Financial News Highlights

- Consumer Price Index (CPI) inflation printed lower than expected in October, fueling a rally in equities and a sharp pullback in longer-term Treasury yields in financial news.

- A government shutdown was averted this week, as Congress passed another short-term funding bill that maintains current spending levels through mid-January.

- Retail sales data showed a moderation in spending activity in October, while higher frequency credit card spend data suggests the weakness has extended into November.

Extended Fed Pause Looking Increasingly Likely

Market sentiment was decisively in the risk-on camp this week, as a softer reading on October inflation and signs of slowing consumer spending fueled expectations of a longer Fed pause. Also providing a lift to equities was Congress acting to pass yet another short-term funding bill that avoids an immediate government shutdown by extending current levels of spending through mid-January. The S&P 500 is shaping up to end the week 2% higher – extending its winning streak to three-consecutive weeks. Longer-term yields traded lower, with the 10-year Treasury ending the week down 18 basis-points to 4.43%.

Market sentiment was decisively in the risk-on camp this week, as a softer reading on October inflation and signs of slowing consumer spending fueled expectations of a longer Fed pause. Also providing a lift to equities was Congress acting to pass yet another short-term funding bill that avoids an immediate government shutdown by extending current levels of spending through mid-January. The S&P 500 is shaping up to end the week 2% higher – extending its winning streak to three-consecutive weeks. Longer-term yields traded lower, with the 10-year Treasury ending the week down 18 basis-points to 4.43%.

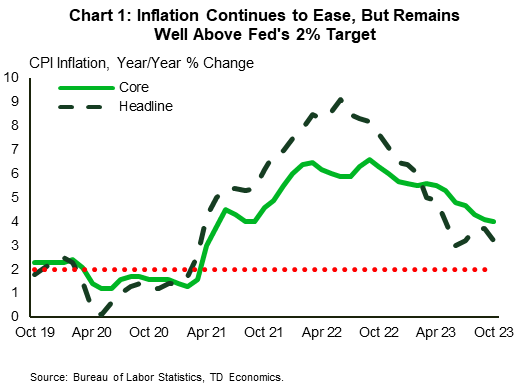

Turning to the Consumer Price Index (CPI) report, both headline and core inflation came in below market expectations. Falling energy and goods prices, a further easing on housing costs and some deceleration in the ‘supercore’ measure all contributed to last month’s softer print. On a twelve-month basis, core inflation is down 2.6 percentage points from last year’s high but, at 4%, remains well above the Fed’s 2% inflation target (Chart 1) in financial news. As noted in our commentary, the challenge for the Fed going forward is that much of the low hanging fruit on the dis-inflation front has now been picked. With supply-chain issues largely resolved, it is unlikely that falling goods prices will continue to exert as much of a drag on inflation going forward. Ultimately, this means a more pronounced slowing in consumer spending will be required to sustain continued downward pressure on inflation.

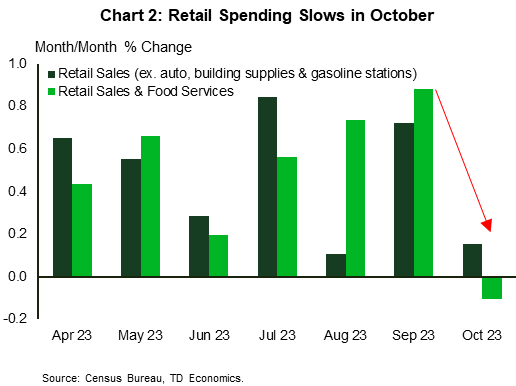

Retail sales data out this week showed that spending activity moderated in October. Although some of the weakness was attributed to a pullback in vehicle sales (possibly impacted by the UAW strike), the less volatile components still showed a meaningful deceleration in spending relative to prior months (Chart 2). Moreover, higher frequency credit card spend data reported through the first week of November has shown that spending activity has continued to moderate into the holiday shopping season.

Retail sales data out this week showed that spending activity moderated in October. Although some of the weakness was attributed to a pullback in vehicle sales (possibly impacted by the UAW strike), the less volatile components still showed a meaningful deceleration in spending relative to prior months (Chart 2). Moreover, higher frequency credit card spend data reported through the first week of November has shown that spending activity has continued to moderate into the holiday shopping season.

At this point, the tailwinds for the consumer seem to be fading. Over two-thirds of the excess savings accumulated during the pandemic have now been exhausted, with most of the remaining savings likely residing with higher income households who tend to have a lower marginal propensity to consume. This is happening at a time when 27 million borrowers have started to make regular student loan repayments amidst a backdrop of deteriorating consumer sentiment and expectations of a cooling labor market.

To that end, recent readings on initial jobless claims have already turned higher over the past month, as have continued claims – recently touching a near two-year high. This suggests that not only are more workers losing their jobs but it’s also becoming a bit harder to find another. Ultimately, the labor market remains very tight by historical standards, but the recent drift higher in claims data suggests underlying conditions are easing on the margin. Although the Fed will need to see further evidence of cooling in the months ahead to rule out another rate hike next year, the recent data flow favors the FOMC holding rates steady in December.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.