Financial Advisor News Highlights

- Fitch became the second major credit rating agency to downgrade the U.S. from the top AAA rating, citing the growing fiscal debt burden and an erosion in governance.

- The U.S. economy added 187k new jobs in July, representing the slowest pace of hiring in over two years.

- The Federal Reserve’s Senior Loan Officer Opinion Survey showed credit standards tightened across the board in the second quarter, weighing on loan demand.

Tighter Credit Weighs on Resilience

In this weeks news from the world of a financial advisor, nearly twelve years to the day of the first U.S. credit rating downgrade in 2011, Fitch became the second major rating agency to lower its evaluation of the government’s creditworthiness. Fitch’s rationale was related to growing fiscal deficits in the near-term, medium-term fiscal challenges stemming from aging demographics, and a multi-decade erosion of governance. Since the decision was announced on Tuesday, Treasury yields rose and equities fell, with the ten-year Treasury up 11 basis-points (bps) and the S&P 500 down 1.8% as of the time of writing. Broader implications are expected to be muted as the U.S. economy continues to have strong fundamentals, however it comes at a time when credit standards are already tight.

Monday’s Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) showed that a significant share of banks had tightened business and consumer lending standards in the second quarter. Unsurprisingly, demand for most loan types fell over the period, with the only exception being credit card loans, which saw no change in demand. The economy is clearing feeling the effects of the rapid rise in interest rates over the past 17 months.

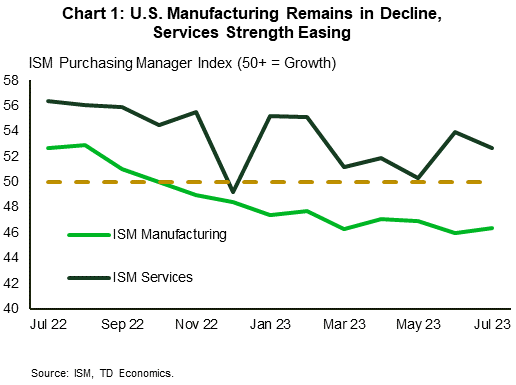

Despite tightening credit conditions, pockets of resilience remain. The ISM PMI data this week continued to show a notable divergence between the manufacturing and service sectors, with the former contracting for a ninth consecutive month and the latter expanding for a seventh straight month in July (Chart 1). Employment growth in both sectors slowed last month, but the services sector is still creating jobs as demand remains robust, whereas the manufacturing employment subindex hit its lowest level in three years.

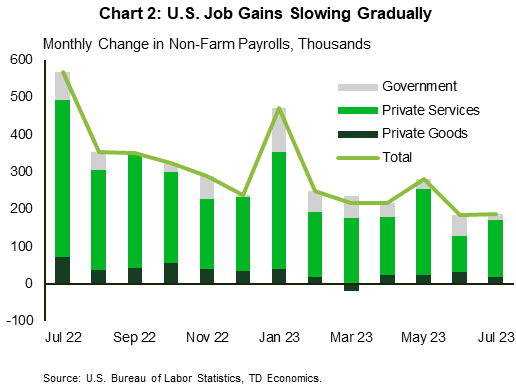

Looking more closely at the most recent labor market update, 187k jobs were created in July, which along with the revised reading for June, represent the slowest pace of job creation in over two years (Chart 2). While this puts job growth on a more sustainable footing, the labor market remains tight, as evidenced by the 4.4% year-on-year(y/y) growth in average weekly earnings in July. The moderation in hiring will be seen as a positive development by the Federal Reserve, but it is unlikely that they will take the prospect of further policy tightening off table until the sustainability of the trend is determined from a financial advisor perspective.

The Fed will get another important indicator next week in the form of the CPI inflation reading for July. June’s print showed core CPI fell below 5% y/y for the first time since December 2021 and the Federal Reserve will be looking to see further progress. With preliminary evidence that the cumulative effects of past rate hikes are working to cool inflationary pressures, we expect that the FOMC will leave the policy rate unchanged when they meet in September. However, they are likely to continue to emphasize the importance of incoming data on determining the future path of interest rates as the ultimate form of ‘landing’ for the economy becomes clearer.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.