Financial News Highlights

- The U.S. economy had good news on the inflation front this week, as core inflation ticked down in July, even as unfavorable base-effects led to a marginal uptick in the headline measure.

- Some Fed speakers this week maintained a hawkish stance, suggesting September’s meeting is an open debate. Incoming inflation and labor market data will play a key role in the decision.

- Small businesses also showed signs that inflation is easing, with fewer of them raising or planning to raise prices.

Word of the Week is Inflation

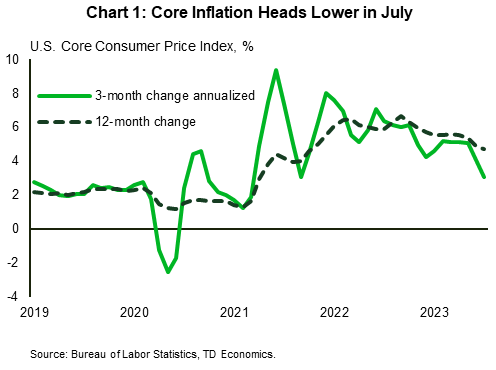

Since skyrocketing during the pandemic, inflation has been a key feature of the economic landscape in financial news. With both consumer and producer price data out this week there was much to add nuance to the scenery. Headline CPI inflation for July was 3.2% year-on-year (y/y), up 0.2 ppts from the previous month. The slight uptick was largely due to base-effects stemming from a notable decline in July 2022 energy prices. The monthly figure was more muted with a 0.2% increase, in line with expectations. Core prices also rose 0.2% month-on-month (m/m) contributing to a deceleration of annual core inflation from 4.8% in June to 4.7% (Chart 1).

Producer prices on the other hand rose slightly more than expected in July (0.3% m/m) due to a pickup in services inflation (0.5% m/m). The uptick in producer prices, which eventually feeds through to consumer prices, illustrates that it may still be too early for the Fed to let its guard down. Nonetheless, these inflation numbers combined with slowing labor market momentum do leave a cloud of doubt about whether the Fed will be raising rates again this year.

Comments from some voting members of the Federal Open Market Committee (FOMC) also suggest that a hike at the September meeting is not a foregone conclusion. NY Fed president Williams noted that both inflation and labor data are generally heading in the right direction, but both are still not quite there yet. He views the question of additional rate increases as still being “open”. Philadelphia Fed President Harker, contrary to his usual hawkish bent, noted that the Fed may be at the point where it can hold rates steady for a while. On the other hand, Fed Governor Bowman is of the view that additional hikes will likely be needed to tame inflation.

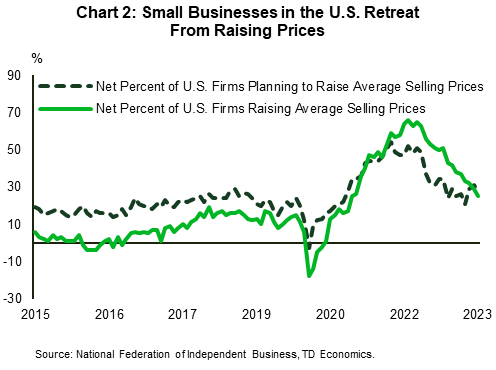

Data from the small business sector also supports the notion that price pressures are receding in financial news. The National Federation of Independent Business survey found that only about one-quarter of small business owners raised prices over the past three months, the lowest reading since January 2021 (Chart 2). Likewise, the share of owners planning to raise prices in the near-term retreated by 4 points following two consecutive monthly increases. Additionally, businesses reporting inflation as their single most important problem declined by 3 points to 21% in July. Overall, the survey suggests that price pressures are moderating, despite a still tight labor market.

One thing that could throw a kink in the downward trajectory of inflation, is rising energy prices in the face of crude oil production cuts by Saudi Arabia and Russia. While the Fed’s preferred measure excludes energy prices, rising oil prices will indirectly boost prices in most other categories.

Ultimately, core inflation should drift lower in the coming months. However, the battle is far from over given that the job market remains tight and the economy resilient. The risk that lower inflation could lift real wages and thus aggregate demand, thereby triggering another round of rising prices, means the Fed will be paying even closer attention to the evolution of jobs data.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.