Financial News Highlights

- Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation.

- The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown.

- The Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Preparing for Landing

Readers would be right to ask, what’s “moderate” about another upside surprise to economic growth in the second quarter for financial news? Fed Chair Powell signaled a meeting-by-meeting approach on changes to the fed funds rate, opting to evaluate incoming data and fine-tune interest rates to help temper inflation. Incoming data have shown that the economy remains resilient – buoyed by healthy consumer spending growth and business investment – as fears of a recession gradually fade. What remains to be seen is whether inflation will continue to moderate in the coming months or whether the Fed will have to push interest rates higher still – thereby raising the odds the economy contracts.

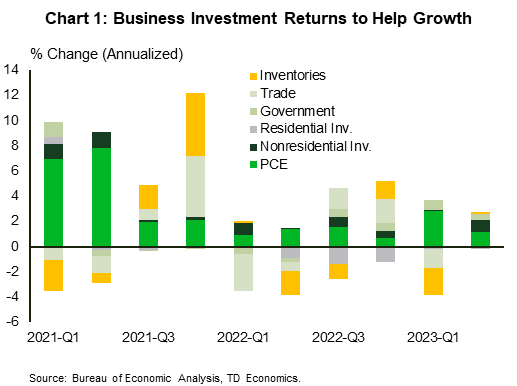

The second quarter’s GDP release showed an economy that continues to chug along at a solid pace – exceeding expectations for a steeper slowdown in financial news. However, the composition of growth was interesting. In line with our forecasts, consumer spending growth advanced 1.6% quarter-on-quarter (q/q) annualized – slowing from 4.2% in Q1. The Fed will be reassured that its rate hiking cycle is filtering through to consumer behavior as spending growth slows despite a drum-tight labor market. Moreover, with rates at multidecade highs, the housing market is feeling the force of tight financing conditions, with residential investment continuing to pull back in the second quarter – now contracting for the ninth quarter in a row. With demand growth slowing, imports pulled back again – now having contracted for the third time in the past year. The gradual slowdown is also not unique to the U.S., as plummeting export growth indicates the global economy is slowing under the weight of inflation and higher interest rates.

A pleasant surprise in the data was the healthy activity in the business sector that provided a meaningful lift to the economy (Chart 1). Nonresidential investment advanced 7.7% q/q – good for the strongest showing since the first quarter of 2022. The flow of federal funds to support climate friendly investments is helping fuel the ongoing strength in structures and equipment investment – the latter registering its best quarterly growth rate since 2011, outside of the post-2020 lockdown bounce.

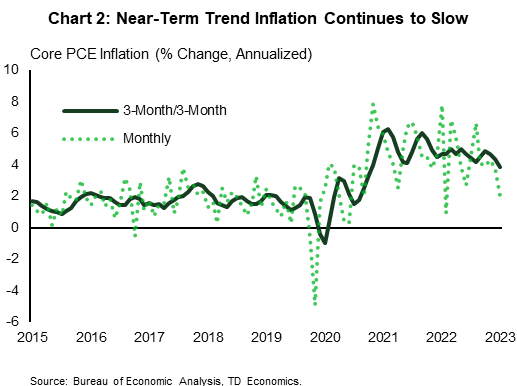

With full second quarter data showing a healthy consumer, all eyes were on June’s personal income and outlay report for signals of spending and price momentum heading into the summer months. Healthy spending held up in June and outstripped income growth, denting the personal savings rate. Between higher interest rates, strong inflation and depleting savings the pandemic era spending binge is slowing down. This is music to the Fed’s ears as it means softening inflationary pressures. Needless to say, the downside surprise on core PCE inflation (4.1% year-on-year vs. 4.2% expected) was a particularly welcome development. Even more encouraging, the near-term trend (Chart 2) has eased to its slowest pace since March 2021.

With inflation slowing and consumer spending remaining resilient the odds of a soft landing are ticking higher. However, the Fed will keep rates in restrictive territory into next year so, even if a recession is avoided, tepid economic growth is to be expected.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.