s Summary of Economic Projections. But perhaps the most noteworthy takeaway from the minutes was an explicit mention that considering the recent banking crisis “… the staff’s projection included a mild recession starting later this year, with a recovery over the subsequent two years”. Indeed, participants agreed that the actions taken by the Federal Reserve and other government agencies helped calm conditions in the banking sector but deemed that it was still too early to assess the confidence and magnitude of the effect of credit tightening on the real economy.

This morning’s retail sales gave a first glimpse into the impact that tighter credit conditions may already be having on households. Both nominal and real spending fell 1.0% m/m in March, marking the second consecutive month of declines. But even after accounting for the pullback, consumer spending is still tracking a robust 4.2% for Q1 in financial news. However, the weak handoff from March suggests last quarter may have been the “last hurrah” as the cumulative effect of higher interest rates alongside the recent tightening in lending standards appear to be bearing down on the consumer.

This morning’s retail sales gave a first glimpse into the impact that tighter credit conditions may already be having on households. Both nominal and real spending fell 1.0% m/m in March, marking the second consecutive month of declines. But even after accounting for the pullback, consumer spending is still tracking a robust 4.2% for Q1 in financial news. However, the weak handoff from March suggests last quarter may have been the “last hurrah” as the cumulative effect of higher interest rates alongside the recent tightening in lending standards appear to be bearing down on the consumer.

From an inflation standpoint, the softening in demand has yet to manifest in any significant easing in core consumer price pressures. Indeed, headline inflation slipped to 5% y/y – a near two-year low – thanks to lower food and energy prices (Chart 1). However, core CPI rose 0.4% m/m, leaving the 3-month (annualized) and 12-month rates of change at 5.1% and 5.6%, respectively. Underpinning the gains was an acceleration in goods prices alongside continued strength in shelter (0.6% m/m) and non-housing services (0.3% m/m).

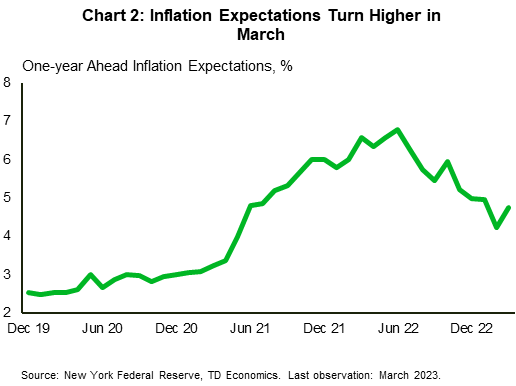

For a central bank who has become increasingly data dependent, the continued persistence in core inflation alongside the recent uptick in inflation expectations is unlikely to sit well (Chart 2). Provided there are no further flare-ups in financial markets, it is likely that the FOMC will need to raise the benchmark rate by another 25-bps in May, before pausing to better assess the full impact of the 500-bps of rate hikes.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.