Financial News Highlights

- Financial markets rallied this week following a string of promising data pointing to easing U.S. inflationary pressures.

- Inflation as measured by the Consumer Price Index fell to the slowest pace of growth since March 2021 in June. Core inflation also only increased modestly on the month. Input costs also trended lower last month, with the Producing Purchase Index falling to the lowest reading since August 2020.

- Though the data overwhelmingly point to easing inflationary pressures, the Federal Reserve is still expected to deliver another 25 basis-point hike later this month.

Inflation Data Brings A Healthy Dose of Optimism

Sentiment across global financial markets firmed this week following a lower-than-expected reading on U.S. inflation in financial news. Recession fears have been top of mind for investors over the past year amidst the Federal Reserve’s most aggressive tightening cycle in several decades. But signs of cooling inflation provided a dose of optimism that policymakers might achieve a goldilocks scenario of returning price stability without tipping the economy into recession. At the time of writing, the S&P 500 is up 2.5% on the week, WTI has rallied by just over 4% to $76 per-barrel, while yields across the board traded lower by approximately 20bps. The 10-Year Treasury yield currently sits at 3.8%.

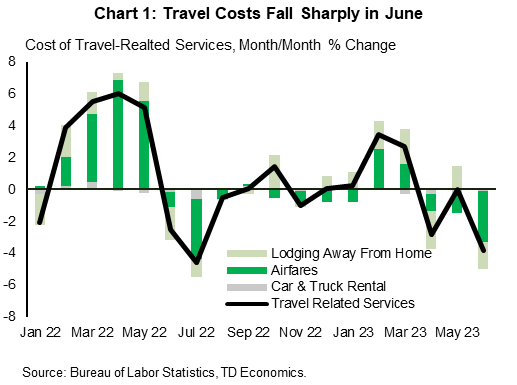

The Consumer Price Index (CPI) eased to a 3.0% pace y/y in June – the lowest reading since March 2021. But, perhaps more notable, core inflation rose by just 0.16% m/m – the slowest pace of growth in 28 months – and dipped to 4.8% y/y. A hefty decline in travel related services underpinned last month’s deceleration, as well as a continued deceleration in shelter costs (Chart 1) in financial news. Used vehicle prices also fell by a modest 0.5% m/m, which came after outsized gains in each of the two-months prior.

Looking to the months ahead, there’s good reason to remain optimistic that further progress will be made on the inflation front. For starters, the much anticipated slowing in shelter costs now appears to be firmly intact, with both owners’ equivalent rent (OER) and rent of primary residence (RPR) having decelerated in recent months. More importantly, current market-based measures of rent continue to show rental costs slowing, which means further disinflationary pressure on OER and RPR as more leases roll over.

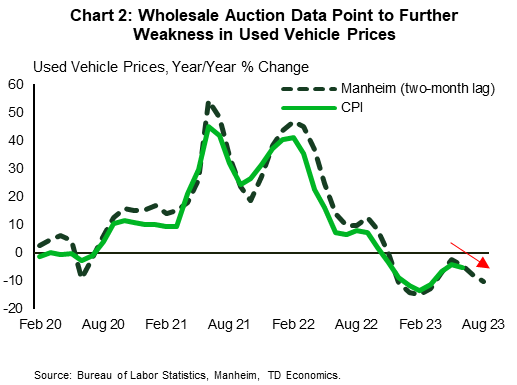

On the goods side, used vehicle prices are expected to be a source of downward pressure on inflation in the coming months. Wholesale auction data for used vehicle prices have tumbled in recent months, with the pass-through to the consumer measure typically taking 2-3 months. (Chart 2). Outside of this category, prices across all other goods have already been flat for three consecutive months and are likely to trend lower through the second half of this year alongside weaker consumer spending. Input costs are also trending favorably. The June reading on the Producer Price Index (PPI) showed that the 12-month change slowed to just 0.1% for final demand products – the lowest reading since August 2020.

Though the recent string of data overwhelming point to a continued easing in inflationary pressures, it is widely expected that Fed will deliver on another 25bps rate hike later this month. No matter which way you slice it, core inflation on a 12, 6, and 3-month annualized basis is still running at a multiple of the Fed’s 2% inflation target. And, with the labor market continuing to exude considerable resilience, policymakers will need to see more convincing evidence that the disinflationary process is firmly intact before calling it quits. Fed Chair Powell has repeatedly emphasized the risk of ‘stopping short’, so the FOMC is likely to maintain a tightening bias over the near-term as they continue to monitor incoming data and fine-tune the end point of its tightening cycle.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.