Financial News Highlights

- Retail sales disappointed market expectations overall in June, but underneath the surface sales in the control group, which are used to calculate consumption, were much stronger, rising 0.6% on the month.

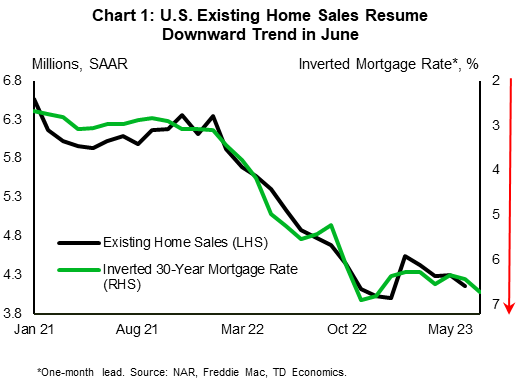

- Elevated mortgage rates and low inventories continue to weigh on existing home sales. The latter resumed their downward trend in June.

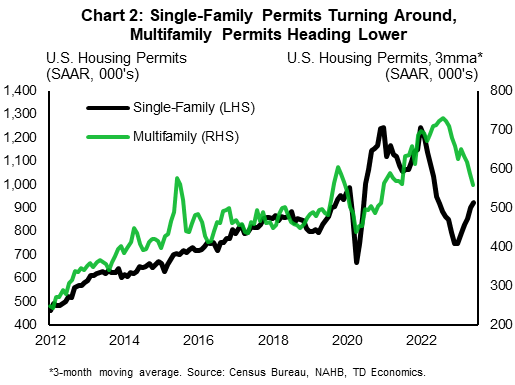

- Housing starts also fell in June. But, permitting data reveals a clear divergence between an upward trend in single-family permits and a downswing in multifamily permits.

Economic data this week wasn’t entirely positive, but it still pointed to an economy that continues to chug along at a decent clip in financial news. With no major red flags on the way, the Fed has the green light to hike the policy rate once more next week, before likely hitting the pause button.

While we expect the labor market to cool ahead, recent high frequency data still points to resilient demand for workers. Continuing jobless claims rose in the week ending July 8th, but initial claims continued to trend lower, easing for the second week in a row last week. With unemployment near multidecade lows, June retail sales suggested consumers are still spending, even as inflation bites into purchasing power. Headline retail sales growth was below market expectations, but an upward revision to the month prior helped provide some offset in financial news. The headline was dragged down by lower sales at gasoline stations, and at building material and garden equipment stores. A notable deceleration in sales at auto and food service establishments didn’t provide much support either. Stronger momentum was seen in the control group, which are used to calculate personal consumption expenditures, with sales rising 0.6% m/m – continuing a healthy pattern for the quarter.

Consumers weren’t as upbeat on homes, with existing home sales resuming their downward trend in June (see here). Elevated mortgage rates are likely to have been a major hurdle, given the tight relationship with sales recently (Chart 1). The higher rate environment has persisted through the first half of July, suggesting that there’s no turnaround in sight for the weakness in existing home sales. Low inventory is also restraining activity. There were only 1.08 million homes for sale in June – 170k less than last year and 840k less than in June 2019 – making for slim pickings.

As we note in a recent report, the tight conditions in the resale housing market are pushing more people toward the new home market. This is much to the delight of homebuilders, whose confidence has been improving rapidly since the start of the year. This optimism has been confined to the single-family segment, however. Multifamily homebuilders have been pulling back. Housing starts retreated in June in both segments, but permitting data reveals a clear divergence between the two segments (Chart 2). The recent softness in the multifamily space is consistent with a rise in the multifamily vacancy rate, and a record-setting number of units under construction in June.

All told, interest-sensitive areas of the economy remain under pressure. But with the employment backdrop continuing to hold up well, consumers still spending, and inflation appearing to move in the right direction, chances of a soft-landing look to have improved. The Federal Reserve is nonetheless expected to maintain a tightening bias over the near-term, and is almost certain to hike the policy rate once more next week. A Fed hike is fully priced in by markets at this point. Provided inflation continues to cool, this will likely be the Fed’s last hike this cycle.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.