Financial News Highlights

- And just like that, the Fed’s short-lived pause is likely done after a bevy of positive economic data show an incredibly resilient economy in financial news.

- This morning’s payrolls report showed a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months.

- Financial conditions have tightened this week, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target.

The Jobs Machine Keeps Whirring

And just like that, the Fed’s short-lived pause is likely done in financial news. Markets have responded aggressively to a bevy of positive economic data and sent ten-year government bond yields up 20 basis points since the start of the week. The bond rout had abated mid-week, only to be abruptly undone by Friday’s gangbusters payrolls report that sent yields surging. This week’s data stream shows an economy that continues to shrug off a higher policy rate, likely forcing the Fed to action before the end of the year.

And just like that, the Fed’s short-lived pause is likely done in financial news. Markets have responded aggressively to a bevy of positive economic data and sent ten-year government bond yields up 20 basis points since the start of the week. The bond rout had abated mid-week, only to be abruptly undone by Friday’s gangbusters payrolls report that sent yields surging. This week’s data stream shows an economy that continues to shrug off a higher policy rate, likely forcing the Fed to action before the end of the year.

With all eyes focused on this morning’s payrolls report, it didn’t disappoint with a stellar 336k jobs added in September, along with an upward revision of another 119k jobs to the past two months. The print for September effectively doubled up on the market’s expectations. Industry figures lined up with this week’s ISM services index, as gains were concentrated in the services sector – with leisure and hospitality leading the way.

There isn’t much need to address the details. The strong addition to payrolls squares with the Job Opening and Labor Turnover Survey (JOLTS) that came earlier this week and showed job openings jumped in August, reversing the two prior months’ declines, as firms continue to search for talent. While the number of open positions continues to trend lower from its pandemic-era surge, there remain a whopping 44% more job openings as of August than there were in December of 2019.

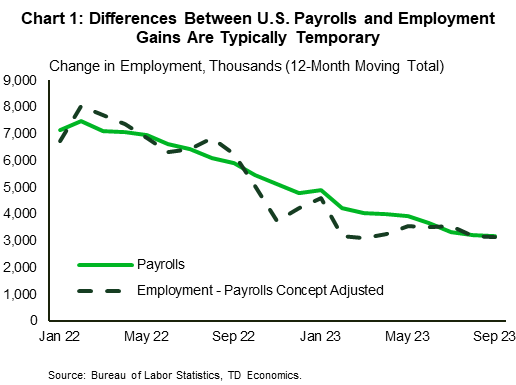

The labor market is tight with jobs aplenty. That said, one apparent contradiction in the report is the wedge between the household employment and payrolls reports. Despite the stellar jobs gains, the unemployment rate was unchanged (3.8%), the labor force participation rate didn’t budge and the number of employed people only rose by 86k. However, deviations of this size are typical and tend to even out in the long run (Chart 1), keeping the focus firmly on the headline job creation figure.

The labor market is tight with jobs aplenty. That said, one apparent contradiction in the report is the wedge between the household employment and payrolls reports. Despite the stellar jobs gains, the unemployment rate was unchanged (3.8%), the labor force participation rate didn’t budge and the number of employed people only rose by 86k. However, deviations of this size are typical and tend to even out in the long run (Chart 1), keeping the focus firmly on the headline job creation figure.

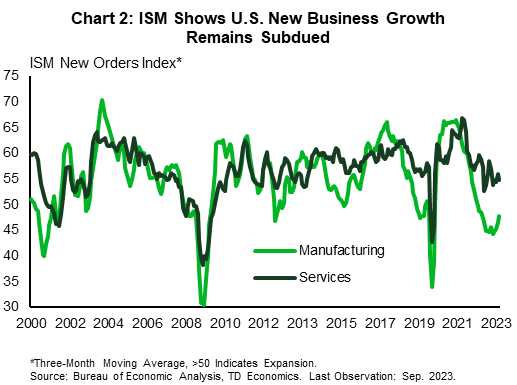

Private sector data that came earlier this week also supported the notion that the economy remains is fairly good shape despite the rate hikes. The ISM Manufacturing Purchasing Managers’ Index (PMI) firmed in the month, showing the contraction in the sector slowed. Meanwhile, its services sector counterpart held in expansionary territory despite slowing for the month. Rate hikes are clearly working as new business growth for both the manufacturing and services sectors (Chart 2) is moderating, but for all the work the Fed has done, it just isn’t proving to be enough.

Bottom line, a week of stronger-than-expected economic data have now all but put an end to the Fed’s pause. Financial conditions have tightened this week and will work to slow activity, but with such healthy economic momentum the Fed still has more work to do to cool demand and bring inflation back in line with its two percent target. This means a hike by year end is now on the table as the Fed continues its work to restore balance and slow price growth.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.